NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02: 18

November, 2010

Edition 03 : 23

February, 2011.

New, revised

edition 04 : 01 September, 2011.

Edition 06 : 09 February,

2013.

(VERSION EN FRANÇAIS PAS

DISPONIBLE)

HOW TO CREATE STABLE FINANCIAL

SYSTEMS IN FOUR COMPLEMENTARY STEPS.

By

Sustento Institute,

"The government should

create, issue and circulate all the currency and credit needed to satisfy the

spending power of the government and the buying power of consumers..... The

privilege of creating and issuing money is not only the supreme prerogative of

Government, but it is the Government's greatest creative opportunity. …….The

taxpayers will be saved immense sums of interest, discounts and exchanges. The

financing of all public enterprises, the maintenance of stable government and

ordered progress, and the conduct of the Treasury will become matters of

practical administration. …….. Money will cease to be the master and become the

servant of humanity."

[

“Financial markets

have worked hard to create a system that enforces their views: with free and

open capital markets, a small country can be flooded with funds one moment,

only to be charged high interest rates - or cut off completely - soon

thereafter. In such circumstances, small countries seemingly have no choice:

financial markets' diktat on austerity, lest they be punished by withdrawal of

financing”.

[Joseph E. Stiglitz “Taming

Finance in an Age of Austerity” Published by Project Syndicate, Monday July

12, 2010.]

Key Words: current

account deficit, debt, debt model, debt growth, deposit interest, domestic

debt, domestic credit, equity in society, exponential debt growth, Financial

Transactions Surcharge, Financial Transactions Tax, Fisher equation, foreign

debt, FTS, FTT, inflation, local currency systems, local economies, revised

Fisher Equation, savings, structural debt growth, systemic debt growth,

systemic inflation, unearned income,

THE PAPERS OF THIS SERIES PUBLISHED SO FAR ARE :

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

ACKNOWLEDGEMENTS.

The author gratefully

acknowledges the support and advice of John Walley and Les Rudd and

the New Zealand Manufacturers and Exporters Association (MEA); to Raf

Manji and the Sustento Institute for their encouragement

and advice; and to Terry Manning and the NGO Bakens Verzet whose

editing and constructive critique have been crucial as the paper has evolved

over time.

![]()

This

work by Lowell Manning is licensed under a Creative Commons

Attribution-Non-commercial Share-Alike 3.0 Unported Licence

CONTENTS:

1. INTRODUCTION

AND

SUMMARY.

2.

MAJOR ISSUES IN REDUCING OR REMOVING DEPOSIT INTEREST.

3.

OPTIONS.

4.

EQUITY IN

SOCIETY.

5.

IMPACTS ON THE PUBLIC

SECTOR .

6.

INDICATIVE COMPARATIVE ECONOMIC

PERFORMANCE.

7.

CONCLUSIONS.

BIBLIOGRAPHY.

APPENDICES.

APPENDIX 1 : THE FOREIGN

TRANSACTIONS SURCHARGE (FTS): SOME INTERNATIONAL BACKGROUND AND CONSIDERATIONS.

APPENDIX 2 : GATS:

APPENDIX 3 : UNDERSTANDING ON

THE BALANCE OF PAYMENTS PROVISION OF THE GENERAL AGREEMENT ON TARIFFS AND TRADE

1994.

APPENDIX 4 : LIST OF DOCUMENTS

COMPRISING GATT 1994.

APPENDIX 5 : LEGAL TEXT OF

GATT ARTICLES XI AND XII.

APPENDIX 6 : IMF DEFINITION OF

CURRENT ACCOUNT AND RELATED CONCEPTS.

APPENDIX 7 : LEGAL TEXT OF

INTERNATIONAL MONETARY FUND (IMF) ARTICLES OF AGREEMENT ARTICLES 1 (PURPOSES)

AND VI (CAPITAL TRANSFERS).

1. INTRODUCTION AND

SUMMARY.

This paper is part of a series

of papers that examine the origin and consequences of unsustainable debt growth

and how to better manage debt levels, money supply and inflation in society at

large.

The paper “The interest-bearing debt system and its economic impacts”

looked at the fundamental cause of exponential debt growth and proposed several

key concepts:

(a) The fundamental debt

problem is that the economy has institutionalised the payment to deposit holders

of unearned income.

(b) That unearned income

takes the form of interest paid on bank deposits.

(c) Interest paid

on bank deposits creates systemic inflation and exponential debt growth.

(d) Orthodox economic

theory fails to provide an effective mechanism to manage either systemic

inflation or exponential debt growth.

(e) There has been a

financial incentive as well as a psychological incentive for deposit interest

to stay in the investment sector.

(f) Culture and

institutional “capture” of the debt debate has prevented rational discussion of

the debt problem.

(g) Sustainable debt

levels can only be achieved by removing most, if not all, new deposit interest.

(h) Quantitative

analysis can be provided using a new debt model of the economy based on a

revised form of the Fisher Equation of Exchange.

This paper is dedicated to

offering practical economic solutions that avoid most systemic inflation and

unsustainable exponential debt growth.

Section 2 sets out the major

issues that are involved when reducing or removing deposit interest from the

debt system to stabilise debt levels and avoid inflation.

Section 3 looks at four

options to reduce or remove deposit interest from the financial system. It also

examines solutions for managing foreign debt and exchange rates as well as the

potential role of local currencies.

Section 4 studies the equity

issues involved when deposit interest is reduced or removed.

Section 5 reviews the effect

on the public sector of reducing or removing deposit interest.

Section 6 compares economic

performance with and without deposit interest using Section 3 Option (B) for

comparison with the existing financial system.

The comparison

between Option (B) and the current financial system shows conclusively that Option

(B) will rapidly bring debt under control and change the SHAPE of the

productive economy. Option (A) in section 3 will produce the same result,

but more slowly, while Option (C) will do so more quickly. The proposals in

Options (A) to (D) in section 3 are not especially unusual. They have all been

used before in one form or another but they have never been linked within a

coherent economic framework until now. An instrument such as the Foreign

Transactions Surcharge (FTS) proposed in the Options is essential in debtor

countries to provide the interest-rate autonomy needed to reduce or remove

deposit interest from the banking system and bring debt growth under control.

2. MAJOR ISSUES IN REDUCING OR

REMOVING DEPOSIT INTEREST.

The paper “The

Interest-bearing Debt System and Its Economic Impacts” concluded that the

world’s debt problem and exponential debt growth arise from the payment of

interest on deposits. That interest represents unearned income. It is paid by

borrowers to deposit holders through the banking system even though the

borrowers get no legal consideration for the deposit interest they pay. Deposit

interest produces nothing, but it shifts consumption capacity from debtors to

the investment sector or paper economy as it is often called, increasing

inequality in society at large. This is discussed in Section 4.

Since the debt

problem arises from deposit interest, a logical solution to eliminating

excessive exponential debt growth is to reduce or remove deposit interest from the

banking system. While a range of options is available to reduce or remove

deposit interest, a number of issues associated with doing so need to be

considered.

Any decision to

substantially reduce deposit interest or remove it from the financial system

implies interest rates at or close to the average spread 01 of the licensed deposit

taking banks. Under the existing financial system the spread that represents

the banks’ costs and profit as well as occasional changes in their provision

for bad debts, is unstable 02. A typical average figure for

the bank spread in a stable financial environment in

1. In the

existing privately owned for-profit banking system low interest rates will

increase the demand for new consumer credit increasing the circulating debt and

unproductive “bubble” lending (part of the circulating debt My in the debt model 02 ). That would increase price

inflation once the capacity in the productive economy has been fully

utilised.

2. In

countries like

3. Lower

interest rates mean higher bond prices.

4. Some

sections of the community, particularly retired people on “fixed” incomes such

as national superannuation, depend upon deposit interest to augment the basic

lifestyle their fixed income allows.

01 The difference between a bank’s lending rate

and the funding rate of interest it pays.

02

The interest-bearing debt system and its economic

impacts.

The four groups are now

considered in turn.

1. Price

Inflation.

There are only two sources of

inflation in the debt model.

The first source is

inflation arising from deposit interest. That automatically reduces towards

zero as deposit interest rates reduce towards zero and so need not be further

considered at this point. Inflation in the price of existing assets in the

investment sector will also fall towards zero, stabilising house prices and

ensuring the investment sector expands in parallel with the productive economy.

The second source

of systemic inflation is the injection of new consumer bank debt or “savings”

(including non-tax based superannuation income) into the circulating debt (My in the debt model). Such

injections increase the amount of circulating debt My 03 without any corresponding

production of goods and services. The orthodox use of interest rates to manage

inflation is by definition excluded by the requirement to maintain low or zero

deposit interest. Other regulatory instruments will be needed to restrain

consumer debt growth. These are discussed later in the paper.

2.

Current Account.

Countries with a

current account deficit have to swap their debt for domestic assets 04. The exchange settlement

process gives the creditor part ownership of the debtor’s economy. Profits

arising from that ownership are also typically repatriated offshore creating a

continuous cycle of increasing their ownership of the domestic economy. Some of

that foreign ownership takes the form of

bank commercial paper whereby domestic banks in the debtor “borrow” foreign

currency to satisfy their exchange settlement requirements 05. In a world of profit-based debt financing,

the debtor is dependent on the willingness of the lender to lend. Foreigners lending to

03 From the revised Fisher

equation in the debt model 02, PQ(d) = My* Vy so that assuming the

structural component Vy remains constant and production Q(d) is also constant (because it has

reached its maximum), the price level P becomes a direct function of My.

04 For a detailed discussion

see The interest-bearing debt system and its economic impacts.

05 In

06 That would be

greatly advanced by limiting or removing inflation from the

07

3.

Bond and Securities Market.

Bonds and Treasury

Bills are usually sold on the basis of a coupon (interest) rate that applies to

the face value of the loan. When bonds and bills are traded, their yield (or

actual interest rate) goes up or down according to their price. When interest rates

fall, the yield falls and so the price must rise. Bond and Bill prices in most

small countries like

4.

Fixed Incomes.

Many household

deposits belong to elderly retired people who have little income other than

their government superannuation. As deposit interest falls, those people may

become more motivated to invest what deposits they have in productive

investments instead of leaving their money in the bank. Many see such

investment as risky, particularly in the light of recent international turmoil

and, in

Very low deposit

rates are far from unknown within the existing financial system.

The main difference

between

08 Though, as of March

2010, 1/3 of

09 In

10 Source : Bank of

11 As of March 2010,

Japan’s net international investment position (including reserve assets) was

plus Y269 trillion, and roughly 57% of its GDP compared with New Zealand’s

accumulated deficit of almost 90% of GDP. Japan’s GDP for the year

ending March 2010 was Y 476 trillion, its public debt was Y 883 Trillion and

private debt (May 2010) including “other surveyed domestically licensed banks”

was about Y 737 Trillion giving a total debt of Y 1620 Trillion or 3.4 x GDP

compared with 1.6 x GDP in New Zealand. [As at early June 2010, 60.5 Yen = NZ$

1, 91 Yen = US$ 1] Data source: Bank of

12 Defining

total debt this way is somewhat misleading. Perhaps a better way to express it

is that

13 House

prices in

14 In

effect, private sector debt has been replaced by public sector debt.

3. OPTIONS.

There are several workable

options available to reduce or eliminate deposit interest from the banking

system. They can be classified under four general headings, each of which

will be discussed in detail. They are discussed in relation to the debt model

shown below.

The first version of the debt

model was published in the paper Manning L., “The Ripple Starts Here : 1694-2009 : Finishing the Past” presented

at the 50th Conference of the New Zealand Association of Economists

(NZAE),

The premise in the

debt model is that the circulating deposits and cash My = Prices P x output q where q

is the quantum of domestic output produced by My over a single cycle. Taken over a whole year, the SNA definition

of Gross Domestic Product GDP is given in the debt model by mathematically

integrating the expression Pq* Vy, where Vy is the number of

times the circulating deposits and cash My are used during the year 16.

The SNA should

reflect an expression of the original Fisher Equation of Exchange 17. The only difference is that the money supply

M in the Fisher equation of exchange included hoarded cash, whereas in the debt

system for practical purposes there is now very little cash contributing to

measured GDP.

My cannot include hoarding of

debt beyond the term of the production cycle because all the productive bank

debt giving rise to My is conceptually repaid at the end of the cycle 18.

At

any point in time there are five broad blocks of deposits in the domestic

financial system.

They are:

Mt The transaction

deposits representing the productive debt My - M0y so:

My

= Mt + M0y (1)

Mca The accumulated

domestic deposits representing the sale of assets to pay for the accumulated

current account deficit. (see section 5 of this paper for details).

M0y The cash in circulation

included in My and used to contribute to productive output.

Ms The net after tax accumulated

deposits arising from unearned deposit income on the total domestic banking

system deposits M3 (excluding repos) 19.

(M0-M0y) Cash hoarded by the public and not used

to generate measured GDP.

In this paper the

total of these deposits, that is, Mt + Mca + M0y + Ms , is

provisionally assumed to be the M3 (excluding repos) monetary aggregate

published by most central banks monthly less the amount of cash in circulation

M0 except for the part M0v that is included in My. In this paper M0y is assumed to have the same speed of circulation as My. In industrialised countries, the contribution

of cash transactions to the measured output of goods and services (GDP) has

been declining in recent decades and their contribution to the GDP has been

provisionally calibrated for the purposes of this paper 20.

19 Repos refer to

inter-institutional lending.

20 More accurate

assessment of the cash contribution to GDP over time requires further detailed

study.

In this paper, the

total debt in the domestic financial system is assumed to be the Domestic

Credit, DC debt aggregate published by most central banks monthly.

At any point in

time there are four broad blocks of domestic debt in the domestic financial

system. Three of them together add up to DC such that:

DC = Dt + Dca 21 + Ds

(2)

Where :

Dt The productive

debt supporting the transaction deposits Mt. .

Dca The whole of

the debt created in the domestic banking system to satisfy the accumulated current

account deficit 22.

Ds The residual debt to balance equation (2)

21 Arguably the accumulated sum of capital

transfers could be included here, in which case the net international investment

position (NIIP) would be used instead of the accumulated current account. The

decision affects the size of the “residual” Db.

22 This is greater

than the monetary deposits Mca because the banking

system may have sold commercial paper to borrow foreign currency to satisfy the

foreign exchange settlement

The fourth block of debt is :

Db, the virtual “bubble” debt, the

excess credit expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit interest Ms defined

above. Db can be positive or negative.

There is also a

fifth block of debt Is that is, conceptually, not bank debt .

Is, the total debt

accumulated by investors arising from Saving Sy = S/Vy.

In the debt model, the

investor pays the investment Iy = I/Vy = Sy = S/Vy to the producer and the money is used to

retire the outstanding part of My relating to the investment in question. Conceptually the investor

borrows the purchase price from employee incomes and the business operating

surplus. Except for households buying new homes, the investor then becomes a

producer, and the interest on investment Iy is included as a production

cost in the subsequent production cycle loans My.

The predicament of

new homeowners is quite different. They cannot service their debt because they

cannot, conceptually earn more than they were before they bought their new

home, because the home itself is nearly always unproductive. There is no new

income stream from their housing investment. If economic demand is to be

maintained, homeowners must, in aggregate, rely upon increasing house prices

and refinancing of their properties, creating an aggregate “pass the baton”

systemic increase in debt.

When non-productive

investment assets are traded there is typically a capital gain because of asset

inflation on investment (Dca + Ms + the property

component of Is). The new purchaser pays more for the asset

because of asset inflation, allowing the seller to retire the outstanding

mortgage debt on the property.

By definition in this paper :

My x Vy = GDP

Ms = Ds

The cash contribution to GDP =

M0y * Vy. Therefore :

DC = (GDP)/Vy - M0y + Ms + Dca

+ Db (3)

Ms =Ds =

(DC – Dca ) – GDP/Vy + M0y - Db (4)

GDP = Vy *(DC - (Ms +Dca

+Db ) + M0y ) (5)

My = GDP/Vy

= DC - (Ms +Dca + Db) + M0y (6)

Where the terms are as defined

above.

Equations (3) to

(6) are all forms of the debt model developed in the earlier paper 23.

23 Links

are provided in the conclusion to this paper.

In the context of

the four Options (A) to (D) listed below, creation of new debt is to be

constrained to meet the needs of the productive economy but there will still be

“savings” so My may still increase.

Whatever option is chosen from among those given below the debt model offers a

solid platform for accurate calibration and management of the financial system.

The model relates to the quantity of GDP. It does not seek to say anything

about the quality of that output, which remains a matter of public debate and

government policy. Common sense would suggest that the more socially and

environmentally useful the productive output is, the better the wellbeing of

the nation is likely to be.

Typical options in

ascending order of effectiveness are:

(A) Maintaining the existing banking system as it

is but with the re-introduction of a supplementary reserve ratio on deposits

(and, should they ever be needed, interest rate caps) to manage the amount of

new lending. The supplementary deposit ratio will be applied over and above the

existing Basle III capital adequacy requirements. In debtor countries this must

be accompanied by some means to manage both the current account deficit and the

exchange rate, such as a universal, variable, temporary and tax-neutral foreign

transactions surcharge (FTS).

(B) As for Option (A) but using the central bank

instead of private banks to supply some new public debt to meet the needs of

the government, and/or to issue interest-free electronic cash (E-notes).

(C) Vesting all credit and money creation in the

government operating through its central bank as in the quote from President

Lincoln at the beginning of this paper, together with a universal, variable,

temporary and tax-neutral foreign transactions surcharge (FTS) as in Options

(A) and (B)

(D) Any of Options (A) to (C) in conjunction with

formally constituted and taxed local currencies.

While the

progression from (A) to (D) may offer a viable route for progressive financial

transformation, the combination of (C) and (D) would ultimately offer the most

powerful benefit and greatest stability to the domestic economy.

Legislation for

each of these proposals can readily be drafted but is outside the scope of this

paper.

The four graded

options are now considered in turn.

OPTION (A): EXISTING SYSTEM

WITH NEW SUPPLEMENTARY DEPOSIT RATIO AND MANAGED CURRENT ACCOUNT AND EXCHANGE

RATE.

Retaining the

existing system is the least flexible of Options (A) to (D) because economic

resource allocation remains, in the first instance, at the discretion of the

private banking system, moderated, as now, by a wide range of tax incentives

and grants administered through the budget according to the government policy

of the day.

The underlying

concept of Option (A) is that the Reserve Bank would set an Official Cash Rate

(OCR), on a regular basis, as it does now, but with a specific supplementary

cash reserve requirement over and above the existing prudential capital

adequacy requirements specified by the international financial institutions,

particularly the Basel III Accord 24.

The mechanism used

to provide the supplementary reserve requirement is of secondary importance as

long as it restricts new bank lending to prevent bubble formation. The

reserve could be a percentage of its net capital assets or net worth.

The cash rate might

be, for example, 0.5%. Interest rate caps would only be contemplated if

the claims interest rate (the lending rate) charged by the registered banks exceeds

a target maximum interest rate specified by the Central Bank from time to time 25. The Official Cash Rate

reduction from present levels could be phased in over time, but quite a few

developed countries already have lower official cash rates than

24 The Basel III accord revised the risk based capital requirements for

the international banking system.

25 Rather like present

inflation targets-for example, with a cash rate of 0.5% and an acceptable

spread of about 2%, an interest rate cap might be specified if average claims

(lending) rates exceed, say, 2.75% .

26

As discussed later in this section, time may be needed for the various

structural adjustments to “bed in” and it may turn out to be prudent to reduce

interest rates and increase the FTS in parallel. The implementation of Options

(A) to (D) will need to be integrated to avoid capital flight.

To give a

practical example, suppose Option (A) is in place and that the rate of change

in Dca , (dDca/dt) and in Ds , which is the debt

corresponding to the unearned income deposits Ms, (dDs/dt) in equation (5) are zero, that domestic

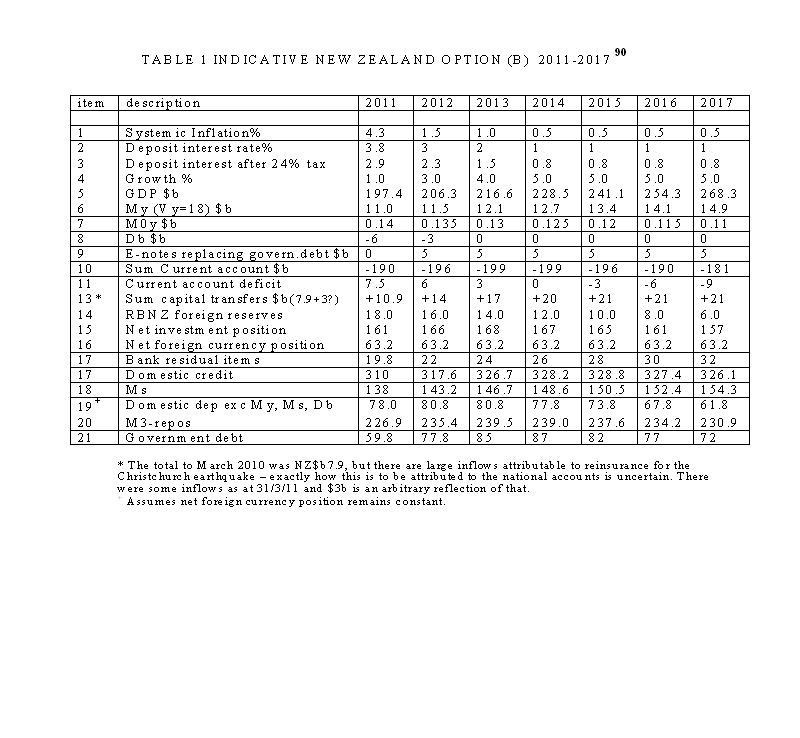

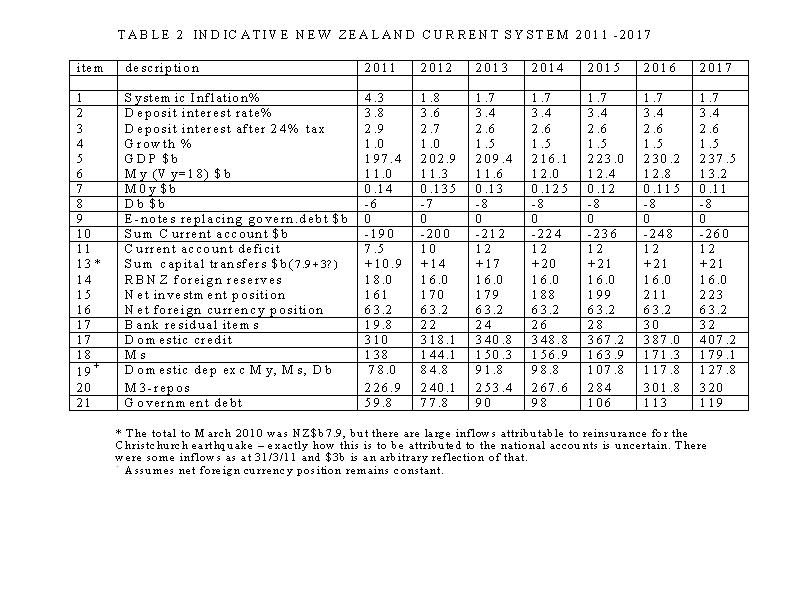

credit is NZ$ 310.8 billion (New Zealand, March 2011) and that the bank debt

multiplier under the Basel III accord is 12 (so the banking system risk-based

capital base is, say, roughly NZ$ 26 billion 27). An increase in the reserve

ratio of just 0.01% of domestic credit would require extra capital reserves of

NZ$ 26 million to be deposited by the registered banks with the Reserve Bank.

Compared with the status quo, that would restrain lending by NZ$ 31.2 million

or 0.15% of the NZ March 2011 gross domestic product of NZ$ 197.4 billion. That

makes banks’ capacity to lend sensitive to the proposed supplementary reserve

asset ratio.

The supplementary

reserve ratio would be operated in conjunction with the banking system to

ensure the creation of new debt increases at the (almost) inflation-free productive

growth capacity of the economy, say, 5% or NZ$ 9 billion a year. In

equation (3) above, five percent growth would require a very small change in

domestic credit Dc of about NZ$ 0.5 billion (NZ$ 9 b growth divided by an

assumed value of Vy of 18) 28. In the example, using

equation 3, assuming the change in Dca and Db remain constant, the increase

in Domestic Credit would be reduced by about

(2.5% -0.5% , the change in OCR and the interest rate paid on deposits)

x the existing figure for M3-repos, (say NZ$ 230 billion) or

about NZ$ 4.6 billion. This is a small

portion of recent historical total debt growth in

Five percent real economic

growth, representing NZ$ 4.6 billion of new debt, with 0.25% inflation in the

productive economy and about 0.5% inflation in the investment sector sounds a

lot better than in New Zealand in recent years where the total debt growth has

been more than NZ$ 30 billion, real GDP growth around 2.5%, investment sector

inflation up to 10% and CPI inflation 2% or more 30 .

Eliminating the so-called

fractional reserve banking system is now getting mainstream attention. Mervyn

King, the Governor of the Bank of England is reported to be raising the

possibility of eliminating the fractional reserve system altogether 31. "If [

27 For illustration –

detailed figures are at Reserve Bank of New Zealand Statistical Series G3

28 Neither Vy nor My has been accurately estimated

for New Zealand yet because the indicative debt model application provided in

the papers does yet accurately reflect the effect of taxation on gross deposit

interest.

29 Except for the

March year 2010 when it was still more than NZ$ 14 billion despite nominal GDP

growth of just NZ$ 1.3 billion (which included 2% of GDP, or NZ$ 3.7 billion,

inflation).

30 The profound economic impact

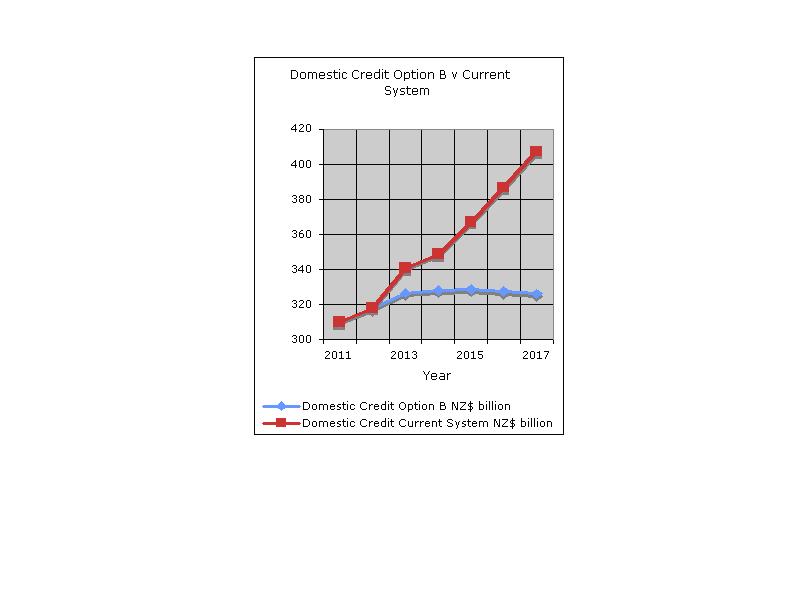

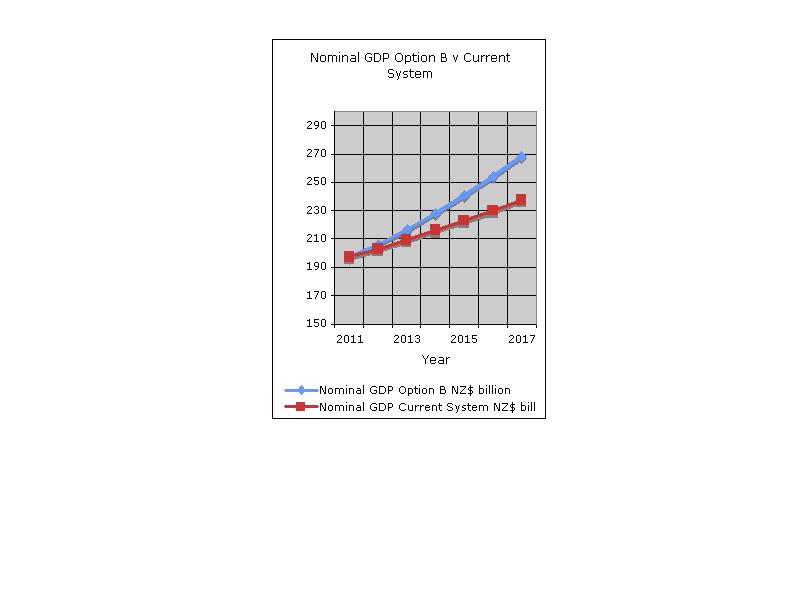

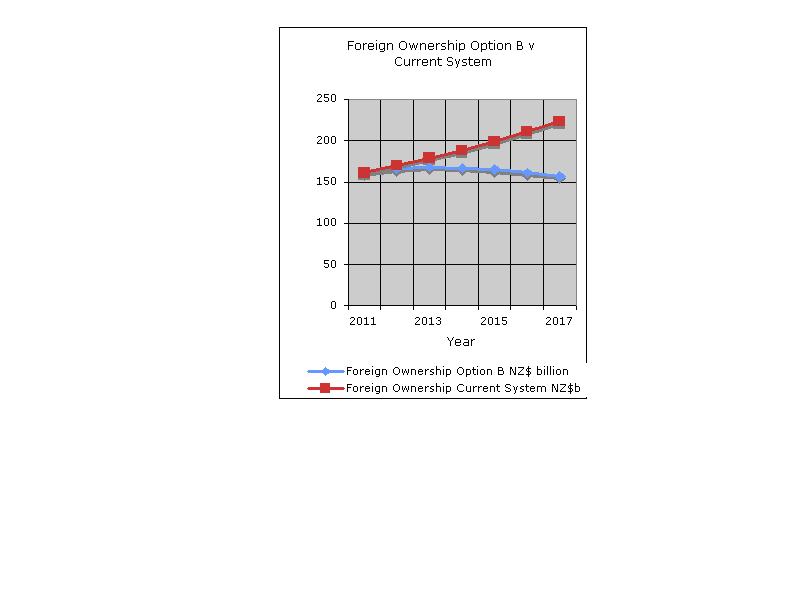

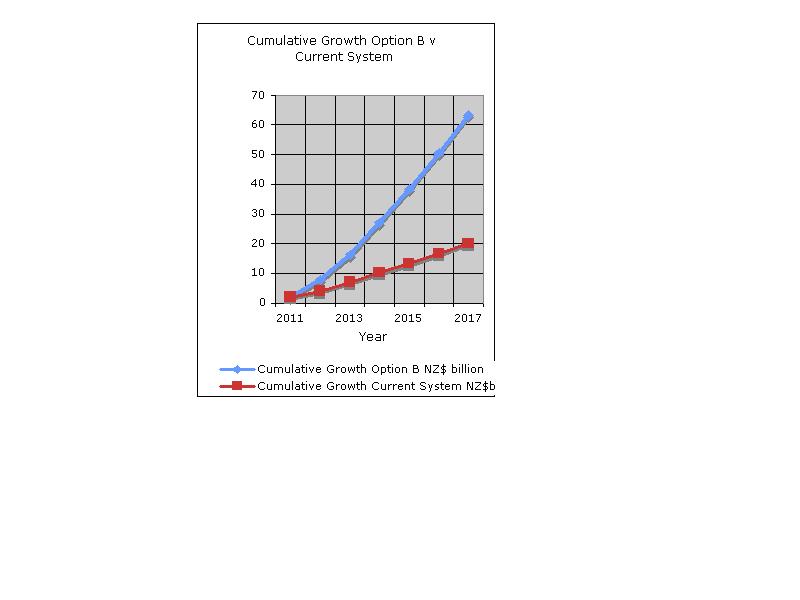

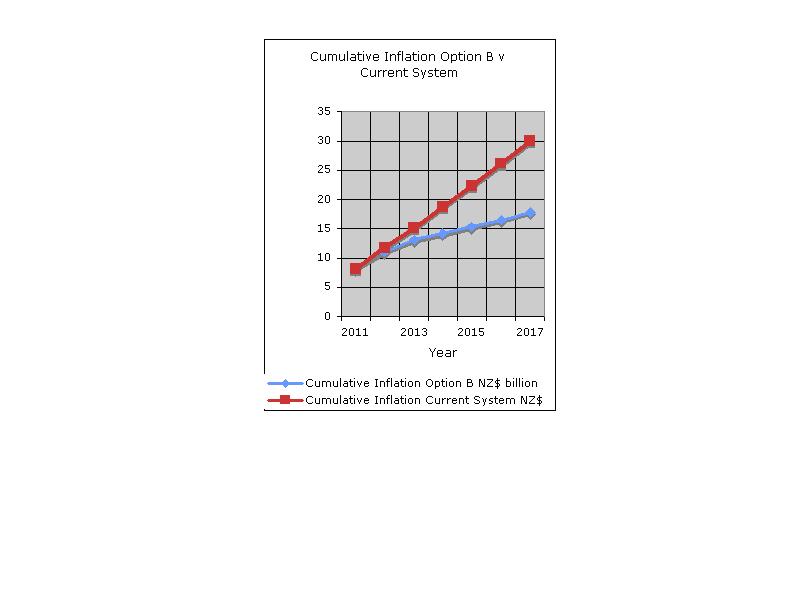

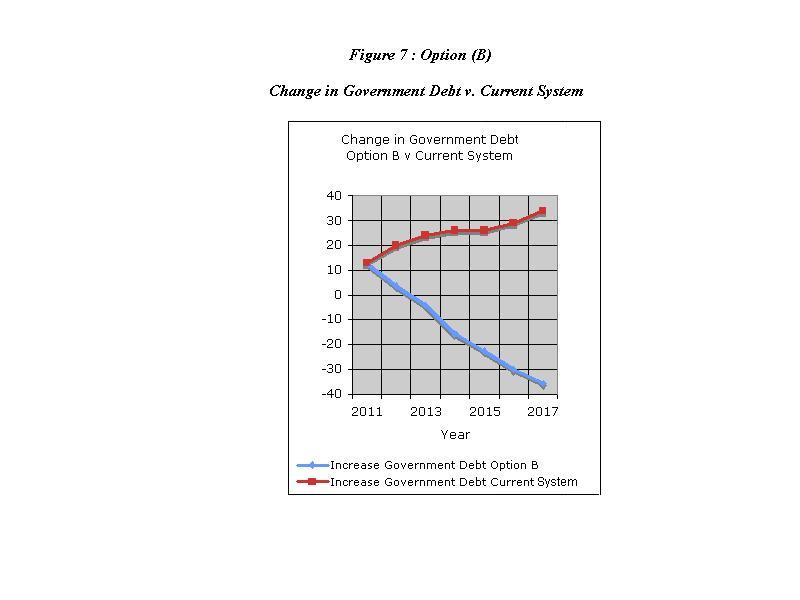

of these proposals is shown visually in Section 6 of this paper.

31

BBC News 25/10/10 “Mervyn ponders abolition of

banking as we know it.”

The second “leg” of

Option (A) involves at least one new instrument to manage the current account

deficit and the exchange rate. One possibility is to use an automatically

collected foreign transactions surcharge or FTS, which would also be simple to

administer 32. It has only very

rarely been used in the past 33. Introducing a financial instrument such as the FTS is essential if

offshore borrowing and interest costs are to be reduced. Orthodox monetary

policy efforts to manage the exchange rate and current account using the Official

Cash Rate (OCR), insofar as it has sought to manage them at all, have failed,

in part because financial deregulation has facilitated unrestricted speculative

capital flows 34. Some

economists may object that a unilateral FTS will not work because banks and

traders can evade the surcharge by “bundling” transactions and reporting, say,

only a single daily settlement sum, or else trading in

32 The “beauty” of FTS

is that it applies to outward capital flows, not inward capital flows. Moreover,

FTS is not a “restriction” on capital flows, it is a temporary universal tax on

all outward transactions.

33 It was used

successfully in

34 Note deleted.

35 Setting the

parameters for that regulatory framework falls beyond the scope of this paper.

A broader issue is

whether a foreign transactions surcharge would contravene international

financial agreements. There are provisions in the relevant international World

Trade Organisation (WTO) protocols for countries to protect their balance of

payments. Relevant material is contained in the Appendices to this paper.

The GATT legal text, Article XI clause 1 (Appendix 5) appears to specifically

permit taxes to be applied. Provision of funding is a service that falls under

the GATS protocols (Appendix 2).

The so-called policy

“trilemma” referred to in the paper “The interest-bearing debt

system and its economic impacts” is important to any debate on the

FTS. Obstfeld (1998) put it this way: “In most of the world's

economies, the exchange rate is a key instrument, target, or indicator for

monetary policy. An open capital market, however, deprives a country's

government of the ability simultaneously to target its exchange rate and to use

monetary policy in pursuit of other economic objectives”.

If the current

account is to be managed, some form of exchange management will be required. To

restructure the financial architecture as proposed in this paper, a tool such

as the FTS will have to be inserted at the currency exchange interface. Failure

to do so would condemn the world to economic ruin. It is now widely, if not yet

universally, acknowledged the current economic system is deeply flawed as

suggested or implied in recent articles from the Bank for International

Settlements, the World Bank, and leading economists like Joesph Stiglitz and

Paul Krugman.

The exchange

management instrument(s) would apply to all outward exchange transactions, not

just outward capital flows.

The proposed FTS is

not a tariff or trade barrier of any kind. Nor is it a restriction on capital

flows as such. It is a temporary because it will apply only until the net

foreign debt has been repaid and it is a fiscally neutral tax on all

outgoing exchange transactions. Moreover the FTS would be variable. It goes no

further than the specified objective of balancing the current account and

progressively repaying the accumulated net foreign debt. This proposal mirrors

the historical position that existed prior to the removal of the

Financial receipts

from the surcharge would be used to offset a corresponding amount of domestic

taxation (for example by reducing GST), to make the surcharge tax-neutral apart

from any receipts put towards foreign debt reduction. Its intent is to correct

the current account, part of the balance of payments as defined in the legal

WTO, GATT, GATS texts, by removing the existing subsidy enjoyed by those

engaging in foreign currency transactions at the expense of those who do not

engage in such transactions or engage less in them. Those using foreign

currency in

The overall saving

to the wider New Zealand economy from the introduction of an FTS is likely to

be more than the annual current account deficit itself 38. In addition to the

obvious reduction in interest costs and the amount of foreign debt there are

consequential downstream benefits to the economy of a country like

A foreign

transactions surcharge would cause the exchange rate to fall towards a stable

base level allowing exports to increase and imports to decrease, providing a

more even playing field for local manufacturers and producers 39 .

36 Under the gold

standard, capital flows do not appear to have been directly restricted, but

they were influenced by the exchange rates fixed from time to time.

37 The famous Bretton

Woods meeting was where the basis for the post World War II financial

architecture was agreed among the allied powers. The British position was

effectively vetoed by the

38 Each 1% in interest rate alone

represents nearly NZ$ 3.1 billion per year on a domestic credit of around NZ$

310 billion, including net foreign debt, as at March 2011. Estimating the

actual economic effect of FTS is outside the scope of this paper, but,

according to the System of National Accounts, every dollar off the current

account deficit is a national “saving” before taking into account other

downstream benefits.

39 Rose (2009) notes

that, historically, exchange rates have relatively little influence on imports,

but it is likely that the FTS would act more directly on the import sector

because it is visible, being drawn directly from bank accounts.

Introduction of the

FTS policy could allow the removal of all remaining tariffs and subsidies in

the

The FTS can also be

seen as a correction designed to offset the unmanaged volatility in

There would be a

substantial reduction in interest rate premiums as the current account is

brought under control, foreign debt repayment begins and inflation is reduced

to very low levels. Rose (2009) notes: “Effectively the market is pricing

country and/or currency risk into national interest rates”. On the other

hand, the

40 It might be

possible to have a separate FTS rate for speculative capital flows. This paper

arbitrarily assumes a single rate and that speculative flows will cease.

41 Source: Reserve

Bank of

42 New Zealand National Accounts

year ended March 2009.

43 The outward

payments would fall from their present level and inward receipts would

increase.

44 This could be done

through some form of tender process. The worked indicative example for

Option (B) at Table

45 The Keynesian

transfer problem implies the current account should go far enough into surplus

to meet all transitional foreign investment claims, though that might be

optimistic in the short term.

46 Rather like the

47 On the other hand,

debtor countries could be better off “biting the bullet” and getting their

financial restructuring out of the way. Since the volume of exports cannot be

rapidly increased, the FTS must rely on changing the relationship between the

NZ$ value of exports and imports.

48 The carry trade is the practice

of transferring deposits from countries where deposit interest is low to

countries where deposit interest is high(er).

The share of the

Banks would quickly

unwind their dependency on foreign debt when the funding rate falls below what

they are paying offshore. Transitional arrangements may be needed to

promote the replacement of foreign funding with domestic funding.

The comparative

example given in Section 6 offers the possibility of foreign debt monetisation

but does not incorporate it as a major feature. Domestic currency

monetisation could change

Some academic

literature supports the need for some form of foreign exchange management to

correct the balance of payments and the current account. Similar policies, such

as “pegged” exchange rates, have been widely used by major countries around the

world, including

Preston (2009)

argues that the levels of the

Option (A) as it is

outlined above is much broader in scope than

OPTION (B): AS OPTION (A) BUT

WITH SOME NEW GOVERNMENT FUNDING REQUIREMENTS PROVIDED BY THE RESERVE BANK.

Under existing policy,

government borrowing is raised at interest through the private banking

system. In New Zealand, government and local authority debt, while less

than that of many other developed countries as a proportion of gross domestic

product, is now rising quite steeply after having been stable in recent years.

Central government debt servicing costs are projected to be about NZ$ 2.4

billion in the fiscal year ending June 30, 2011 49 and as much as NZ$ 4.5

billion by 2014. Because of the recent recession in

The New Zealand

Reserve Bank Act specifically provides the power to the Reserve Bank to issue

currency and to act as Banker to the Government 50 so there is no reason existing

policy cannot be amended to instruct the Reserve Bank to responsibly issue

electronic cash currency credits (to be called E-notes in this paper) 51 and low interest or even

interest free debt to replace debt presently borrowed from commercial banks;

and for the government of the day to spend that new money and debt into

circulation 52. Brash

(1996) noted (page 5) that:

“(T)he Reserve

Bank Act does not prevent the government from choosing to override the price

stability objective chosen for monetary policy by Parliament, but it does require

any government choosing some other objective to tell everybody that that is

what their new instruction to the central bank is.”

This proposal does

NOT seek to change the inflation objective, but rather strengthen it and add

additional viable objectives to manage debt expansion and the exchange rate to

permanently stabilise the nation’s financial system. The present Governor

of the Reserve Bank of

“ (T)he extent of the

recent financial crisis showed that inflation targeting monetary policy was not

sufficient to guarantee comprehensive macroeconomic stability” 53.

49

50 See especially

sections 5,8,9,25,34,39.

51 Since E-notes

become part of the circulating deposits in bank accounts just like deposits

arising from debt, their speed of circulation will, unlike notes and coin in

circulation, have the same aggregate speed of circulation Vy in equation (3) as debt that

can only be used once because once used it must be repaid. Vy might be expected to undergo a gradual

structural increase as the proportion of E-notes to debt increases.

52 Some low cost debt

might be used as well as E-notes to facilitate repayment (amortisation) of

capital goods. If debt is not used for capital expenditure, capital

repayments would have to be taxed out of circulation, otherwise there would be

an inflationary build up of deposits in the banking system. To cope with that,

tax rates would need to change whenever there are substantial changes in the

rate of capital investment.

53 Allan Bollard, speech to Canterbury Employers’ Chamber of Commerce Friday 29/1/2010.

Such views suggest

that despite the historical reluctance of central banks to test new policy

concepts, additional instruments could enhance a country’s growth prospects and

macroeconomic stability if they are properly designed, while still maintaining

tight fiscal responsibility and inflation targets.

The proposed

government-issued debt does not have to be interest-free. It could even

be issued at the same interest rate as private debt. In that case any profit from

the bank spread would accrue to the government through the Reserve Bank rather

than to private banks. Once the government has spent the new funding into

circulation it would become deposits in the banking system just like all other

deposits and would be available for lending intermediation by the private

banks.

Some experts

believed in the past that Reserve Bank funding would be inflationary because it

would increase the available excess reserves in the private banking system the

way government bond issues do (or did) in fractional reserve credit expansion.

Those new excess reserves from creation of new debt funding by the Reserve Bank

would then encourage (further) expansionary growth of private bank debt. When

direct Reserve Bank funding was used in the past, particularly during the

1930’s world depression, there was a vast reservoir of unused capacity in the

economy, which meant the additional reserves did not create inflation. The

situation in Option (B) is quite different.

In Option (B), any

surplus excess bank reserves resulting from new bank deposits arising from the

issue of central bank E-notes or credit would be sterilised by adjusting the

supplementary reserve ratio established for the banks under Option (A),

removing any possibility of inflation arising within the domestic banking

system.

The debt model

derived from the modified Fisher Equation of Exchange referred to above

requires an extra term to be added to account for E-note injection because

E-notes are not subject to repayment and, unlike debt, can be used repeatedly

as long as they remain in circulation 54.

Some advantages of central

bank funding of new government expenditure include:

-

It is cheaper than private funding and can be costless, saving billions of

dollars each year in interest costs compared with the present system, and

savings compared with Option (A), too 55.

-

Existing privately issued interest-bearing government debt can be progressively

retired as it matures and replaced with publicly issued interest-free debt or

E-notes.

-

It is easier for governments to prioritise productive resource allocation in

the public sector.

-

Direct public taxation can be gradually reduced as the economy grows.

54 E-notes and

existing cash are provided for in the general expression of equations (4) and

(5) (Manning 2009, referenced footnote 2, page 25) which includes a term E0*Ve0 where E0 is the

electronic cash in the system and Ve0 is its speed of circulation.

Ve0 is thought to

be the same as Vy.

55 The saving is less

under Option (A), because in Option (B) the effective net costs of government

debt is almost zero. In Option (A), at 2.5% bank spread plus 0.5% deposit

interest the cost of $40 billion of government debt would still be NZ$ 1.2

billion.

The first two

points are self-evident. The third is more political. It concerns the role of

government in the economy and is outside the scope of this paper. However, the

government could choose to use unutilised resources in the economy for

infrastructure projects, investment in health and education or other productive

investment.

If the New Zealand government

were to inject, say, a net NZ$ 0.5 billion/year of direct Reserve Bank funding

into the economy transaction accounts My, total government debt would,

in the long term, still never exceed 6% of GDP, still lower than most other

developed countries 56. There

is no particular reason to keep government debt to any arbitrary figure,

because its use is almost costless.

One of the major

concerns among economists about the vast government debt growth in the United

States 2008-2010 is that it has been borrowed through the private banking

system without any means other than the Basle III capital adequacy requirements

to constrain debt expansion. Some of that borrowing has served to cover bank

losses against loan defaults. There has been little new lending to the

productive economy so there is no inflation (yet). “

56 In Option (A), the

assumed growth was $ 9 billion/year. If the government injected NZ$ 5

billion/year out of that $9 billion increase in GDP, the total government

injection in the long run could not be more than 5/9 of the total debt, or less

than 56%.

57 The worked

comparison in Section 6 shows public debt could, under Option (B), potentially

be fully repaid quite quickly.

58 NZ$ 0.5 billion (My) * 18 (Vy ) * say, NZ$ 0.4 billion tax /total gross government

revenue (budget 2010) of NZ$ 70 billion= 5%

59 NZ$ 0.5 billion * Vy * 18 /GDP NZ$ 186

billion = 4.8%.

OPTION (C) VESTING ALL CREDIT

AND MONETARY ISSUE IN A PUBLIC RESERVE BANK OR CREDIT AUTHORITY AS RECOMMENDED BY

UNITED STATES PRESIDENT LINCOLN TOGETHER WITH THE FOREIGN TRANSACTIONS

SURCHARGE OF OPTION (A).

As recently as

World War II, a large part of war expenditure was funded from government debt

rather than from taxation 60. Domestic consumption was reduced through the issue of War Bonds,

price controls and rationing. In many cases the total public debt was far

higher in countries like

Key underlying

issues when deciding what levels of public debt are acceptable are the price of

that debt, and the ideological concept that private debt is “good” and public

debt is “bad”. As long as interest rates are used as the primary, if not

the only instrument to manage inflation in modern economies, the cost of public

debt purchased from the private banking system is likely to be high and

volatile. That in turn creates uncertainty in bond markets and leads to

recurrent financial crises.

Private banks

oppose public funding of public debt because they want debt levels to expand as

quickly as possible to increase their profit. Their profit comes from the

spread on their loans, which is the difference between the interest they charge

on their loans and the interest they pay to their deposit holders. As a general

rule, the more debt there is the more profit the banks make. In the recent

deregulated lending environment the large (mainly US banks) went beyond their

existing physical debt base to create a vast pool of virtual debt in the form

of complex derivatives from which they also sought to profit. The system

collapsed because the productive economy could no longer fund the profit

expectations of the bloated investment sector 61.

60 War expenditure has

been a common cause of sharp increases in public debt for centuries.

61 These matters will

be discussed fully in a later paper.

Public credit and

money creation will tend to reduce the capacity of the private banking system to

increase total debt in the financial system. That is essential because

the present financial system has failed to adequately manage the exponential

growth of debt. Slower debt growth could reduce the banks’ future profit

growth, but it will not affect their profit margin because the proposals in

this paper address the interest rate on deposits, not the bank spread.

Under Option (A)

the growth of bank profits is subject to the relatively minor restraint that

less new debt will be needed. Under Option (B) the growth of bank profits might

be reduced further depending on the amount of public E-note and debt issued. In

both Options (A) and (B) the nominal reduction in debt creation is offset by

much higher economic growth as well as minimal inflation and, possibly, lower

taxes. The economy will grow faster, so there will still be some growth in bank

deposits and some growth of bank profits.

Option (C) is

different from Options (A) and (B) in that the private banks would operate as

intermediaries in the financial system rather than issuing new debt themselves.

Under Option (C) the government would issue all the new E-notes and debt needed

to achieve optimal economic activity by spending them into circulation. The

money would then be deposited into the banking system in the normal way and the

private banking system would operate like a savings bank, redistributing

deposits to borrowers using existing lending criteria but with lending rates

limited as set out in Options (A) and (B).

The debt model

(equation (3) above) supporting this paper shows that to achieve 5% growth in

New Zealand the new debt issue (based on March 2010 figures) might be about NZ$

4.6 billion. Debt growth would be a lot less than recent increases in domestic

credit reducing the growth of the total debt base by about one sixth after

taking into account the annual current account deficit. The required reserve

ratio of the private banks will gradually increase as more public debt is

introduced to the system, until it ultimately reaches 100%.

Public credit and

money issue will enable the domestic banking system to operate in a high

growth, low risk, low interest, low inflation economy while retaining its

existing profit and growth path except that the debt growth exponential will be

lower because growth is tied to the productive economy instead of being

inflated by deposit interest.

A consistent growth

rate of 5% could be possible in

The management of

outward financial flows proposed in Option (A) could dramatically change

domestic manufacturing opportunities.

Under the present

economic and financial structures, without retraining, people displaced by

"cuts" in the service sector have nowhere to go except the

unemployment queue. Adjustments being imposed by restrictions on public

spending around the world today are brutal, to say the least. They are

also misplaced. Without changes of the kind set out in this paper, the United

Sates and other developed economies are not just eating their own economic

tails. Most of their people are also being asset stripped through the rapid

transfer of wealth to the holders of bank deposits by way of unearned income

from deposit interest. Unless exponential debt growth is contained, the

future must be one of worsening economic crisis.

62 The figures are for 2009 taken

from the CIA “World Factbook”. Other organizations also provide sectoral

breakdowns and the numbers do vary from one to the other.

OPTION (D) : INTRODUCING

FORMAL LOCAL CURRENCY SYSTEMS.

There are many

local currency systems in use around the world and quite a few have been

proposed to assist development in areas where there is little or no national

currency available and few current options to initiate local development

programs 63. Such

proposals are not intended to replace national currency or national development

but to supplement the growth of useful local economic activity where it would

otherwise be unlikely to take place.

63 A highly developed

regional development model with a raft of fully detailed applications can be

found at the website of the Dutch NGO Stichting

Bakens Verzet (Another Way). Details of the nature and organisation of local money

systems in integrated development projects can be found in sections 3 and 4 of

the financial structures section of the course for the Diploma

in Integrated Development there.

Almost all local

currencies have the single outstanding characteristic that they fall broadly

within Option (C) of this paper; that is, they are mostly co-operatively owned

interest free, self-cancelling monetary systems. Typically, from a modelling

perspective, they conform to a simple dynamic production cycle 64 where participants operate as

entrepreneurs. Any debt incurred during the production phase is sterilised when

the product is sold leaving the supplier with an operating credit and the

purchaser with a corresponding operating debit. There is then a reciprocal

imperative for those with an operating deficit to contribute to economic

activity within the system. There is no net systemic debt. Where

participants default on any residual debit balance they may have when they

leave the local currency group, the debit is effectively offset by the goodwill

of those holding the corresponding credit balances, and vice versa.

Local currency systems are

designed to work in parallel with the national economy, and to supplement it,

not supplant it.

The dominant

advantages of local currencies are that they avoid financial leakage whereby

national currency incomes are drawn away from local communities, they stimulate

community cohesion and local development, they strongly encourage personal

independence, responsibility and participation, and they induce useful economic

activity that would otherwise not take place, especially among those presently

active in unpaid work.

The overwhelming

disadvantages of most local currency systems are that they are usually too

small to operate as a “market” in any normal sense because they lack the range

of skills and number of participants to provide economic efficiency and choice,

and they cannot be properly taxed without destroying the integrity of the local

accounting systems.

The twin keys to

future success of local currencies in developed countries are that they are

acceptable for the payment of taxes, thereby greatly encouraging participation,

and that the local currency activity can in turn be taxed on a broadly similar

basis to national economic activity. In most cases neither of these crucial

elements is presently satisfied.

Option (D) provides

for formal recognition of the positive role local currencies can play in

economic and community development by encouraging the participation of

government agencies, particularly local and regional government, whereby local

currency is accepted for (at least some of) that part of taxation that

territorial authorities expend on local productive output. Territorial

authorities could even be encouraged to become the driving force of local

currency initiatives. While the local currency initiatives would remain

local, a nationwide “EFTPOS” style accounting system would need to be

introduced so that local currency trading can be measured and taxed. To

accomplish this, each local currency member could be issued a “local currency”

debit card that could be accessed through an EFTPOS terminal or similar system 65. The card

would carry two separate balances: the local currency balance and a separate

national currency balance. When a credit transaction is entered (that is, an

income), a national currency tax, essentially similar in nature to GST, but set

by parliament from time to time at a level it decides is appropriate 66, would be deducted from the

seller’s national currency balance and the full local currency credit would

then be credited to the seller’s local currency balance. If there is

insufficient national currency balance on the seller’s card, or if the

purchaser is operating outside the authorised local currency debit range, the

transaction would be declined, just as EFTPOS transactions are declined now

where there are insufficient funds to meet the payment 67.

The process

described above also theoretically allows centralised entry of transactions at

a local level by authorised personnel. In that variation, the transactions

would be recorded by notes or by cheques68. The transaction accounts would still be the same but

it might not be necessary for every participant to have a separate card.

Some method would still be needed to enable individual accounts to be

downloaded with national currency so the tax payments can be made. There

appears to be no particular technical reason why the “local-currency” card

couldn’t also function as a normal EFTPOS debit card, and likewise no obvious

reason why existing debit cards couldn’t be modified to incorporate the local

currency features. This paper keeps the two systems separate on grounds of

public perception: most of those participating in local currency

transactions will be keen for others to see they are using local

currency.

It is likely that

local currencies used as outlined above significantly increase measured gross

domestic product and economic growth. As long as the local currency tax rate is

set to encourage local activity without measurably inhibiting growth in

national currency activity 69 the local currency option must benefit all parties,

including the government of the day. Used in the manner set out above, local

currencies could become an extension of Options (A) to (C).

64 Manning L., “The interest-bearing debt system and its economic impacts”,

Section 3, Figures 1 and 2.

65 Eftpos facilities

are already becoming quite common at local markets in New Zealand, and can be

held on a group basis – the proposal is not suggesting that every member

necessarily have an Eftpos terminal – but it is technologically possible for

the EFTPOS programs to be amended to enable local currency payments to be

processed from any existing terminal (for example 1 swipe and entry

“from”, another swipe and entry “to”) There are also already several mobile

phone platforms in use (Kenya, India, US) for making small payments.

66 The national

currency debit would also include any formal money EFTPOS processing costs.

67 Should, in the

future, any Universal Basic Income (sometimes called Guaranteed Minimum Income

or GMI) be introduced, the proposal provides a ready-made payment route since

everyone would have such a local currency debit card, and the formal

money UBI could be paid automatically onto the card. A full plan for the

introduction of a GMI into

68 This paper does not

consider Option (D) from the point of view of system security, that is, for example

the risk of a lengthy electricity failure or viral or other corruption of

network electronic processors. Such systemic risks are very low and common to

most modern economic activity.

69 If the tax rate is

too low it will draw activity away from the national economy into the local

economy reducing gross tax revenue, whereas the intent of Option (D) is to

enhance both economic activity and total gross tax revenue.

4.

EQUITY IN SOCIETY.

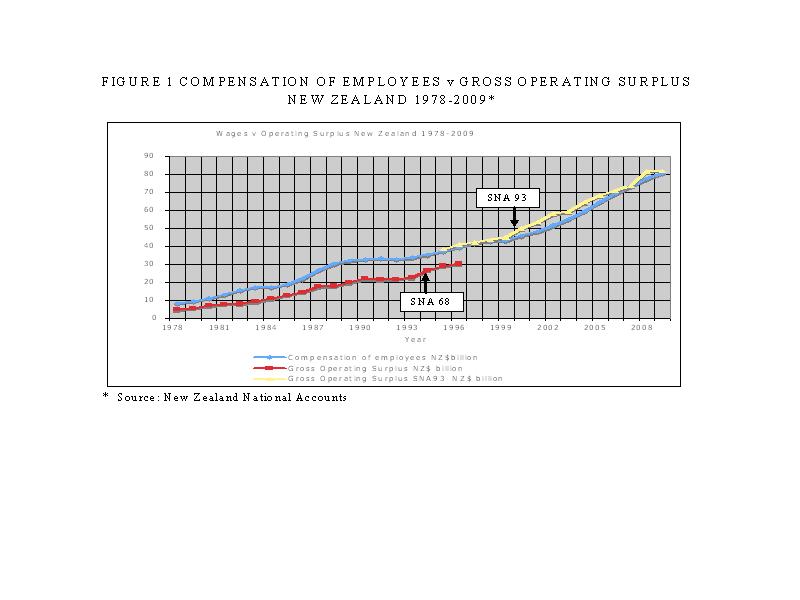

Figure 1 shows compensation

of employees plotted against the operating surplus for

Click here to see :

FIGURE 1 COMPENSATION OF EMPLOYEES v GROSS OPERATING

SURPLUS NEW ZEALAND 1978-2009.

{kind=link}

However, the

relationship between employee incomes and gross operating surplus can mask

dramatic changes in equity among income groups. One common way of measuring

income equality is by using the Gini coefficient 72 . A high score means relative

income inequality and a low score income equality. Over recent decades,

70 The figures have

been amended several times. The discontinuity in the series is due to the

change in the SNA accounting system from SNA68 to SNA93.

71 It remains possible the relationship between the numbers of entrepreneurs and the numbers of wage and salary earners has altered, for example if firms became bigger on average. Such changes would not be disclosed in Figure 1.

72 The Gini

coefficient is developed from the Lorenz curve, which is a plot of incomes

against population starting from the poorest groups in the population.

Wkikpedia provides a good introduction to the Gini coefficient. The Gini

coefficient does NOT typically include investment income.

73 The Gini curve used for these figures was taken from the

NZ Green Party website 19/6/10 because it is reasonably current Various

organizations like the UN and the CIA calculate Gini coefficients which can

vary depending on the way the basic data is compiled.

Poor income

distribution suppresses demand for domestically produced goods and services. People

with low incomes have relatively little to spend on domestic consumption,

especially on services, which make up the bulk of monetised economic activity.

Income concentration encourages relatively high demand for imported “luxury”

products adding to

There are just two

ways to avoid large earned income imbalances. The first is by increasing lower end

wages and salaries, especially minimum incomes. The second way is by

reconsidering taxation policy, not for political reasons but because the

existing income distribution structure has not been working well. Both the debt

model referred to Section 3 of this paper and the analysis in the paper “The Interest

Bearing Debt System and its Economic Impacts” Section 375 show that inflation and growth must be reflected in

incomes for the production cycle to clear. Heavily skewed income

distributions make the process of clearing the market from each production

cycle more difficult. Some people have “too much” (and growing) income in

relation to domestic consumption and many others “too little” (and falling)

income. “Ordinary” employment gets squeezed.

Every economy can

be thought of as having its own physical shape. That shape reflects the degree

of “reasonable self-sufficiency” the economy possesses. Reasonable

self-sufficiency describes how well domestic production matches the consumption

patterns of the population as a whole taking into account its income structure.

The less of its own domestic product an economy can afford to consume and the

more reliant that economy becomes on importing what it needs but does not

produce the more skewed the economy becomes. The more skewed the economy the

more dependent it is likely to be on foreign trade, globalisation, and in some

cases, on foreign debt.

Income distortions

have become structural, especially in industrialised economies. According to

the debt model, increased incomes are inflationary unless they are accompanied

by corresponding increases in productive output. Since the employed workforce

is already producing goods and services, the SHAPE of the economy, the basket

of goods and services produced in relation to incomes and consumption patterns,

will have to change if it is to improve the lot of the people as a whole so

that everyone gets a “fair” share 76. Increasing incomes

without increasing production would just increase prices.

74 This does not

suggest

75 Manning L. “The Interest

Bearing Debt System and its Economic Impacts” Section 3

76 What that “fair”

share is should be a defining political debate in a democracy.

Changing the shape

of the economy means eliminating excessive debt, especially foreign debt, as

discussed in Section 3. It also suggests changing the tax structure to optimise

the options as also set out in Section 3.

Tax structures in

most parts of the world are confusing, antiquated and expensive to run.

They are layered like an onion. New taxes have been added over the centuries as

the means to collect them have become available. They are full of loopholes and

exceptions granted to vested interests of one kind or the other. Governments of

all hues have tended to weight tax law with an eye towards their own perceived

constituencies and re-election. This implies adoption of short-term goals

instead of policies for the long-term benefit of the nation as a whole.

Governments claim to know the importance of goals such as economic efficiency,

research and development, the “knowledge” economy, investment and the reduction

of welfare dependency but they are unable to “walk the talk”. Systemic

constraints have made effective political action to adapt the existing

financial architecture to the needs of modern economies all but impossible. The

basic issues to be addressed are covered in the debt model referred to in Section

3 of this paper and in the paper “The Interest Bearing Debt System and its Economic

Impacts”. The current financial system has become a straightjacket on the

world’s economies as the recent debt “crises” have demonstrated.

In

A flat tax to

achieve tax universality is available to governments that choose to use

it. It is called a Financial Transactions Tax (FTT) 78. FTT is very cheap to

administer. It could easily replace all other forms of taxation except social

excise and environmental taxes such as those on tobacco, alcohol, fuel,

pollutants, and perhaps source deductions on sugars and saturated fats that

contribute heavily to obesity, diabetes and heart disease. Most of the nations’

Revenue Departments could be dismantled. One version of FTT is to deduct the

tax automatically every time money is transferred out of any deposit account

unless the transfer is to another account held by the same account holder.

Savings in downstream compliance costs (government, accountants, lawyers,

business administration), would be substantial 79. The quality of

economic output could be improved. The quantity of output would

play a smaller role in the economy. FTT would considerably increase economic

efficiency, releasing a pool of educated and experienced people for more productive

and useful output 80.

77 GST refers to Goods

and Services Tax. In

78 This is a general

tax, not to be confused with the so-called Tobin, or “Robin Hood” tax

79 Estimation of the

savings is outside the scope of this paper, but could easily exceed 5% of GDP

80 No reflection on

the people concerned is intended – in the present context they are productive

and useful–but in the broadest economic sense their skills could well be better

utilised.

As described above,

the quality of output refers to the real benefit the economic

activity contributes to national and environmental well-being. Reducing

compliance costs and the demand for legal, taxation and policy advice, for

example, would, over time, free more people to do more work that is more useful

to society. The more complicated and controlled society becomes the less

beneficial its economic output will be.

The level of the

FTT is easy to calculate. In New Zealand, for example, the 2010 budget

proposes total revenue of NZ$ 70 billion out of a GDP of, say, NZ$ 190 billion.

Suppose NZ$ 65 billion is to be raised from FTT. This is based on total

transactions in the New Zealand economy of about 1.8 times the GDP or, say, NZ$

340 billion 81. The

required FTT rate is then about 19% (65/340)82. All income is kept until it

leaves the bank account into which it has been placed.

Unlike GST, which

is a “pass-the-parcel” tax on value added, FTT is a layered tax because it is

charged every time money is transferred from a bank account. The more complex a

product is, and the more packaging, transport and storage it needs the more

expensive it will be because there are more payments made before the final

product is consumed. FTT therefore favours local production and local

consumption of local products. Local development will be stimulated. Typically,

exports are sold exclusive of such domestic taxes 83. FTT would be added to

imported goods and services when they are sold just as GST is at present.

The proposed overall

FTT tax level clearly illustrates the hefty tax skew masked by the existing

taxation system that substantially exempts the investment sector from paying

its “fair share” of tax.

Most ordinary

people spend most of their income on basic needs. While those buying a house

will pay FTT 84 on both the house

and on loan repayments, the interest rate under the four options in Section 3

may be less than 3%. 19% tax on the interest and repayments is still probably

less than 1% of their outstanding loan. Their total household financing cost is

still less than 3% interest plus another 1% FTT tax on their interest and

repayments, or 4%. That 4% is much less than the interest most people pay now.

A universal “flat tax” of about 20% considered so desirable by some political

parties in

81 The additional

transactions include such things as intermediate transactions in production,

property and equity transactions, financial transactions, interest, and loan

repayments.

82 The 19% figure

could be reduced to 17.5% with government injection into My of NZ$ 0.5b/year (Option B

above).

83 Consumption taxes are

usually levied under the tax system of the country where they are consumed, not

in the country where they are produced. In any case they are levied on sales

rather than purchases. The exporter is selling and not buying. It might be

practical to strip out some of the FTT costs layered into the export sale price

of the exported goods. That is not recommended because it would add complexity

to an otherwise extremely simple tax system and could make it subject to abuse.

Two of the beauties of FTT are its universality and its simplicity.

84

The tax would presumably be added to the loan

just like GST is added to prices now.

Social transfer

payments from tax revenue to beneficiaries and super-annuitants will still be needed.

They may need to be extended a little because the reduction or removal of bank

deposit interest as proposed in Section 3 will affect people, especially

retirees, who currently depend on interest income to supplement their pensions.

Options to deal with these issues are outside the scope of this paper. One

option is to provide insurance or guarantees for investments in new businesses

and deposits with qualifying non-bank deposit taking institutions. If the

existing tax system is, for the time being, retained, retiree depositors could

be compensated for loss of interest income by exempting some of their pension

from income tax.

Case management for

beneficiaries other than pensioners has always been fraught with difficulty,

and that will, unfortunately, not change unless a universal basic income (UBI) 85 (Manning, 2010) is introduced to replace the plethora

of individual entitlements that characterise “modern” social transfer systems.

In the meantime, earned incomes will still have to be linked to social

transfers with the on-going intrusion of eligibility qualifications.

85 A UBI would

nominally increase the FTT closer to 26% unless it is accompanied by a wealth

tax. Assuming the UBI is made very close to “social-transfer neutral”, the 7.5%

difference in FTT would, in aggregate, be “refunded” as UBI to those who have

paid most of it. The net income redistribution would then be roughly similar to

what it is now, but without any of the present barriers, stigmas, or government

intrusion in peoples’ lives and without the massive compliance costs involved

in the application of social legislation. Manning, 2010

provides a fully worked plan for a Guaranteed Minimum Income for New Zealand , incorporating a

wealth tax of 1% and a small E-note injection.

5.

IMPACTS ON THE PUBLIC SECTOR.

This paper does not

argue for or against more or less public sector involvement in the

economy. The proposals are “public sector neutral”. The debt model shows

that the debate about the public sector should not be about its size, but about

the quality of its economic output compared with that of the

private sector for the same amount of economic input. When the public sector is

more efficient it should be used. It is easy to be ideological about the role

of government with one side wanting to reduce government and open more of the

economy to private profit and the other wanting to improve “people power” or

social equity.

Whichever side of the

ideological fence is chosen the impact on government from the proposals

contained in this paper is profound. They should enable government to function

more effectively. There will still be a tax system and there will still be

income redistribution, public welfare and (in

The only effect of

the proposed changes to the banking sector will be that the exponential growth

of debt will fall (in

Looking at the

options (A) to (D) in relation to the Pubic Sector:

Option (A) merely

reinserts a supplementary reserve requirement on the banking system that

enables the central bank to manage the quantity of new debt by a means other

than the domestic OCR (official cash rate). The reserve requirement allows the

price of domestic debt to remain cheap so deposit interest can be reduced or

removed in much the same way debt expansion used to be managed before the oil

shocks of the 1970’s. If Option (A) is to be successful, the foreign exchange

interface has to be carefully managed as set out earlier in this paper. Capital

flows will be managed to bring the current account into balance and, over time,

enable net foreign debt to be repaid. The reduced demand for foreign debt

should permanently reduce the Trade Weighted Index (TWI) to a stable lower

level consistent with a balanced current account and much lower interest rate

structure. Permanently lower exchange rates will increase profits in the export

sector. The government may have to find ways to sterilise some of those profits

to avoid inflation in the domestic economy. One way to do this would be to offer

attractive national development bonds to stimulate increases in productivity

through investment in new industry and research, and similar schemes designed

to direct the additional income into national productive use. The foreign

transactions surcharge (FTS) will stop the “carry” trade and prevent it

from being reversed when domestic interest rates fall to very low levels.

Option (B) provides

the public sector with more leverage over its own activity to the extent there

are unused or under-utilised resources available to increase productive

economic output. In addition to making use of available resources, public

credit can be extended to provide funding for economic growth and to refinance

existing government bonds as they mature. Transitional provisions will need to

be introduced to allow for the supplementary reserve ratios to steadily rise as

traditional new bank lending through debt expansion is reduced and lending of

deposits through bank intermediation increases.

From the government

and public sector point of view, Option (C) is conceptually different from