NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02 :

13 November, 2009.

Edition 05 : 09 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org.

NEW Capital is debt.

NEW Comments on the IMF (Benes and

Kumhof) paper “The Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

SUMMARY "THE

RIPPLE STARTS HERE"

1694-2009: FINISHING THE PAST

Paper presented at the 50th Anniversary Conference New Zealand

Association of Economists (NZAE) 2nd July, 2009

by Lowell Manning.

..............................................................

"The Ripple Starts Here" revises the Fisher Equation of

Exchange first put forward by Irving Fisher in 1911.

The original Fisher equation said simply that the amount of money M in

circulation times its speed of circulation V must equal the gross

Domestic Product PQ where P is the overall price level and Q the

total volume of goods and services produced.

MV = PQ

In Irving Fisher's time his equation could not be easily checked because

much of the information needed to do so was unavailable.

He spent a good deal of his subsequent career developing indices and

associated data bases to better measure the economy.

In Fisher's day most economic transactions contributing to the economy

were still made in cash and his equation took no account of either Domestic or foreign debt. These days in

"modern" developed economies almost all transactions are debt

based and cash is all but irrelevant.

****************************************

The debt model presented in the paper changes Irving Fisher's

equation to a debt-based equivalent;

MdVp = PQ +

(Ms + Mv)Vp

Where Md is the total debt in the economy (each dollar of debt is a

dollar of money somewhere), Vp is the speed of the productive debt

giving rise to PQ, Ms is the accumulated unearned interest on all bank

deposits, and Mv is debt borrowed for speculation.

In the debt model Vp must be 1, because debt can only be spent once. The

model can be visualised as millions of separate transactions

where the money to produce the goods and services is borrowed during the

production phase and then repaid when the product is consumed.

The revised debt version of the Fisher equation of exchange then reduces

to:

Total debt Md = PQ + (Ms+Mv)

As a first approximation Md is very nearly the country's

Domestic Credit plus its accumulated Current Account Deficit

(In the paper, the accumulated Current Account Deficit is the total of

all the annual deficits since 1954).

Ms is the accumulated interest paid by the productive sector to the

investment sector as unearned income.

Ms is really the seigniorage of the modern debt economy that began with

interest paid on unproductive debt by the English Crown to the directors of the

Bank of England in 1694. That debt and the associated

introduction of fiat currency (banknotes) allowed the Crown

to avoid politically dangerous tax increases to pay for its

war costs. Ms broadly represents the "gap" so often

referred to in monetary reform literature.

In

exponentially at 8.6% per year.

Ms is inherently inflationary because, leaving aside any productivity

changes, it means more and more debt has to be used for the same

amount of production. In practice the productive sector usually

borrows the extra debt each year to fund the unearned income and, by and

large, passes on in its prices to consumers any change in its

resulting costs.

Mv is the infamous investment "bubble" that grows and decays

during each business cycle. When times are "good"

the banks lend extensively to investors directly on the assumption that

next week's investment sector prices will be higher than this week's

prices. The banks do this because they increase their profit if

they lend more.

Mv bubbles are typically

liquidated during recessions and the year or two after they end.

In the revised Fisher equation, Md, PQ and Ms are readily available from

statistics, and that means the bubble Mv can for the first

time, be accurately quantified.

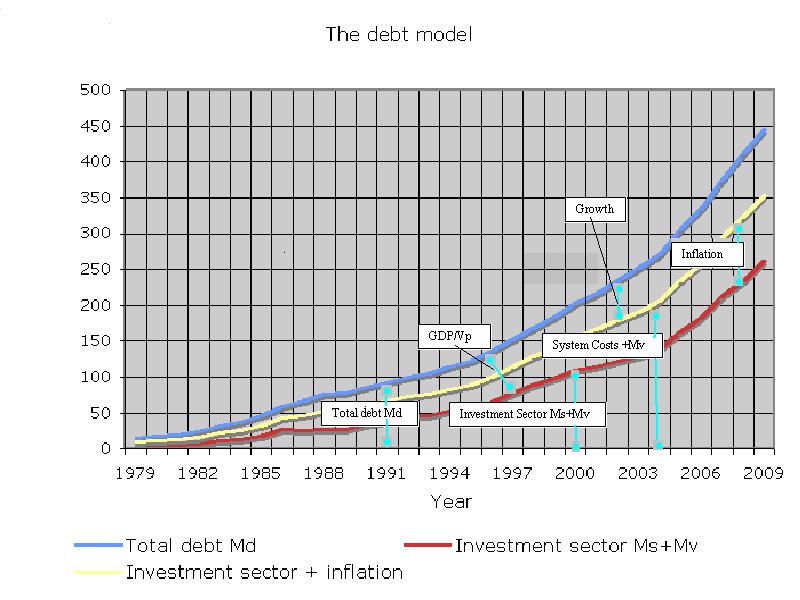

Click to see The new debt model

for New Zealand 1979-2009.

{kind=link}

The first and most

relevant feature of the model is that all the curves are

exponential. To keep afloat, the debt economy is locked into

exponential growth of debt and GDP.

The second most relevant feature is

that the exponential for the investment sector Ms (11.2%) is

much greater than that for the total debt Md (8.6%). That

means present and past monetary policy necessarily produces a rapid

transfer of wealth from the productive sector to the investment sector.

Wage and salary earners are fundamentally disadvantaged relative to those

with deposits in the banking system who receive a "free-lunch"

in the form of unearned income merely because they have those

deposits. Producers get ever less while non-producers get

more and more. There is a large, structural and on-going transfer

of wealth taking place from the poor to the rich in society. In the

present system that transfer in wealth can only be offset through

large-scale income redistribution.

The third most relevant

feature is that the current financial "architecture" is quite

unsustainable. Economic "crashes" become unavoidable as

investment sector expectations literally drown the ability of the

productive sector to satisfy them.

The model suggests the only way to remedy that fundamental

contradiction (assuming we persist with the current system) is for the

investment sector to expand at the same rate as the productive economy.

That in turn means that both the price and quantity of new debt have to

be managed by the government or the reserve bank .

Centuries of evidence show that private issue of debt for profit is

diametrically opposed to such price and quantity controls. Banks earn

more by lending more.

The most recent and classic case is the "meltdown" in the

irresponsible lending to patently uncreditworthy customers.

Such "pass the parcel" transfers of toxic debt

accentuated the underlying

systemic risk instead of reducing it. On such grounds alone there is a

powerful case for public control of the issue of new debt (and money in

the form of electronic cash) and public control of deposit interest

rates.

.........................................................

The debt model offers valuable insights into other areas of major

interest to economists.

First, It provides a specific and rational definition of recessions and

depressions. A depression occurs when the change in the total

debt over time is less than what is needed to service the unearned

interest that has to be paid to the investment sector Ms plus any

increase in speculative investment Mv; that is, when there is no

provision for either inflation or growth. A recession occurs when

the change in total debt over time is less than what is needed to service

the financial system costs, being the unearned interest that has to be

paid to the investment sector Ms, plus speculative investment Mv, plus

inflation.

Secondly,

billion higher than it otherwise would have been, and savings and wealth

in the country about NZ$ 100 billion lower. The paper introduces the

concept of system liquidity, Mcd, being the GDP less the accumulated

current account deficit. Mcd represents transaction account

balances plus earned savings. The paper shows Mcd is dangerously low in

Finally, in the absence of tax or other incentives to encourage

traditional savings, there is an inherent conflict of interest

between increasing productive GDP output and households still

holding debt. Economic efficiency will usually induce households to

retire expensive debt instead of saving. In the debt model debt

retirement reduces economic output.

............................................................

The debt model does not, of itself, distinguish between "good"

and "bad" GDP but it recognises implicitly that new debt

creation should focus on productive activity. To achieve this there

is good reason to reserve to the government the issue of new debt, with

that debt being spent into circulation in the form of investment in

education, health, research, infrastructure and business development.

Following first use of new domestic debt by the government the

corresponding deposits would appear in the banking system from where the

banks would on-lend it according to monetary policy guidelines

published from time to time.

In its 78th annual report (p137) the Bank for International

Settlements (BIS) wrote of the current turmoil in the world's financial

centres "A powerful interaction between financial market

innovation, lax internal and external governance and easy global monetary

conditions over many years has led us to today's predicament."

Presently the financial system itself is structured to not only allow,

but to encourage those human and institutional failings to which the BIS

properly refers. Those failings are largely driven by self interest and

greed that are part of human nature. Since human nature is unlikely to

change, the world financial architecture needs to be remodelled to keep

sticky human fingers out of the global money pot.

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org.

NEW Capital is debt.

NEW Comments on the IMF (Benes and

Kumhof) paper “The Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English edition, Peter Owen,

![]()

This work is

licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence.