NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 :22 July, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the (Jaromir Benes and Michael Kumhof) Chicago Plan Revisited Paper.

Debt bubbles cannot be popped : Business cycles are policy inventions.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Measuring Nothing on the Road to Nowhere : The Myths of Inflation and

Growth Measurement.

Savings Myth. (Revised edition).

There’s no such thing as affordable housing.

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

![]()

This

work is licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence

DEBT

BUBBLES CANNOT BE POPPED:

BUSINESS

CYCLES ARE POLICY INVENTIONS.

By

Sustento Institute,

Version 3 for distribution.

18 July 2013, 3000 words.

EXECUTIVE SUMMARY.

Figure 1 : Model systemic

inflation v. GDP : New Zealand 1968-2013.

{kind=link}

Figure 2 : Debt Model and

Bubble Size for New Zealand 1978-2013.

{kind=link}

Figure 3 : Systemic inflation

and GDP growth in New Zealand 1986-2013.

{kind=link}

Attempts to deflate debt

bubbles deflate the economy not the bubbles.

Not even the Great Depression

of the 1930’s destroyed all the debt that had built up prior to the worldwide

crash. Nor has the present “Global Financial Crisis” deflated the current debt

mountain. The debt mountain has instead increased in the

Bubbles are largely a figment

of macroeconomic imagination. Just like business cycles. Wrecking the world

economy to de-leverage structural debt is like trying to shovel lava from an

erupting volcano.

This article traces the origin

and growth of exponential debt growth, bubbles and business cycles.

In the absence of structural

financial reform orthodox economic theories and policies cannot stop the

impending implosion of the world financial system because they do not offer a

mechanism for appropriate macroeconomic action.

INTRODUCTION.

There is a long history of

attempts to explain business cycles and debt bubbles. The economists involved

include a who’s who of the world’s most prominent academics that is far too

long to list here.

From Irving Fisher’s

“The Debt-Deflation

Theory of Great Depressions” of

1933, to Hyman Minsky’s “ The Financial Instablility Hypothesis” of

1992, many of those writers have

recognized that business cycles and bubbles relate to changes of ....surprise, surprise ...... debt. For example, as long ago as 1951 Arthur Burns

wrote:

“The

problem of how business cycles come about is therefore inseparable from the

problem of how a capitalist economy functions.” (A. F. Burns,

in Wesley C. Mitchell, What happens during business cycles: A progress

report.

Despite the mountains of

learned work over more than half a century since that was written, nobody until

now has properly described “how

a capitalist economy functions” even though the underlying

mechanisms have been staring the world in the face all along.

This article refers

to a debt model of the economy that “connects the dots” to demonstrate the

mechanics of the debt-based financial system.

The model is used

first to discuss what “bubbles” really are, and then to show how macroeconomic

policy itself creates business cycles in a futile attempt to “manage” systemic

debt growth and inflation.

Finally the article

considers the consequences to the world financial system as it becomes

saturated with systemic inflation arising from the exponential increase of

interest-bearing debt.

THE DEBT MODEL.

The author’s debt model of the

economy is most recently summarised in a paper “Measuring Nothing on the Road to Nowhere : The Myths of

Inflation and Growth Measurement.”

In contrast to orthodox

economic work, the author’s modified Fisher Equation of exchange fully

satisfies the basic accounting equation, which is : Assets=Liabilities + Net Worth.

For the M3 banking

institutions and the central bank , the basic accounting equation is expressed

as DC+Dnfca = M3+ R.

DCm

=(GDP)/Vy +Ms +Dni +Db+R - Dnfcb +Nb (1)

Where:

DC = Domestic Credit.

DCm = Domestic Credit plus secondary debt Nb borrowed through

non-bank lending institutions (NBLI).

GDP/Vy = The

debt and cash used to create GDP (Dmy= Dmt+M0y).

GDP = Gross Domestic Product.

Vy = The speed of circulation

of productive transaction accounts.

Dmy = The productive transaction

account balance used to generate GDP.

Dmt = The portion of Dmy

arising from bank debt.

Dni = Debt

supporting non-inflationary economic growth.

M0y = The portion of Dmy contributing

to the non-inflationary cash transactions M0y * Vy

included in GDP.

Ms = Accumulated systemic

inflation arising from net after tax deposit interest paid on the total system

debt DCm .

Dnfca = Net foreign currency assets

(NFCA) resulting from the current account and capital transfers from the rest

of the world.

Db = Bubble debt (debt in

excess of the systemic debt requirements).

R = Bank residual retained profits and paid up

share capital not being part of the money supply M3.

Nb =

Secondary non-bank debt.

Surprisingly, this is the only

model of the debt-based economy that fully satisfies the basic financial

accounting equation, though some other economists like Steve Keen in

The unique features of the debt

model are that:

(a) It

separates the debt needed to fund the productive economy (GDP)/Vy from the remaining terms on the right hand side of

equation (1) that together make up the investment sector of the economy, and

(b) It separates the exponential

systemic inflation component Ms from the other investment sector

terms on the right hand side of equation (1).

Only a small amount of debt is used to physically

generate the economic output GDP. In developed economies, the investment sector

funding is dominated by the systemic inflation component Ms which

itself depends on the existing debt level and the interest rate paid on

deposits. Since the investment sector itself does not produce any goods and services

that contribute to GDP other than taxable services like brokerage and

consultancy provided by financial sector service companies, Ms must

be wholly funded by the productive economy through inflation in the productive

sector.

Ms funding creates an

exponential feedback loop that cannot be stopped unless the interest rate on

deposits is reduced to zero.

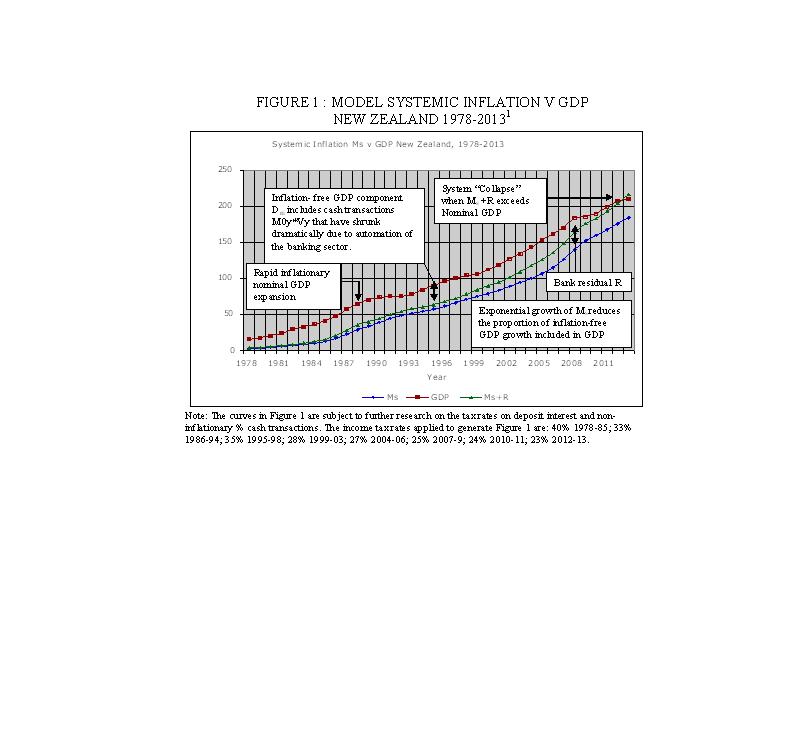

Figure 1 : Model systemic

inflation v. GDP : New Zealand 1968-2013.

Figure 1 plots the components of GDP

shown in equation (2).

GDP = Ms+ Dni+R (2)

Figure

1 shows that accumulated non-inflationary GDP growth Dni has all-but

disappeared in

Figure 1 shows that systemic inflation increased by NZ$150 billion

between 1988 and 2013 while nominal GDP increased by NZ$140 billion over the

same period. The systemic inflation Ms curve closely follows the GDP

curve. All

There has been no “real” GDP increase in

The recent debt de-leveraging

in 2009 and 2010 has made the situation worse, not better, just as it did

following the 1987 share market crash. The two events can be seen clearly in Figure

1 for 1987 (spike in inflation) and Figure 2 (below) for 2007 (spike in bubble

debt Db).

Equation

(2) is derived in the “Measuring Nothing on the Road to Nowhere : The Myths of Inflation and

Growth Measurement.”

While some of the capital

investment supporting the productive sector has been destroyed through debt

default in recessions like those of the early 1990’s and 2009-2010, Ms

continued to expand, as it must do as long as deposit interest rates exceed

zero. Orthodox measurements of “growth” and “inflation” entirely miss the

crucial structural processes taking place in the debt-based economy. For more

information refer to the DNA of the debt-based economy which shows that in a debt based financial system GDP equals the outstanding

principal on capital investment.

BUBBLES.

Bubbles evolve when banks

create and lend more debt than the financial system needs. It really is that

simple, despite a century of misplaced research.

The bubble debt can be easily

calculated by solving equation (1) for Db since all the other terms

are either known or can be independently calculated. To get the bubble size Bu,

the secondary debt Nb has to be added onto Db in Figure

2.

That

equation is: M3= (Dmy+Ms+Dni+Db).

The bubble history for

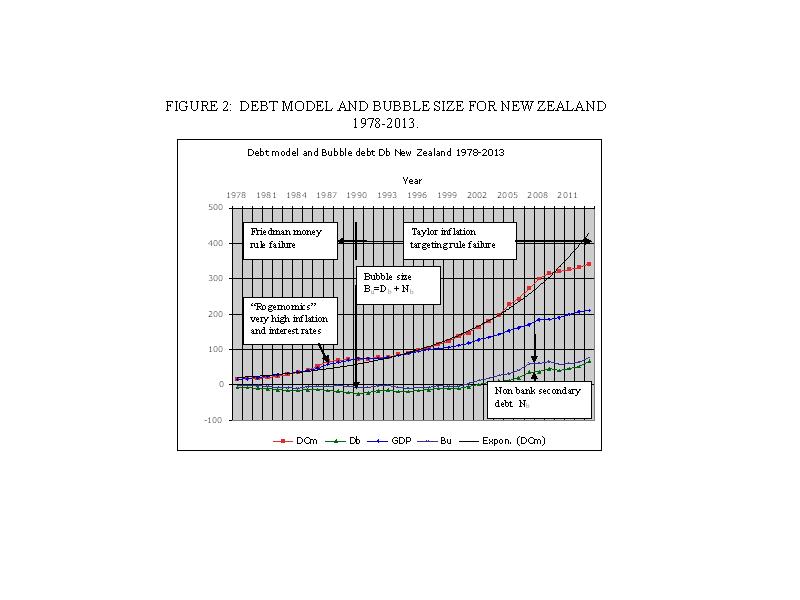

Figure 2 : Debt Model and

Bubble Size for New Zealand 1978-2013.

Figure

2 is plotted for DCm (=DC+Nb) whereas Db is calculated from M3

that does not include

The two major

In the lead up to the 1987

share market crash, policy was guided by the Friedman money rule that allowed

the money supply to expand to match nominal GDP growth. The high inflation that

resulted from the monetary policy was accompanied by substantial “real”

economic growth as it is currently measured under the current System of

National Accounts (SNA). That is clearly shown by the increase in Dni

(refer to the text box in Figure 1). Interest rates were

progressively increased to try to manage the debt expansion, generating even

more systemic inflation Ms. Debt continued to expand until the

productive sector could no longer fund the escalating share prices in the

investment sector. Share prices collapsed because investors’ profit growth

expectations could no longer be satisfied. Many highly leveraged businesses

failed, including (in

Following the 1987 collapse,

orthodox macroeconomic policy was switched from targeting the money supply

following the Friedman money rule to inflation targeting following a

Higher interest rates increase systemic inflation instead of reducing

it.

The demand for new debt then falls but the need for new debt

rises because debt servicing costs in the productive sector increase.

When inflation targeting imposed rising interest rates in

The

In the present financial system debt de-leveraging typically “hits” the

banking sector first, rendering it quickly insolvent as happened in the

The

The recent primary over-funding of debt since 2002 shown in Figure 2 as

the bubble size Bu in

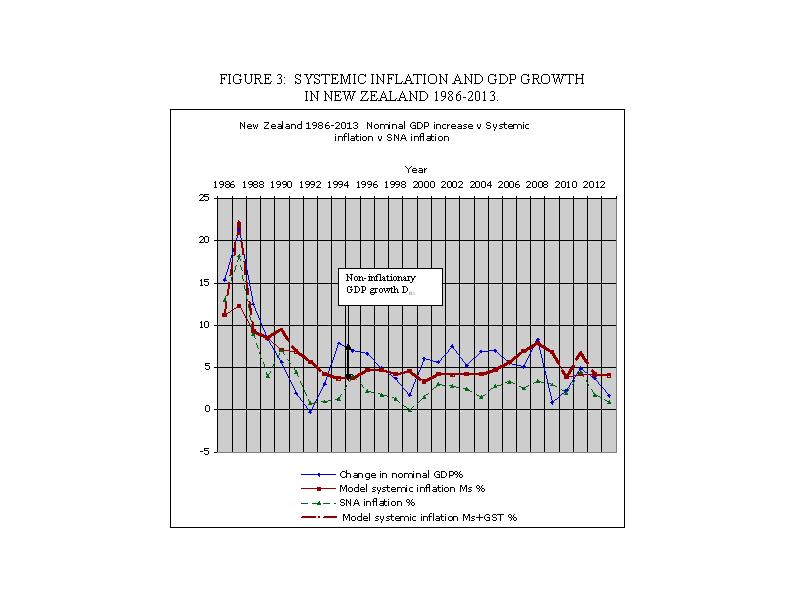

BUSINESS CYCLES.

Business cycles are similar to bubbles except that they are typically of

shorter duration and they are non-structural, being caused directly by the

application of very poor macroeconomic policy options, especially inflation

targeting that has continually suppressed “real” economic growth (Dni).

No sooner than non-inflationary growth Dni has got started, it has

been destroyed by flawed central bank monetary policy as can be seen in Figure

3.

As shown in “Measuring Nothing on the Road to

Nowhere : The Myths of Inflation and Growth Measurement” the use of CPI inflation as the trigger for

interest-rate intervention is not only wildly mis-measured, it bears no

relation to the structural exponential systemic inflation occurring in the

economy. Astonishingly, interest costs are not included in the CPI, so

the effects of interest rate changes are not taken into account when monetary

policy is used to “control inflation”. In

Lower systemic inflation would mean that available productive resources

could be utilised better. More “growth” could occur simply because income

earners would keep more of their incomes. There are no complex theories or

equations involved.

Figure

3 : Systemic inflation and GDP growth in New Zealand 1986-2013.

The business cycle comprises the following sequence:

(a) Since all debt must be

funded from the productive economy, higher interest rates increase the gross unearned

income of deposit holders while reducing aggregate disposable incomes in the

productive sector by the same amount.

(b) Reduced incomes in the

productive sector lead to reduced demand (consumption) there, higher

unemployment, and default on household and business debt.

(c) At the same time, those

same households and businesses are forced to take on yet more Ms

debt to fund higher systemic inflation created by the higher interest rates. That is a classic “double hit” on the productive

sector.

(d) The government receives more taxation from the higher taxes it receives

on unearned income but that extra tax is offset by lower business profits that

reduce the government’s company tax receipts. The government also has to “pick

up the pieces” as unemployment and associated social transfer costs rise.

(e) When households and

businesses cannot take on more debt some of them default, slightly reducing the

rate of increase of total debt DCm. Some of the vast majority who do

not default choose to repay debt instead of consuming. Others try to “save” by

hoarding part of their incomes and reducing their consumption that way.

(f) Nominal GDP increases

below systemic inflation indicate a recession because existing income, and

therefore GDP, is given up to fund the systemic inflation as consumption falls.

(g) There is a cascade effect

on GDP as consumer demand falls, forcing the remaining players in the

productive economy to discount prices and profits.

(h) As the measured (but

wrongly calculated) CPI inflation falls toward the lower end of the inflation

target range, the monetary authorities reduce interest rates.

(i) Disposable incomes begin

to rise because the rate of change in Ms falls. Households and firms

then have more to spend. Some save or continue repaying debt, slowing the

recovery process.

(j) GDP growth in excess of

systemic inflation is “real” (Dni) growth.

(k) There is no inflation targeting for the investment sector so there are

no controls on debt growth there.

Contrary to orthodox economic

theory, the debt model shows there are no multipliers in macroeconomics. The

basic financial accounting equation is a one to one relationship between

financial assets on the one hand and financial liabilities on the other hand.

Inflation targeting and other applications of orthodox macroeconomic

policy destroy inflation-free GDP while increasing systemic inflation.

LIVING

WITH THE CONSEQUENCES OF SYSTEMIC INFLATION.

When nominal GDP and Ms

grow at the same rate the investment sector expands at the same rate as the

productive economy and there can be no economic “growth” (Figure 1).

When Ms increases

faster than nominal GDP, (Dni + R) must fall as shown in equation (2).

GDP = Ms+ Dni+R (2)

Since the banks will not give

up their residual R except in the case of debt default by their clients, the

debt supporting non-inflationary growth (Dni) mathematically must

shrink when Ms growth is greater than the change in the measured CPI

inflation included in nominal GDP. This can be clearly seen in both

As Dni falls towards zero, earlier inflation-free gains in GDP

are lost to the systemic inflation that orthodox economics has failed to

measure, as shown for

Businesses and income earners

are no better off in real terms than they were before the Friedman money rule

and

In

The vast majority of people,

“the 99%”, are financially worse off now in terms of their real purchasing

power and quality of life than they were decades ago.

That is why most households must have two incomes to make ends meet and

why so many people cannot “afford” their own home.

Chaos erupts once Dni has been reduced to zero because the

banking system then fails as R is also (quickly) eroded toward zero through

debt default.

When that happens the monetary authorities have no choice but to “bail

out” the banks by creating some form of interest-free money. That is exactly

what has happened in

To avoid global system failure the financial system must be

comprehensively restructured to eliminate systemic inflation as far as is

possible[1].

In the interim, increases in Ms must be slowed or stopped so

that non-inflationary “growth” can resume. And that, again, is what has

happened in

There is chaos in countries like

The “impossible” in this context is to try to offset ongoing Ms

growth greater than GDP growth against the GDP itself.

According to the author’s debt model that is a theoretical impossibility

because it causes a systemic economic collapse that cannot be corrected without

fundamental reform first of all to reduce the growth of Ms to close

to zero and secondly to control the issue of new credit to avoid bubble

formation.

Lowell Manning 18/7/13

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

Debt bubbles cannot be popped : Business cycles are policy inventions.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Measuring Nothing on the Road to Nowhere : The Myths of Inflation and

Growth Measurement.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English edition, Peter Owen,

![]()

This work is

licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence.