NGO Another Way

(Stichting Bakens Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 05: 08 August, 2011.

Edition 07 : 09 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Information on monetary reform :

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE RIPPLE STARTS HERE

1694-2009:

Finishing the Past

By:

manning@kapiti.co.nz 19B

Version

4 18/05/09

Key

words: Debt, Debt model, Economic

theory, Financial System, Fisher equation, Friedman, Inflation, Irving Fisher,

Keynes, Keynesianism, Macroeconomics, Macroeconomic model, Mechanics of debt,

Monetarism, Savings, Economic growth,

SYNOPSIS

This

paper offers a definitive statement of economic activity to replace

Keynesianism and Monetarism. It shows why both the main economic theories of the twentieth

century have failed and what to do about the world financial situation. The

work amends the Fisher equation of exchange (MV=PQ) to allow for structural

changes in the financial system that took place after the Bank of England was

set up in 1694. An economic debt “model”

demonstrates the underlying mechanics of private debt-based banking and the

relationship between the productive and investment sectors. The “model” is

definitive in that it describes actual economic activity. It is used to provide

an historical profile of the

INTRODUCTION

There has long been a

substantial theoretical disconnect between financial and monetary policy and

economic behaviour in the real world.

Recent world events show how limited economists’ understanding of the

mechanisms underlying the monetary policy has been and still is. The basic

mechanisms at the heart of the “modern” financial system itself have never

successfully been put into a logical framework that is robust enough to allow

the underlying relationships to be quantified.

One effort to do so was

provided by Irving Fisher in 1911[1] in his well-known

equation of exchange that takes the form:

MV = PQ (1)

or M= PQ/V (2)

Where: M = the amount of money in circulation

V = the speed of circulation of that money; the

number of times M is used over a given period T

P = the

price level of goods and services an economy produces during time T

Q= the

monetised quantity of goods and services an economy produces during time T.

The product PQ is

what is known today as Gross Domestic Product or GDP. At first sight, the

Fisher equation seems to be self-evident. People have to be able to produce and

exchange goods and services. To the

extent money is used to do this, the total produced must bear a relationship to

the amount of money and the frequency with which it is used.

Verifying the

Fisher equation of exchange, until now, has been difficult. A few people have

tried to do it[2]. The main difficulties have been to work out

reliable estimates for the variables. Historically, only the price level P has

been known within a reasonable margin of error, despite the fantastic work done

by researchers around the world[3].

The relationship presented

here began with an attempt to address a psychological question. “Has peoples’ hoarding behaviour changed over

time?” The question is crucial to

understanding the Fisher relationship.

For a given quantity of goods and services Q, does the price P change

when the amount of money M changes, or does the speed of circulation of that

money, V, change? Or do P and V both

change?

The crude estimate

of V in

The speed of

circulation, V, appears to have been reasonably constant[7] because it essentially represents a

hoarding function. At any given time, most money was “saved”. It can be

surmised that V is a structural rather than a dynamic component in the Fisher

relationship. The immediate response to a change in the money supply M will be

a change on the production side of the equation PQ. If the change in M is rapid, the response

will be a change in prices P until production and demand adjust to compensate

for the change in the money supply. That’s different from what happens with

fresh produce in the supermarket after bad weather. In that case the money side of the equation

remains unchanged and prices rise because production falls. That happens in the

shops regularly and from season to season.

The speed of

circulation on the other hand appears to require a change in people’s behaviour

toward money, or changes in the way the financial system works.

THE BANK OF

Changes in the

economy began with structural changes in the money supply M made possible

through the creation of new money as debt. When the Bank of England was

established in 1694, the money supply, for the first time, became relatively

independent of the supply of gold and silver.

When a bank issues

a new loan, the loan amount becomes an asset in the accounts of the bank. From

the bank’s point of view it’s an asset because the borrower has to repay his

debt to the bank. The new loan asset is offset by an equal liability for the

bank in the form of a money deposit. Money has been created “out of nothing” by

way of a bookkeeping entry. Of course, the loan has to be repaid over

time. As it is repaid, the outstanding

loan is reduced. Once the loan is fully repaid there is no loan remaining and

no residual deposit. The loan and the new money have both been cancelled out of

existence.

The bank gets

nothing from the process itself. As long

as the loan and deposit remain the same there is no profit to the bank and no

way for the bankers to become rich.

Instead, the Bank of England shareholders became rich because they

charged interest on their loans.

Interest has been

paid on loans ever since the use of money became widespread thousands of years

ago. People would loan their hoarded savings to someone else and expect their

savings to increase by the amount of interest they received. The borrowers would usually borrow in the

expectation that doing so would increase their productivity or their fortune in

some other way. For example, buying an ox or workhorse might dramatically

increase production from a farmer’s land. The increased production created by

using the ox or the workhorse would more than offset the interest on the

loan. Both parties were better off as a

result of the investment made by using the borrowed money.

The operative word in all this

is “investment”, the use of money to increase production. The problem with the Bank of England in 1694

was twofold. First, the loans it made to

the government were not to increase production but to help pay the war debts of

the crown. Secondly the Ways and Means Act[8] that authorised the

Bank of England provided for a perpetual fund of interest charged on ships’

“tunnage” and liquor duties. Not only

was the loan for current spending instead of investment, it would never be

repaid. The interest would have to be

funded from taxes forever. Since then,

governments have found it very easy to borrow perpetual debt in this way and

its use has increased steadily over time.

STRUCTURAL CHANGES

IN THE SPEED OF CIRCULATION V

Establishing banks

that create money, the so-called banks of issue like the Bank of England,

structurally altered the financial system by providing a mechanism for the

speed of circulation, V, to change over time.

That mechanism allowed the creation of a

non-productive pool of “unearned”

interest income from deposits.

Unearned income from

deposit interest is a structural part of the debt system. It has nothing at all

to do with production and accumulates solely because new money is created as an

interest-bearing debt. It forms the

basis of the investment sector as distinct from earned savings. The investment

sector is characterised by trading and speculative investment in existing

wealth rather than creating new production and new wealth. Other things being

equal, prices for that existing wealth keep rising because the pool of unearned

income grows as more and more interest is added to it[9].

The banking sector

relies for increased profits on the total money supply M increasing as fast as

possible, thereby allowing the pool of unearned interest to grow quickly.

That’s the main reason the money supply has expanded so quickly. Profit

arising from the bank spread or margin, the difference between the interest

borrowers pay on their loans and the interest banks pay depositors on their

deposits, is a direct function of the money supply M and is, most people would

be surprised to know, largely independent of interest rates. When M goes up bank profits rise. Bank

profits fluctuate with interest rates only when, as a result of perceived

lending risk, they alter their spread, the difference between the interest they

charge on loans and the interest they pay their depositors; or with changes in

the number and size of defaults by borrowers. Such banking activity is part of

the productive sector, but the unearned interest paid by banks on bank deposits

is not.

There is an

inherent conflict of interest between the debt-based banking system and the

productive sector. Capitalism is fundamentally profit-seeking. Banks seek to

increase M to get the greatest profit, while the productive sector receives a

decreasing share of wealth because unearned income shifts money away from the

productive sector to the investment sector. In aggregate, over time, this

drives up asset prices, creating the all too familiar investment bubbles and an

overemphasis on capital gains. Prices

are likely to increase until the point is reached where the expectations of the

investment sector overwhelm the productive economy. This paper will show that

the divergence between capital gains and productive incomes has been increasing

exponentially, guaranteeing future economic collapse unless the financial

system itself is adapted to take account of the mechanics of interest-bearing

debt.

AMENDING THE FISHER EQUATION OF EXCHANGE

The foregoing

discussion suggests the money supply M in the Fisher equation of exchange can

be conceptually divided into two parts.

Money used for production could be called Mp and the unearned income

interest component of M could be called Ms so the Fisher equation can be

written as.

M= Mp+Ms (3)

Mp*Vp = PQ (4)

M = PQ/Vp +Ms (5)

PQ = (M-Ms)*Vp (6)

Mp=M-Ms (7)

Where Mp is the money used for

production,

M is the total money supply,

Ms is the accumulated unearned

income from interest on bank deposits,

Vp is the speed of circulation

of Mp,

P is the price level,

Q is total output of goods and

services.

The unearned income

Ms circulates outside the production cycle so it has no impact on PQ. Hoarding in

times gone by did not structurally increase the money supply M, but the

continual addition of interest on all interest-bearing debt to Ms produces a

structural change in the money supply M and hence, in the original Fisher

equation (Mp+Ms)V=PQ, a structural change in V. That structural change in V has

nothing to do with changes in human hoarding behaviour. It is a mechanical

feature of the interest-bearing debt system.

That may be why so many people have had so much difficulty working with

the Fisher equation of exchange in the past.

In the interest-bearing debt system, all the loans

included in M can never be repaid. The productive money supply Mp from which

they must be repaid is necessarily less than M because M=Mp+Ms. The debt

supporting the unearned income Ms remains forever a burden on the productive

sector.

In equation (4)

Mp*Vp = PQ, if Mp, the productive part of the money supply, is not to actually

shrink, either the total money supply M =(Mp+Ms) must grow by at least the

amount added to Ms, or else the speed of circulation, Vp, of Mp must rise. If

Vp is reasonably constant, as is suspected, then the money supply M must grow

faster than Ms if PQ is to grow.

Since the amount added to M as unearned income from

deposit interest Ms is a percentage of M, the financial system is locked into

exponential growth at least equal to the interest rate on the unearned deposits. The only way to reduce that exponential

growth of M is to reduce or eliminate the interest rate on deposits.

Conceptually, the

effect of unearned interest on deposits is to transfer claims on the real

wealth of the nation from those who produce the economic output PQ to those in

the investment sector who produce nothing.

Houses and other assets become more expensive in terms of the inflated

prices in the investment sector but must be bought using the less inflated

money of the productive sector.

Unless inflation in

the investment sector and the productive sector are equalised, there must be an

ever-widening gap between debt-bound wage and salary earners on the one hand

and the participants in the investment sector with net deposits in the banking

system on the other hand. At the moment

there is a kind of dual exchange rate operating in favour of investors. Wage

and salary earners have to use the less inflated money they earn to buy assets

“priced” in the inflated dollars of the investment sector.

The original Fisher

equation took no account of the investment sector unearned income Ms. Nor did

it take into account offshore borrowings. Countries owing money offshore have

to pay interest on those offshore loans even though the corresponding money

(foreign debt) does not appear in any domestic bank account.

Interest on the accumulated

foreign debt, like interest on the domestic debt, has to be funded from the

productive economy. Unearned interest payments being made on foreign accounts

have to be included in unearned income Ms if it is to truly represent the whole

of the investment pool of unearned income, as well as the interest on domestic

accounts. The domestic money supply is no longer the sole “base” of the “money”

supply as it used to be. Distortions caused by omission of foreign debt would

have been minor for most countries in the early twentieth century when Fisher

first proposed his equation of exchange. They are often more significant today

because some countries like New Zealand have very large current account

(foreign) debts while others like Japan have large current account (foreign)

surpluses.

DEBT

IS MONEY

Until the Bank of

England was established in 1694 virtually all money in circulation was coin.

From 1694 until perhaps the middle of the nineteenth century much of the money

in circulation was made up of bank notes and coins. That changed through the 19th

century. For example, in

By July 2008, 99%

of the

If debt

is money, the variables in equation 7 can be restated:

Debt for production Mp=

(Total

Debt)

With this in mind,

the original Fisher equation can be further reformulated so the speed of

circulation V becomes a function of the productive debt Mp only. This will be

called Vp. The justification for this is that unearned income derived from Ms

produces nothing, though it remains a valuable measure of the concentration of

wealth in the economy.

Since the Total

Debt Md= debt for production Mp + debt supporting unearned income Ms, (equation

3) and Mp=Md-Ms, (equation 7) the newly revised form of the Fisher equation (5)

using just the speed of circulation Vp of the productive debt Mp becomes:

M(d)=PQ(d)/Vp +Ms (8)

Where:

Mp= debt used for production

Vp = speed of circulation of

debt used for production

M(d) = total debt

Ms= debt held by productive

sector to fund unearned income on the total debt,

P = prices

Q(d) = quantity or output of production produced

by Mp

PQ(d) does not include any contribution to a

nation’s GDP resulting from cash transactions.

The three main

components of the total debt Md are the domestic debt, the foreign debt and

central bank reserves. In this work the domestic debt is taken to be the

Domestic Credit while the foreign debt is taken to be Accumulation of all the

Current Account deficits over time. The

reserves, R, held by the central bank, must be subtracted when calculating Md

because they represent debt included in Domestic Credit that is not in

circulation[11]. R is small

compared with

A national current account

deficit really means a country is consuming production created by money

circulating abroad instead of using local money to generate the whole of its

economic product locally. From the point of view of the new Fisher equation

(8), debt circulating in a foreign country is no different from debt

circulating locally. Likewise, the interest being paid on offshore borrowing is

unearned income and its corresponding debt forms part of Ms in the revised

version of the Fisher equation (8) described above. It is conceptually no

different from other unearned income supported by Ms.

When considering

the new Fisher equation in the context of the modern economy the total debt Md

in equation (8) Md=PQ(d)/Vp+Ms has to

include the foreign debt and the debt Ms arising unearned income has to allow

for the interest paid on foreign debt as well as the deposit interest paid on

domestic debt.

The accumulated

national current account debt will be called Dca and the domestic credit

component will be called Ddc. Central bank reserves will be called R. These are

the three main components of total debt

There is one

further variable to be considered. It is the debt, to be called Mv in this

work, directly borrowed to support speculative investment. It belongs with Ms in the investment sector

and is likely to be associated with rapid expansion of debt during an

investment boom.

Mv is, literally, the investment“bubble” that inflates

with booms and decays with busts. The revised Fisher relationship enables it to

be identified and quantified.

Mv appears to have

been especially prominent in the “wild west” days in New Zealand during the mid

1980’s, during the dotcom boom in the late 1990’s and apparently from 2005 to

2009 when there was a substantial new debt bubble. Mv has almost certainly

played a significant role in the

The revised Fisher

equation (8) can be rewritten as:

Md= (Ddc+Dca-R) = PQ(d)/Vp +

(Ms+Mv) (9)

Or, since from equation (7)

Mp= (Md-Ms),

Mp = (Ddc+Dca-R) –(Ms+Mv) (10)

where:

Dca = accumulated current account debt,

Ddc = domestic credit,

R = central bank reserves[12],

Vp = speed of circulation of

debt used for production,

Md = total debt,

Ms = debt held by productive sector to fund the unearned

income on the total debt,

Mv = debt borrowed for speculative investment rather than production

P = prices,

Q(d) = quantity of production produced by debt Mp,

Mp = debt used for production

= (Md-Ms).

The debt that

supplies the investment pool Ms is always “owned” by the productive sector, not

the investment sector. It is a structural part of the total debt Md but its

monetary equivalent in the form of unearned income resides outside of and is

separate from the productive sector. In bad times when there are “losses” in

the investment

sector, the debt Ms remains numerically intact whatever happens in the

productive economy. It is theoretically unrepayable unless debt-free money is

introduced into the financial system or unless there is a negative deposit

interest rate. Actual investment sector losses (write downs) must come either

from the investment sector debt Mv or from the productive sector funding Mp,

reducing the financial system liquidity as was apparent in the

When investors lose

their shirts, their unearned income deposits (their share of deposits arising

from Ms) are merely shifted to someone else. They are still unearned income

deposits. At the end of the day, were

all of the investment sector debt Mv and the productive sector funding Mp to be

eliminated, people in the productive sector would still be left with the debt

Ms. Another, presumably different, group would hold all of the corresponding

unearned income deposits. That is a conceptual endpoint of the present

financial system. Hunger, despair, riots

and even revolution would presumably lead to a change in the financial system

long before such a conceptual endpoint is reached.

AN

ECONOMIC REVOLUTION FROM THE NEW FISHER EQUATION

Take the revised form of the

Fisher equation of exchange:

Md= (Ddc+Dca-R) = PQ(d)/Vp +

(Ms+Mv) (9)

Mp = (Ddc+Dca-R) –(Ms+Mv) (10)

In each production

cycle part of Mp arises from the creation of new debt in the production

phase. In general that new debt is

subsequently cancelled in the consumption phase. There are literally millions

of these cycles continuously superimposed one on the other.

This leads to a

startling conclusion that reflects the beauty of devising a debt model of the

economy. In aggregate, the speed of circulation Vp of the productive debt Mp

must theoretically be 1 when used in the new form (9) of the Fisher equation of

exchange[13]. Each tranche of

new debt Mp is notionally repaid as its product PQ(d) is consumed. Each tranche

of debt is used just once. It is impossible to spend the money arising from a

loan more than once. To spend more means

borrowing more. The shortfall, amounting to the unearned interest income

transferred to Ms in each production cycle, has to be borrowed in addition to

the tranche needed to fund the next production cycle. Much, if not most, of

increased productivity in the productive sector is immediately “lost” to the

investment sector.

The debt Mp in the productive economy must grow if the

economy is to grow. That is the fundamental source of the exponential growth

imperative in all modern debt based economies.

Equations (9)

and (10) are debt based. If Vp in equation (9) is 1, it follows that

the speed of circulation of the monetary equivalent of Mp must also be 1 if

equation (9) is to hold when expressed in monetary terms. That the monetary

“footprint” of Mp can be used only once in generating the nation’s GDP at first

appears to be surprising, remembering that the historical value of the speed of

circulation V in the original Fisher equation in England appears to have been

something like 2.5[14]. Conceptually, each production cycle is

separate. The debt for production is

borrowed and the corresponding money is first used and then repaid as goods and

services are production and consumed.

The money is re-borrowed and repaid again during the next cycle. In aggregate, intermediate productive

transactions are a “pass the parcel” exercise, accumulating and retiring debt

through the production and consumption process.

Table1[15] shows an

indicative model for the

Md= (Ddc+Dca-R) = PQ(d)/Vp +

(Ms+Mv) (9)

It solves the

equation for the speed of circulation in the productive economy, Vp, by

restating equation (9) as:

Vp = PQ(d)/[(Ddc+Dca-R)-(Ms+Mv] (11)

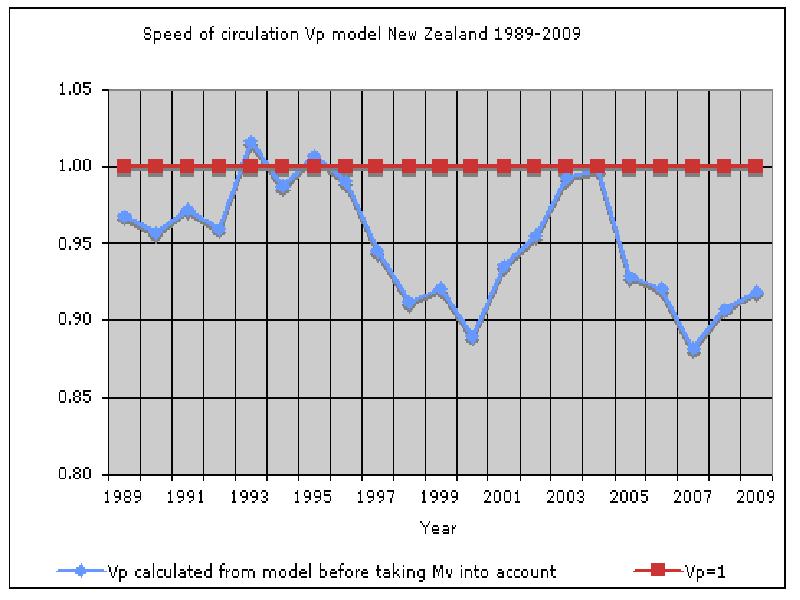

Figure 1 shows the

speed of circulation Vp of the productive debt Mp used to generate the debt

derived portion of

In

Despite the evident

data limitations Table 1 is believed to give a reasonable first approximation

of the application in New Zealand of the revised Fisher equation Vp = PQ(d)/[(Ddc+Dca-R)-(Ms+Mv] (11).

The new version of

the Fisher equation of exchange (9) can be applied at any point in time, in

principle providing macro economic data in real time if the debt and interest

rate numbers are available.

Were interest on

bank deposits to be reduced to zero, the pool of unearned income Ms would

remain constant at its present level.

With the speed of circulation Vp=1, the increase in GDP would become a

direct function of the Total Debt Md-Mv.

The effect of

applying the modified Fisher equation (11) Vp =

PQ(d)/[(Ddc+Dca-R)-(Ms+Mv)] in

the modern economy can be stated as follows:

In a cash-free debt

based economy with zero interest rates on deposits the increase in GDP (PQ)

equals the increase in the total debt Md less any change in direct speculative

investment Mv.

In

the debt system, economics is primarily a matter of debt management.

TABLE 1 MODIFIED FISHER

APPLICATION NEW ZEALAND 1978-2008

USING AGGREGATE FIGURES

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

13 |

|

Year |

CA* |

DC* |

I%* |

GDP* |

Mo |

Vo |

PQd* |

Md* |

%Md* |

Ms |

Vp’ |

Mv* |

|

1978 |

4.8 |

9(Est) |

8.7 |

15.3+ |

0.404 |

19 |

7.6 |

13.6 |

36 |

4.75 |

0.86 |

1.21 |

|

1979 |

5.3 |

9.8 |

7.0 |

17.4+ |

0.455 |

19 |

8.8 |

14.9 |

36 |

5.11 |

0.90 |

1.01 |

|

1980 |

6.1 |

11.2 |

8.0 |

20.3+ |

0.491 |

19 |

11.0 |

17.1 |

36 |

5.57 |

0.95 |

0.52 |

|

1981 |

7.0 |

12.9 |

9.0 |

23.6+ |

0.535 |

19 |

13.4 |

19.6 |

36 |

6.16 |

1.00 |

0.08 |

|

1982 |

8.6 |

15.9 |

9.0 |

28.7+ |

0.593 |

19 |

17.4 |

24.2 |

36 |

6.87 |

1.00 |

-0.07 |

|

1983 |

10.5 |

21.8 |

8.8 |

32.3+ |

0.650 |

19 |

20.0 |

32.0 |

36 |

7.77 |

0.82 |

4.31 |

|

1984 |

12.4 |

25.4 |

10.1 |

36.0+ |

0.652 |

19 |

23.6 |

37.5 |

36 |

9.03 |

0.83 |

4.88 |

|

1985 |

15.7 |

30.4 |

10.5 |

40.7+ |

0.718 |

18 |

27.8 |

45.8 |

36 |

10.60 |

0.79 |

7.43 |

|

1986 |

19.7 |

40.0 |

14.3 |

46.9+ |

0.831 |

17 |

32.8 |

59.4 |

36 |

13.31 |

0.71 |

13.31 |

|

1987 |

22.5 |

44.6 |

14.2 |

55.3+ |

0.868 |

17 |

40.5 |

66.8 |

36 |

16.54 |

0.81 |

9.71 |

|

1988 |

24.9 |

51.8 |

12.3 |

63.2+ |

0.861 |

17 |

48.6 |

76.4 |

42 |

20.24 |

0.86 |

7.58 |

|

1989 |

25.5 |

53.2 |

11.5 |

67.9+ |

0.953 |

17 |

51.7 |

78.3 |

53 |

24.95 |

0.97 |

1.70 |

|

1990 |

28.3 |

58.3 |

10.8 |

71.5+ |

1.075 |

17 |

53.2 |

86.2 |

64 |

30.84 |

0.96 |

2.38 |

|

1991 |

30.2 |

63.1 |

10.8 |

73.3+ |

1.120 |

17 |

54.3 |

92.9 |

67 |

37.12 |

0.97 |

1.55 |

|

1992 |

32.1 |

68.9 |

8.4 |

72.9+ |

1.024 |

17 |

55.5 |

100.6 |

70 |

42.81 |

0.96 |

2.32 |

|

1993 |

34.0 |

70.9 |

6.3 |

76.1+ |

1.082 |

16.8 |

58.0 |

104.5 |

72 |

47.46 |

1.02 |

-1.21 |

|

1994 |

35.9 |

77.9 |

5.4 |

80.9+ |

1.219 |

16.5 |

60.8 |

113.4 |

74 |

51.82 |

0.99 |

0.8 |

|

1995 |

40.0 |

82.5 |

5.8 |

86.3+ |

1.301 |

16

|

65.5 |

122.0 |

76 |

57.01 |

1.01 |

-1.14 |

|

1996 |

45.1 |

91.9 |

7.2 |

93.2 |

1.399 |

15.5 |

71.5 |

136.5 |

78 |

64.27 |

0.99 |

0.83 |

|

1997 |

51.0 |

102.0 |

7.3 |

98.0 |

1.503 |

15 |

75.5 |

152.5 |

80 |

72.70 |

0.95 |

5.04 |

|

1998 |

56.5 |

112.2 |

6.5 |

101.7 |

1.547 |

14.5 |

79.3 |

168.2 |

82 |

81.25 |

0.91 |

7.71 |

|

1999 |

60.9 |

122.5 |

6.4 |

103.4 |

1.682 |

11 |

84.9 |

182.9 |

84 |

90.69 |

0.92 |

8.51 |

|

2000 |

68.0 |

134.6 |

4.4 |

109.1 |

1.830 |

9 |

92.6 |

202.1 |

86 |

97.97 |

0.89 |

11.37 |

|

2001 |

73.2 |

143.9 |

5.4 |

116.0 |

2.044 |

7 |

101.7 |

216.5 |

88 |

107.9 |

0.94 |

6.86 |

|

2002 |

76.6 |

159.6 |

4.7 |

124.1 |

2.237 |

5 |

112.9 |

235.7 |

90 |

117.5 |

0.96 |

5.17 |

|

2003 |

81.6 |

170.6 |

4.6 |

131.0 |

2.289 |

3.5 |

123.0 |

251.6 |

92 |

127.8 |

0.99 |

0.76 |

|

2004 |

87.9 |

184.5 |

4.4 |

139.8 |

2.483 |

2.75 |

133.0 |

271.8 |

94 |

138.6 |

1.00 |

0.13 |

|

2005 |

98.2 |

209.9 |

4.8 |

149.1 |

2.686 |

2 |

143.7 |

306.5 |

95 |

151.8 |

0.93 |

10.84 |

|

2006 |

112.7 |

223.8 |

5.7 |

156.6 |

2.811 |

1.5 |

152.4 |

334.7 |

96 |

169.3 |

0.92 |

12.86 |

|

2007 |

126.4 |

249.7 |

6.2 |

165.1 |

2.945 |

1.0 |

162.2 |

374.5 |

97 |

190.6 |

0.88 |

21.34 |

|

2008 |

140.2 |

273.3 |

7.0 |

177.6 |

3.038 |

0.5 |

176.1 |

411.6 |

98 |

217.6 |

0.91 |

17.80 |

|

2009 |

155 |

292.9 |

6.49 |

183 |

3.44 |

0 |

183.0 |

444.1 |

99 |

245.9 |

0.92 |

15.93 |

CA = accumulated current

account deficit NZ$b; DC=Domestic Credit

NZ$b; I%= annual average deposit interest rate;

GDP = Official SNA GDP NZ$b; PQd=Column 5- Column 6 x column 7

NZ$b; Md=Column2 +Column3-RBNZ “capital

reserves” NZ$b, %Md = estimated

proportion of Md funded at deposit interest rate; Ms =Column 9 *x Column 10 x Column 4 accumulated NZ$b; Vp’=(Column 9-Column

11)/Column 8NZ$b; Mv =Column 9- Column 5-Column 11 NZ$b + GDP figures based on SNA 68.

Were Ms and Mv zero in the

revised Fisher equation (11), it would

essentially be returned to the form of the original Fisher equation (1) MV=PQ except that the debt-derived equivalent

of M in the original equation is now expressed as (Ddc+Dca-R).

At the time Fisher first

proposed the Fisher equation of exchange in 1911, most economic transactions

were still cash transactions[19].

That is not to suggest

for a moment there is no role for economic and monetary policy. The allocation

of available human and natural resources and distribution of wealth are

immensely important issues in modern societies.

But there is no alchemy of economics and never was, any more than was

the case in late medieval

Figure 1 shows Vp

plotted for New Zealand 1989-2009 from Table 1 before taking into account the

speculative investment Mv. Mv is the

debt needed to bring Vp back to 1.

Figure 2 shows the

Mv bubbles as a percentage of GDP that result when Vp is 1. Figure 2 suggests the dotcom bubble at the

turn of the century and the property bubble 2005-2009 were both smaller than

Mv bubbles

dissipate through the repayment (or

write-off) of the speculative debt. Speculative investors sell off assets to

the holders of Ms unearned income deposits or those with earned savings forming

part of

BANKS

AND BANKING

Generally speaking, the larger

the Total

FIGURE 1: SPEED OF CIRCULATION Vp’ OF PRODUCTIVE DEBT

NEW ZEALAND 1989-2009 FROM TABLE 1*

(CLICK HERE FOR FIGURE 1 : THE SPEED OF

CIRCULATION Vp OF PRODUCTIVE DEBT IN NEW ZEALAND 1989-2009 )

{kind=link}

Vp’ greater than 1.0 arises

from data and modelling error

FIGURE 2 BUSINESS CYCLE BUBBLES AS PERCENTAGE OF GDP

(CLICK HERE FOR FIGURE 2 : BUSINESS

CYCLE BUBBLES AS PERCENTAGE OF GDP)

{kind=link}

* Named after finance minister Douglas. Mv was

substantial through this period of wild speculative expansion though it appears

to have begun earlier. Mv below 0 arises

from data and modelling error income Ms,

the only way to fully repay that new debt is by creating yet more new debt on

which yet more interest has to be paid.

This ongoing process produces the exponential increase in total debt Md,

(and therefore Ms), in the present financial system. Exponential trendlines can be overlaid on the

historical curves for total debt Md, the investment sector Ms and the

accumulated current account deficit Dca (1986-2009) from Table 1[22].

Not only are those

debt trend curves exponential, they show clearly that the investment sector in

New Zealand has been growing exponentially at about 11.2%, substantially faster

than the total debt and current account which have each been growing at about

8.6% and 8.9% respectively. The rapid growth of Ms has very serious monetary

policy implications because it means the productive debt Mp is shrinking as a

proportion of total debt

Monetary policy in

the Western world has evidently and, one would like to hope, inadvertently,

supported this stranglehold by banks over the economy. The only mechanism

presently in use to manage the growth of total debt Md is the interest rate

that in most countries is indirectly controlled by central banks like the US

Federal Reserve. Many of those central banks are themselves powerfully

influenced by the private sector.

Increasing interest

rates to manage inflation has two immediate effects. First, it further

increases the flow of money from the productive sector to the investment sector

by increasing the unearned income pool Ms. Secondly it will tend to increase

bank profits wherever, in response to higher perceived lending risks, the banks

increase their spread or gross interest margin on their loans[23]. Raising the price

of productive debt Mp squeezes demand for it. Jobs are lost. Ordinary people

have less money to spend because more of their income is used to service (pay

interest on) their existing debt. Home ownership becomes difficult if not

impossible. This shift can be called the “transfer effect”.

The transfer effect

is the main reason the use of interest rates to manage the economy has now

failed around the world. In

The revised Fisher equation of exchange proves

conclusively that the use of interest rates for economic management works, if

it works at all, only at extraordinary human cost. The revised Fisher equations

developed in this paper provide a compelling theoretical basis for changing the

world’s financial architecture.

LIQUIDITY

AND CIRCULATING DEBT

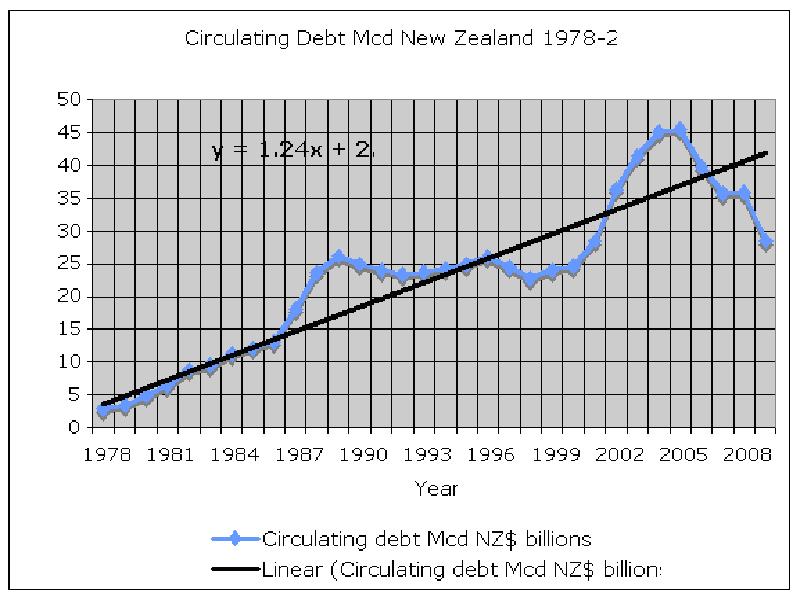

The productive debt

Mp is made up of a foreign component Dca, the accumulated current account

deficit, and a domestic component Mcd which is equal to the domestic credit Ddc

less the investment sector debt Ms less the central bank reserves R. Mcd can be

called the “circulating debt”.

Md=Mp+(Ms+Mv) =

(Dca+ Mcd) + (Ms+Mv) = Dca+Ddc -R (12)

Other indicators

can be readily developed using these simple relationships. For example, the “circulating debt” Mcd can be defined as

Mcd= (Mp-Dca) = Ddc-(Ms+Mv)-R (13)

where:

Dca is the

accumulated national current account deficit,

Ddc is the domestic

credit,

Mcd represents the debt

actually available to be used in producing the domestic part of the gross

domestic product produced by debt (PQ(d)),

Mp, Ms, Md. Mv and

R are as previously defined.

The portion of the

gross domestic product produced by domestic debt can be called PQ(dom). It can be defined as:

PQ(dom) =

PQ(d)-PQ(ca) (14)

Where:

PQ (dom) is the

domestic part of QP(d),

PQ(ca) is the

contribution to PQ(d) resulting from the current account,

PQ(d) is as

previously defined.

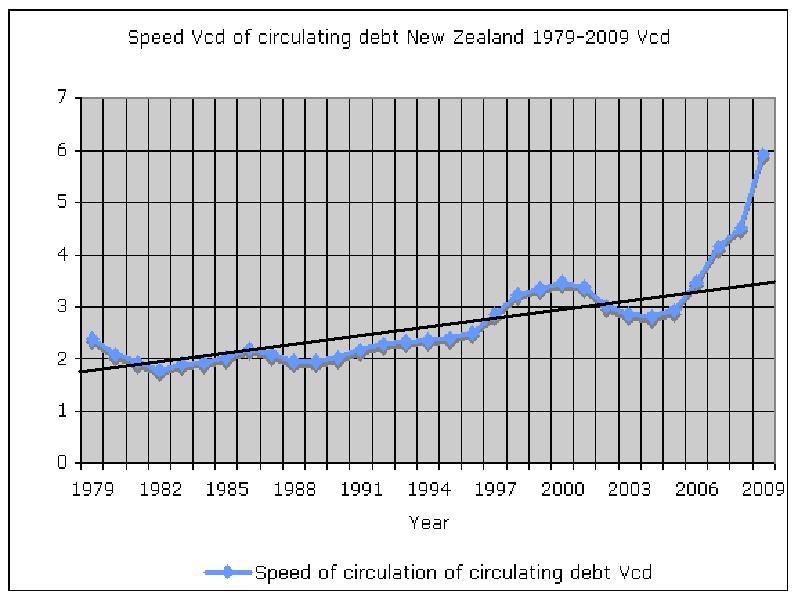

The speed of

circulation Vcd of the “circulating debt” Mcd

can be defined as :

Vcd =

PQ(dom)/Mcd =

PQ(dom)/(Ddc-(Ms+Mv)-R) (15)

Mcd is the debt

actually available to produce the domestic component PQ(dom) of output PQ(d)

because the foreign debt Dca is committed offshore and is not available for

domestic production. In one sense it is the closest modern equivalent to the

money supply M in the original Fisher equation of exchange MV=PQ (1) and is

believed to be a very sensitive indicator of economic activity. In a world of

instantaneous transaction settlement, most of Mcd represents earned savings

plus transaction account balances.

The speed of

circulation Vcd is believed to be comparable to the speed of circulation V of the

money supply M in the original Fisher equation (1) though it is more virtual

than real. In the interest-bearing debt system the speed of circulation, Vp, of

Mp is 1. Because Dca is unavailable to

the domestic economy except as debt in bank accounts the residual part of Mp,

Mcd, appears to “work harder”. Most of

the earned savings that make up Mp belong to overseas savers when in a healthy

economy those savings would be held in

Figures 3 and 4

show Mcd and Vcd for New Zealand, 1979-2009.

They show that the

speed of circulation Vcd increased steadily in

FIGURE 3:

(CLICK HERE FOR FIGURE 3 : CIRCULATING DEBT Mcd IN NEW ZEALAND 1979-2009

)

{kind=link}

FIGURE 4: SPEED OF CIRCULATION Vcd OF CIRCULATING DEBT

Mcd NEW ZEALAND 1979-2009[25]

{kind=link}

Because of

substantial fluctuation of the circulating debt for production Mcd during

modern business cycles, Vcd is thought to be much less stable now than in past

centuries.

The circulating

debt for production Mcd is thought to be an excellent (inverse) numerical

measure of the liquidity of the financial system.

Figures 3 and 4

show the three boom and bust cycles (mid 1980’s equities, late 1990’s dotcom,

2005-2008 property)

THE

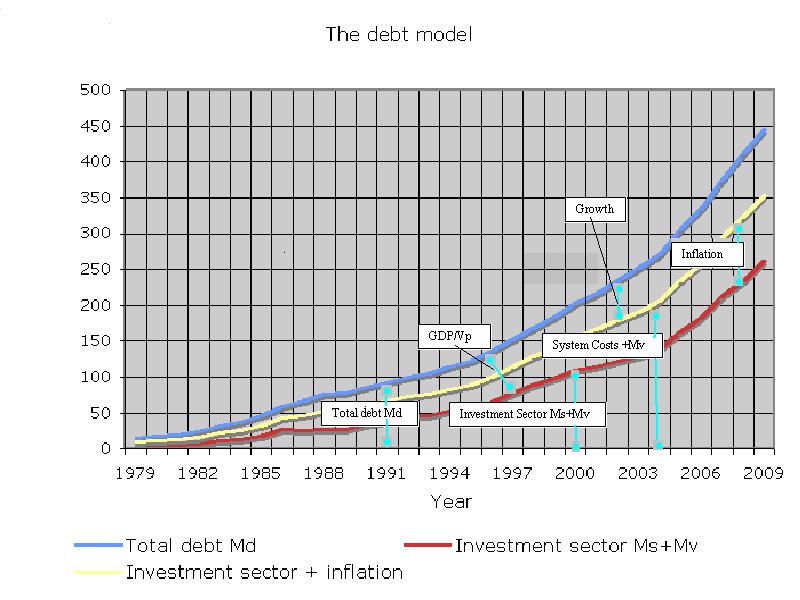

DEBT MODEL

The revised Fisher equation of

exchange Md= (Ddc+Dca-R) = PQ(d)/Vp + (Ms+Mv)

(9)

offers a very simple debt

model of the economy.

It is shown in

Figure 5 where the total debt Md, and unearned income Ms plus speculative

investment Mv, are plotted against time.

PQ(d)/Vp (=Nominal GDP) is the difference between the two curves.

The dependence of

gross domestic product (GDP) on the total

debt Md and the interest rate on bank deposits in the modern cash-free economy

has truly profound implications. The speed of circulation in the productive

sector Vp is fixed at 1. Increases in unearned income arising from Ms depend

directly on the deposit interest rate.

In the light of the

worldwide financial chaos of 2007-2009 the first order debt model shown in

Figure 5 provides a powerful argument in support of public control of a

nation’s financial system. The present

system leaves the world economy at the mercy of privately owned institutions

working for private profit by allowing irresponsible increases of the total

debt, Md and its associated bubble formation.

It isn’t possible

to have a simpler model of the economy than:

Total

debt Md=Nominal GDP (Mp)+Unearned Income Ms + speculative investment Mv.

That is especially

so when, with a simple reconfiguration of the financial architecture, Mv can be eliminated and Ms held constant. That would make the economy

directly dependent on

Total debt, Md, in

New Zealand has grown exponentially by an average of about 8.6% per year since

1986 while the unearned income investment sector as been expanding at the rate

of 11.2% per year. Unless checked, the

only possible outcome for the system over time is for the system liquidity

(Figure 3) to be squeezed toward zero, producing fundamental economic collapse[27].

It is therefore imperative that liquidity be injected

into the system urgently by increasing the domestic credit and largely

eliminating the growth of the investment sector Ms. The model can be used to

quantify the liquidity needed to utilise each nation’s maximum growth capacity.

FIGURE 5: THE DEBT MODEL FOR

THE

(CLICK HERE FOR FIGURE 5 : THE DEBT

MODEL FOR THE NEW ZEALAND ECONOMY )

{kind=link}

DEPRESSIONS,

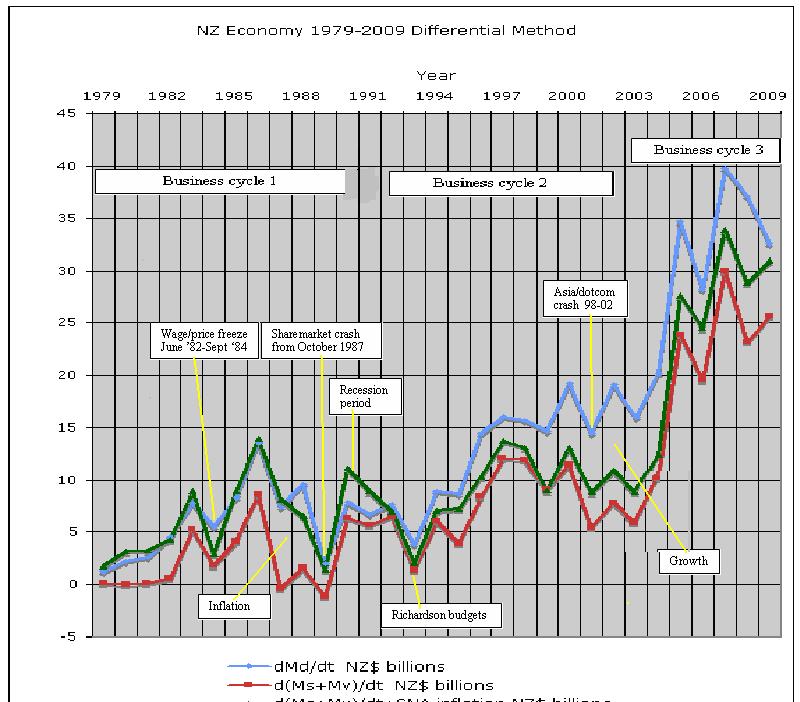

RECESSIONS AND DIFFERENTIAL ANALYSIS

The revised Fisher

equation (9)

Md= (Ddc+Dca-R) =

PQ(d)/Vp + (Ms+Mv)

shows the

relationships among the total debt Md, the total productive output PQ(d), the

speed of circulation of the productive debt Vp, the debt arising from accumulated

unearned income Ms and speculative investment Mv over time. Following basic

differential methods the equation can also be written:

dMd/dt = d/dt (Ddc+Dca-R) = d/dt[PQ(d)/Vp +

(Ms+Mv)] (16)

where over any

small period of time dt, the change in the total debt Md = the change over the

same time dt of PQ(d)/Vp +(Ms+Mv).

There is quite a

lot more variability in the figures calculated this way compared with Table 1

because additional error is introduced by multiple subtractions of large numbers.

Using the

differential approach allows the new debt model to show how the economy is

performing in practice. With better data economic performance could be assessed

monthly, or even, theoretically, in real time.

The differential approach using annual data from Table 1 is shown in

Figure 6. The recorded consumer price

index (CPI) inflation has been added to demonstrate business cycle booms and

busts. Figure 6 is indicative only

pending better model data and calibration.

Of particular

interest in differential equations is what happens at maxima and minima, that

is, at high points and low points.

Referring again to equation (16),

When dMd/dt = 0, d[PQ(d)/Vp+

(Ms+Mv)]/dt = 0, so d/dt PQ(d)/Vp = -d (Ms+Mv)/dt

If there is no

increase in the total debt, nominal economic output PQ(d)/Vp must contract by the amount of unearned income that has to

be transferred to the investment sector and any increase in speculative

investment Mv. For nominal economic output to increase at all, Md must increase

by at least the amount transferred to Ms and invested in Mv. This provides, for the first time, an

absolute definition of a depression, namely when dMd/dt

is less than d(Ms+Mv)/dt.

A depression occurs when the change in the total debt

over time is less than what is needed to service the unearned interest that has

to be paid to the investment sector Ms plus any increase in speculative

investment Mv, that is, when there is no provision for either inflation or

growth.

A similar, absolute,

definition of a recession is when dMd/dt is less than d(Ms+Mv)/dt plus

provision for inflation. Provision for

inflation and unearned income can together be considered financial system

costs. Economic growth occurs only when and to the extent that dMd/dt exceeds

the financial system costs plus speculative investment Mv.

A recession occurs when the change in total debt over

time is less than what is needed to service the financial system costs, being

the unearned interest that has to be paid to the investment sector Ms plus

inflation, plus speculative investment Mv.

The difference

between a recession and a depression is that a recession provides for inflation

but not growth, while a depression provides for neither growth nor inflation.

The model can be

used to provide specific measurable monetary targets to avoid recessions and

depressions. The targets can easily be identified in advance and new debt

injected into the system to maintain growth.

FIGURE 6: INDICATIVE REVISED FISHER DIFFERENTIAL EQUATION

(16) FOR THE

(CLICK HERE FOR FIGURE 6 : NZ

ECONOMY 1979-2009 DIFFERENTIAL METHOD )

{kind=link}

*Preliminary data only; March

years: to show how the model works in

practice.

The chart applies only to

PQ(d) the GDP produced by debt (see equation 16): it does not include GDP

created through the use of cash. The banking sector seized up in 1989 and 1993

much as it did in 2008-2009.

As long as private

interest-bearing debt continues to fund economic activity, it is fundamental

that the total debt dMd/dt continue to expand, no matter what else is happening

in the economy. In the midst of a major

economic downturn in

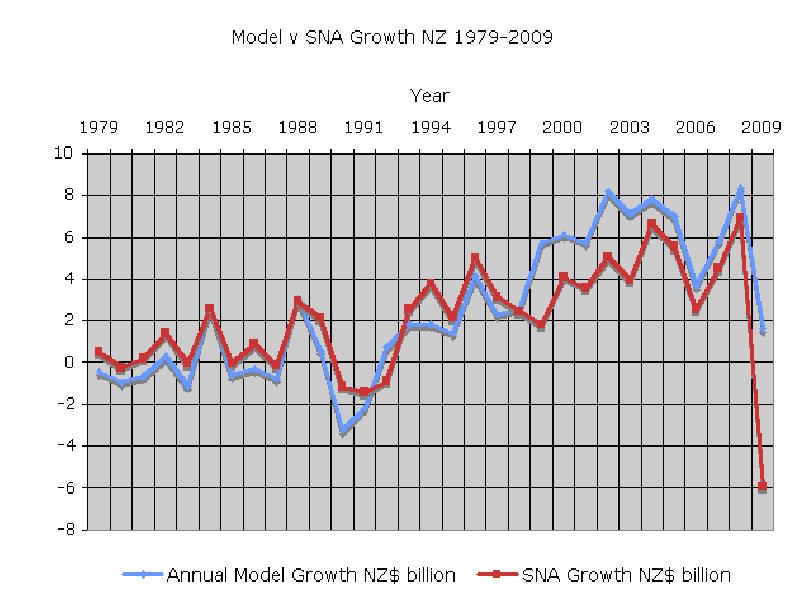

Figure 7 shows the

model growth from Figure 6 plotted against the measured SNA growth from

1979-2009. While Figure 7, like Figure

6, is only preliminary, the model pattern follows the SNA growth trend very

well except for 1999[28]. The model growth figures tend, on the whole,

to be lower than the SNA growth figures because they arise from the use of debt

only. They do not include growth arising from cash transactions during the

period prior to the rapid expansion of EFTPOS beginning in the March 1999

year.

FIGURE 7: MODEL GROWTH COMPARED WITH SNA GROWTH IN THE

(CLICK HERE FOR FIGURE 7 : MODEL v. SNA

GROWTH NZ 1979-2009.)

{kind=link}

THE

GENERAL RESTATEMENT OF THE FISHER EQUATION OF EXCHANGE

A general economic model

aligned to the original Fisher equation of exchange is

PQ = (

Where PQ is the GDP,

Md,Ms,Vp,Mv are as described elsewhere

in this paper, (for example equation (9)):

Md is the total debt,

Ms is the debt representing

unearned income on deposits,

Mv is the debt borrowed for

speculative investment rather than production

Vp is the speed of circulation

of Mp (

Mo is the circulating currency

contributing to output,

Vo is the speed of circulation

of Mo,

Eo is circulating electronic

debt-free currency,

Veo is the speed of

circulation of Eo (and must be equal to Vcd).

This general

revision of the original Fisher equation of exchange allows the model to apply

to countries that are not yet cash-free, and countries where debt-free

electronic cash or E-Notes are introduced to replace bank debt.

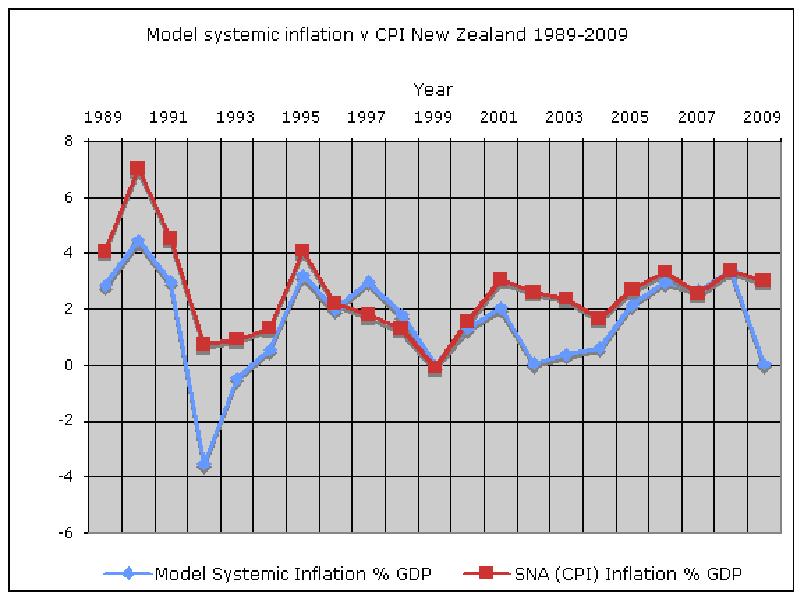

INFLATION

The debt model

proposed in this paper offers radical new insights into the nature and causes

of inflation.

The revised

differential form of the Fisher relationship:

dMd/dt = d/dt (Ddc+Dca-R) = d/dt[PQ(d)/Vp +

(Ms+Mv)] (16)

includes dMs/dt, the

structural increase of unearned income in the debt system. Conceptually dMs/dt is borrowed into

existence through each production cycle and is passed by way of interest on the

total debt Md through the economy to deposit holders. Ms is unproductive and

represents a structural cost of the debt system. As long as dMs/dt remains the same over time

the same amount of new deposit interest is being passed through the productive

system each cycle. At any point in time, the amount dMs/dt is already included

in the price structure PQ. However, should dMs/dt change over time the amount

included in the price structure PQ must also change. The change over time of

dMs/dt is called the second derivative of Ms. The second derivative of Ms[30] represents systemic inflation in the productive

sector resulting from the debt system because it must be reflected in prices

unless producers accept ever lower margins.

Systemic inflation is inherent in any rise in total debt Md unless the

impact of falling interest rates offsets the impact of rising debt.

Inflation in the

debt system can be divided into three components:

(a) The structural systemic inflation d2Ms/dt, the second derivative of Ms,

representing the changes in dMs/dt over time, and

(b) “PQ”

inflation representing the price-quantity “swap”, effectively the demand curve

of basic economics. PQ inflation happens

when prices rise and the quantity consumed decreases more or less

proportionately. Typical recent examples in

(c) Non-systemic price changes to increase or

maintain margins or profit, such as, for example, to offset wage and salary

increases, tax adjustments and other compliance costs.

PQ inflation does

not change the nominal GDP although it does change the relationship between

inflation and growth within the nominal GDP.

Non-systemic price changes are, like systemic inflation, inflationary.

Aggregate price changes have their counterpart on the income side in increased wages

and salaries, establishing a feedback loop as production costs then continue to

increase[31].

Since Ms, dMs/dt

and d2Ms/dt2 are readily available from Table

The plotted

systemic inflation d2Ms/dt2 figures should always be less

than the CPI figures because they do not include:

(i) “PQ” inflation

(ii) The inflation contribution from increases in

the amount of cash in circulation and used to generate nominal GDP.

(iii) Other non-systemic price changes to

increase or maintain margins or profits.

The contribution

from (ii) is weighted towards the earlier end of the graph in Figure 8 because

Ms was much smaller then and more cash was being used. In

The introduction of

the concept of systemic inflation

leads to a truly radical conclusion;

Raising interest

rates in a cash-free interest-bearing debt-based economy increases systemic CPI

inflation instead of reducing it.

The effect of increasing

interest rates is to starve the productive economy of productive debt as more

of the total debt Md is shifted to Ms, while, at the same time, the demand for

new debt is constrained by the higher interest rates. Under orthodox economic management, systemic

inflation falls after interest rates

begin to fall, that is, after the productive economy has already been slowed or

forced into recession by high interest rates[33]. The rising systemic inflation is

masked, as interest rates are increased, by discounting inventory and by lower

business profitability. To reduce CPI inflation figures when interest rates are

rising, non-systemic inflation must fall faster than systemic inflation rises,

driving the economy into recession.

Since wage and

salary increases often occur in response to price increases they have to be

substantially absorbed by productivity gains or reduced business margins

whenever systemic inflation is similar to measured CPI inflation, as has been

the case during much of the period shown on Figure 8. This raises the possibility that aggregate

productivity gains in the economy could be larger than is generally

acknowledged.

GROWTH AND TRADE

In the revised

Fisher equation (16):

dMd/dt = d/dt (Ddc+Dca-R) = d/dt[PQ(d)/Vp +

(Ms+Mv)]

for the change in

FIGURE 8: MODEL SYSTEMIC INFLATION V CPI INFLATION

NEW ZEALAND 1989-2009

(CLICK HERE FOR FIGURE 8 : MODEL

SYSTEMIC INFLATION v. CPI NEW ZEALAND 1989-2009 )

{kind=link}

GDP growth in

In terms of the revised Fisher

equations (10) and Figure 5, economic growth in a cash-free debt-based economy

is defined as:

Growth

= Total debt Md – Unearned income Ms- Speculative Investment Mv - Inflation

More importantly,

since from equation (13),

Mcd= (Mp-Dca) = Ddc-(Ms+Mv)-R

Mcd would be up to

NZ$100 billion dollars higher than it is.

The accumulated

current account deficit Dca is the underlying source of

Had Dca not

accumulated the way it has, there would be no savings problem in New Zealand

even if some of the extra NZ$ 100 billion had been used to retire domestic debt[36]. Any such debt retirement would have meant the

total debt Md and the circulating debt Mcd would each have been reduced by the

same amount. While this would have reduced the GDP[37], new domestic lending would probably

have offset any domestic debt retirement.

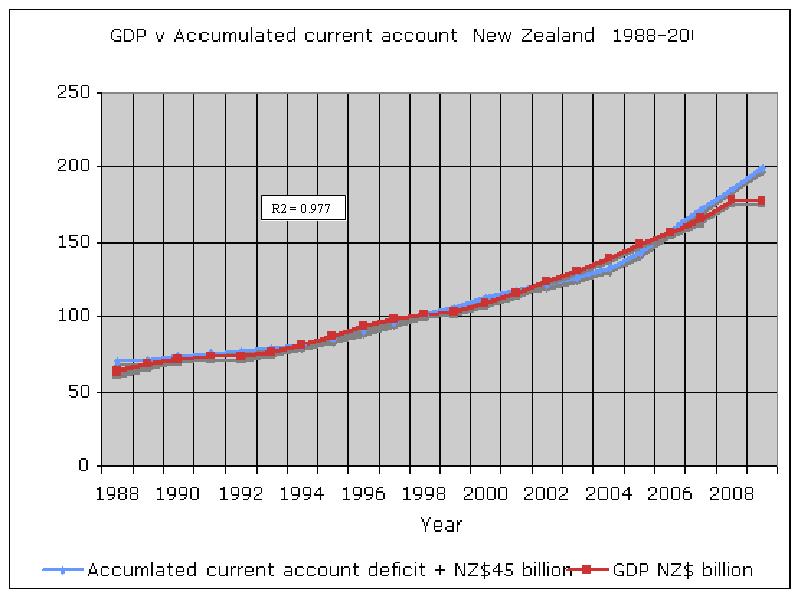

FIGURE 9: INCREASE IN GDP v INCREASE IN ACCUMULATED

CURRENT ACCOUNT NEW ZEALAND 1988-2009

(CLICK HERE FOR FIGURE 9 : GDP v.

ACCUMULATED CURRENT ACCOUNT NEW ZEALAND 1988-2009)

{kind=link}

Greater savings Mcd

would have been likely to have stimulated more productive investment, expanding

the productive economy. The country’s “wealth” would be NZ$100 billion greater

than it is because the deposits corresponding to the additional debt Ddc would

be held in

The debt model

described in this paper discloses the importance of the current account being

balanced. In practice, the revised Fisher equations show

On the face of it,

Applying the

revised Fisher equation (16) to

dMd/dt = d/dt (Ddc+Dca-R) = d/dt[PQ(d)/Vp +

(Ms+Mv)]

there have been no

bubbles since 1990, so dMv/dt is effectively zero. Deposit rates have also been

practically zero so dMs/dt is also close to zero. R is very small compared with Ddc and Dca and

Vp is 1, leaving, as a first approximation:

dPQ(d)/dt [

Table 2 gives the

key current account data for

TABLE 2: CURRENT ACCOUNT DEFICIT JAPAN 2004-2008

|

|

2004 |

2005 |

2006 |

2007 |

2008 |

Total |

|

Current account deficit |

-172 |

-166 |

-170 |

-213 |

-193 |

-914 |

|

Nominal GDP change % |

2.7 |

1.9 |

2.4 |

2.1 |

1.4 |

|

|

CPI% |

0 |

-0.3 |

0.3 |

0 |

0.6 |

|

|

Growth% |

2.7 |

2.2 |

2.1 |

2.1 |

0.8 |

|

|

Nominal GDP change US$b |

114 |

100 |

96 |

92 |

35 |

437 |

The Japanese US$

current account surpluses could theoretically have been sold for Yen. Doing so

would have substantially increased the Yen/US$ exchange rate making Japanese products

more expensive. The Japanese decision not to allow the orthodox exchange rate

mechanism to work to “self correct” the current account deficit was a public

policy decision[41].

The revised Fisher

equations presented in this paper demonstrate how inappropriate the present

world financial architecture is. Current account imbalances and their

associated capital flows cause economic dislocation in the case of surplus as

well as deficit. The message from this

work is that free trade could be fine as long as current accounts remain

balanced. Existing large imbalances are causing major disruption throughout the

world economy. The unilateral use of a mechanism like the foreign exchange

surcharge referred to above could be seen as an interim measure pending the

introduction of a mutually agreed international mechanism to maintain neutral

current account balances[42].

SAVINGS

In the revised

Fisher equations (9) and (16) traditional “savings” stand outside the

accumulated unearned income Ms and speculative investment Mv. They represent

earned income that is not spent and are included in the “circulating debt” for

domestic production Mcd shown in Figure 3[43]. They form part of Mp, the debt used

for production, rather like the money supply M of hundreds of years ago referred

to in the original Fisher equation (1) MV=PQ.

While traditional

savings from earned income form part of the debt for production Mp, they are

still deposits in the banking system like all other deposits. The unearned income

on them is also derived from debt and therefore forms part of the investment

sector Ms.

Superficially, the

speed of circulation Vcd of the circulating debt Mcd, assuming Mcd is

equivalent to M in the original Fisher equation MV=PQ (1), is still of the same

order as V is thought to have been about 700 years ago. It seems at first

glance, that human hoarding behaviour may not have changed substantially over

time. That is not necessarily so because

the mechanics of the debt system have produced immense changes in banking and

accounting through the centuries. In the

modern debt system in

The level of earned

savings Mcd is defined primarily by the debt system mechanics rather than by

individual savers.

That’s why, from

equation (13), Mcd= (Mp-Dca) =

Ddc-(Ms+Mv)-R, the savings level in

Encouraging wage

and salary earners to “save” means increasing the circulating debt Mcd[44]. The speed of circulation Vcd of Mcd is an

excellent measure of domestic saving

or hoarding[45]. The lower the

speed of circulation Vcd the more domestic saving there is.

The decline in

domestic household saving has long been a concern in countries like

There should be

widespread concern that domestic

hoarded savings can no longer be used for productive investment as much as they

used to be[47]. In the present

debt system, debt typically borrowed for productive investment migrates to

savings accounts once spent. Apparently, new debt precedes more savings in the

production cycle. More hoarding requires

either higher net incomes or a lower standard of living, both of which have

considerable policy implications; but in New Zealand, above all, it depends on

managing the country’s accumulated current account deficit so domestic savings

can be increased as a proportion of GDP.

In economic downturns many households prefer to reduce

debt rather than hold savings deposits. Holding debt costs more than is

“earned”, after tax, from the interest on deposits. Such debt retirement (repayment)

reduces the total debt Md as well as the debt for production Mp and the

circulating debt Mcd. That means it also decreases the nation’s gross domestic

product, GDP. In the absence of tax or other incentives to encourage

traditional savings there is an inherent conflict between the national interest

of increased productive output, GDP, and the interests of households still

holding debt. Avoiding increases in the

debt supporting the unearned income Ms by removing interest on deposits would

help restore economic growth but it would also tend to further reduce the

incentive to save. Just about everyone would choose to repay his debt unless

the interest rates on bank loans are held below 2-3%. This would produce

tension between traditional savings and the payment of interest on deposits as

well as between savings and debt. Perhaps the only way to resolve the tension

between savings on the one hand and debt repayment and interest rates on the

other hand may be to restrain or remove the interest-bearing debt system

itself. This is a powerful argument in support of reserving to the government

and people of

Since some sectors

in the community presently rely quite heavily on unearned income, government

issue of new debt at very low or zero deposit interest could be accompanied by

compensatory tax changes, such as making a first tranche of income free from

income tax.

CONCLUDING REMARKS

1. Debt modelling can be used to provide

insights into the mechanics of the traditional interest-bearing debt-based

financial system.

2. The economy can be represented by a debt

model derived from the Fisher equation of exchange (Mv=PQ) .

3. The general form of the debt model is:

PQ = (

Where PQ is the GDP, Md is the total debt, Ms is the debt representing

unearned income on deposits, Mv is the debt borrowed for speculative investment

rather than production, Vp is the speed of

circulation of Mp (Md-Ms), Mo is the

circulating currency contributing to output, Vo is the speed of circulation of

Mo, Eo is circulating electronic

debt-free currency, Veo is the speed of circulation of Eo (and must be equal to

Vcd).

This general

revision of the original Fisher equation of exchange allows the model to apply

to countries that are not yet cash-free, and countries where debt-free

electronic cash or E-Notes are introduced to replace bank debt.

4. A recession occurs when the change in total

debt over time is less than what is needed to service the financial system

costs, being the unearned interest that has to be paid to the investment sector

Ms plus inflation, plus speculative investment Mv. In a recession the growth of

5.

When interest rates fall, the rate of increase of the

total debt Md tends to rise because borrowing becomes more affordable. In that

case, in the revised Fisher equation, both the productive sector debt Mp and

the growth of nominal GDP, (PQ) are likely to rise.

6.

The speed of circulation Vp of the productive debt Mp

in the revised Fisher equation is 1.

7.

Once the bubble variable Mv is eliminated, nominal GDP

growth is immediately available by solving the modified Fisher equation of

exchange over any desired time span.

8.

The investment sector debt Ms, in the revised forms of

the Fisher equation (9,17), is generated solely by deposit interest (unearned

income) on the total debt

9.

A new measure

of the debt system liquidity, the circulating debt Mcd, is provided as a

sensitive indicator of the financial health of the domestic economy.

10.

The debt model introduces the concept of “systemic”

inflation as a structural component of the debt system that increases when

interest rates rise and is a major component of CPI inflation.

11.

The level of domestic

earned savings in

12 Western

world economies have become almost entirely dependent on “good” debt

management. Unfortunately, there has been no effective debt management for

decades. That is why economic policy has failed to prevent the boom and bust

cycles in the modern economy. This paper

demonstrates why that has happened and how such cycles can be avoided in

future.

18th May

2009

Tel +64 4 2986890

Email: manning@kapiti.co.nz

More information on monetary reform :

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

Return to : Bakensverzet homepage

"Money is not the key that opens the gates of the market but the

bolt that bars them."

Gesell, Silvio, The Natural Economic Order, revised English edition,

Peter Owen,

![]()

This

work is licensed under a Creative Commons

Attribution-Non-commercial Share-Alike 3.0 Licence.