NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 : 23 January, 2012.

Edition 02 : 21 October, 2012.

Edition 04 : 09 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

The

referenced papers :

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE MISSING LINKS

BETWEEN GROWTH, SAVING, DEPOSITS AND GDP

By Lowell

Manning manning@kapiti.co.nz VERSION 3

21/10/12

Key words: debt, debt model, deposits, deposit interest,

domestic credit, Fisher equation, GDP, growth, inflation, revised Fisher

equation, saving, savings, systemic inflation, unearned income.

CONTENTS:

1. EXECUTIVE SUMMARY

2. BACKGROUND

3. THE DEBT MODEL

4. DEBT AND DEBT GROWTH

5. THE MISSING LINKS

6. CONCLUSION

ACKNOWLEDGEMENTS

The author wishes to thank Raf

Manji and the Sustento Institute for their ongoing support of this research and

Terry Manning of NGO Bakens Verzet for

his perceptive critique and editing of the drafts.

![]()

This work is Licensed under a Creative Commons 3.0

Attribution – Non-commercial – ShareAlike licence.

1. EXECUTIVE

SUMMARY.

This paper brings

together the concepts explored in a series of earlier papers for which links

are given at the top of Page 3. It

summarises the main elements of two of them,

“The Savings Myth” and “ The DNA of the Debt-Based Economy”. Those two papers show how the current account

and exchange settlement processes work, the principles of production in the

debt- based economy and the concept of systemic inflation.

Section 3 describes

a debt model that can be used to analyse the debt-based economy and concludes

with Figure 8. Figure 8 shows “DNA”

helices that relate GDP to accumulated Saving and Growth. The debt model is a

form of the well-known Fisher Equation of exchange revised so it can be applied

to a debt-based economy.

Section 4 uses the

concepts in Sections 2 and 3 to explain debt growth in more detail. It shows

that when the current account is balanced the overwhelming cause of exponential

debt growth is the unearned income derived from the interest banks pay on

banking system deposits. Figure 11 shows the process of debt creation based on

the banks’ risk based capital, the influences of the central bank and how

government debt is generated.

Section 5 explains

how the differences between the historical orthodox “fractional reserve”

explanation of debt expansion and the existing risk-based capital method of

debt expansion arose. The orthodox explanation was based on a Savings and Loan

model of banking that was discarded decades ago prior to the implementation of

the

The paper shows

that interest on the accumulated investment debt (the GDP according to “The DNA

of the Debt-Based Economy”) can only be paid out of productivity gains made

available from new productive investment.

If the productivity gains are insufficient to fund the interest, the

productive sector must inflate to make up the shortfall.

There are systemic

connections between debt, deposits and GDP.

In

The final section

of the paper discusses the links between debt, deposits, and unproductive

saving, and concludes that the entire modern monetary system is based on

inflation. In a debt-based financial

system, household deposits represent the accumulated cost-push systemic

inflation in the productive economy plus the accumulated demand-pull inflation

of the accumulated current account balance. The net international investment

position (NIIP) could be used instead of the accumulated current account

balance.

Except for real

added production, the financial system debt and deposits are determined

endogenously through deposit interest and exogenously through the accumulated

current account balance [or NIIP].

2. BACKGROUND.

This paper explores

the links between Growth, Saving, Deposits and GDP discussed in some of the

author’s previous papers.

The papers are

available at www.integrateddevelopment.org

General summary of all papers published. (Revised edition).

The DNA of the debt-based economy.

The Savings Myth. (Revised edition)

The interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

Unified text of the manifesto of the debt-based

economy.

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition).

How to introduce a guaranteed

minimum income in New Zealand. (Revised edition).

Financial system mechanics explained for the first time. “The Ripple

Starts Here.” (Original

version, not updated. This is now for historical reference only. Other papers

incorporate up-dates and revisions. )

Short summary of the paper The Ripple Starts Here.

(Original version, not updated. This is now for historical reference only.

Other papers incorporate up-dates and revisions.)

Financial system mechanics: Power-point presentation. (Original version, not updated. This is now

for historical reference only. Other papers incorporating up-dates and

revisions.)

This paper relates

mainly to the papers “The Savings Myth” and “The DNA of the debt-based

economy”.

THE SAVINGS MYTH.

“The Savings Myth”

discusses Saving in relation to the System of National Accounts (SNA) used

around the world to measure economic activity and growth. The paper concludes

there are serious problems with the structure of the national Income and Outlay

and Capital Accounts in the SNA and that

“Saving” recorded in the SNA bears little relation to Savings =

Investment as set out in classical orthodox economics. Some of the main features in the paper are:

a) A positive balance of external goods and

services swaps domestic consumption goods and services for foreign capital

assets. It is therefore a negative domestic growth factor in the exporting

country at large and a positive growth factor for that country’s business

interests. While it may reflect domestic economic activity it does not reflect

domestic growth because the income is not spent where it is earned.

b) A study of the nature of the current

account and foreign exchange settlement processes shows there is no such thing

as foreign debt. There is only foreign ownership of the domestic economy in

debtor countries when there is an accumulated current account deficit there.

That ownership can be direct or it can be in the form of commercial paper that represents

claims on the domestic economy.

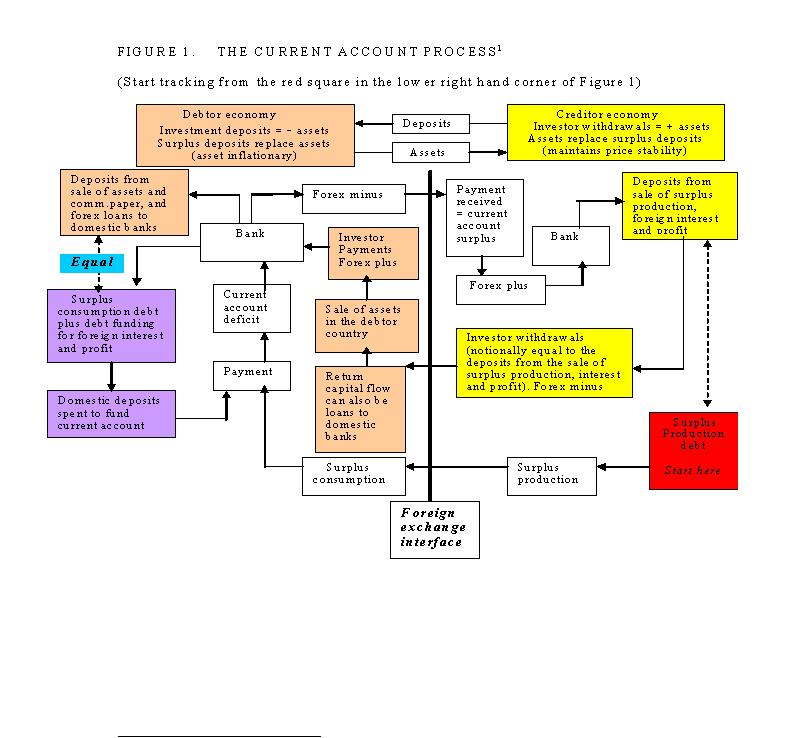

Figure 1 reproduces

Figure 1 from “The Savings Myth”. It

shows how assets and deposits are exchanged through the foreign exchange

interface.

FIGURE 1. THE CURRENT ACCOUNT PROCESS. [1]

{kind=link}

[1] The box

“foreign exchange interface” defining the thick black line representing the

interface between the debtor economy and the creditor economy has been added

for clarity as have minor amendments inside two of the text boxes.

Foreign ownership

of a debtor nation’s economy drains its domestic economic growth through

outgoing current account payments of interest on commercial paper and dividends

and profits arising from the physical foreign ownership of its assets.

Foreign ownership

of a debtor nation’s economy exposes it to high interest rates and the

permanent risk of capital flight.

c) The decline in Saving for Investment is

structural. The decline arises from persistent business demand for faster

depreciation allowances. Part of that demand arises from rapid innovation and

planned obsolescence, but part of it is greed.

Higher depreciation provisions usually increases bottom line profits.

That means faster repayment of investment principal and therefore a lower surplus

for productive investment. Less

productive investment means slower growth. National Saving has been swapped for

short-term profit.

d) The structural decline in national Saving

cannot be addressed anywhere in the world using existing orthodox economic

theory and policy.

e) Non-productive “Savings” schemes around

the world (such as Kiwisaver and the so-called “Cullen” Superannuation Fund in

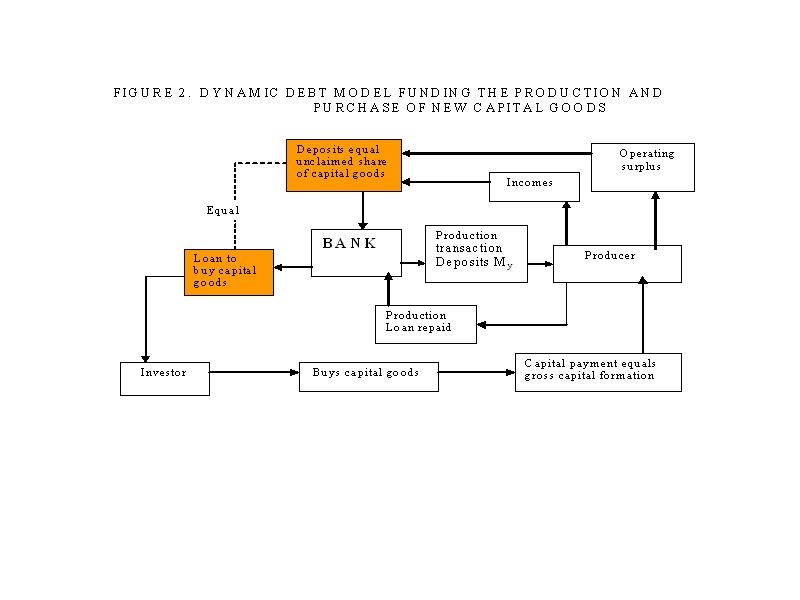

f) Figure 2 reproduces Figure 2 from “The

Savings Myth”.

FIGURE 2. DYNAMIC

DEBT MODEL FUNDING THE PRODUCTION AND PURCHASE

OF NEW CAPITAL GOODS.

{kind=link}

Figure 2 shows that

in a dynamic economy the investment process is internal to the production

cycle. There are sufficient incomes in

aggregate to buy the capital goods produced. Some incomes earned in the

production of capital goods are “Saved” by employees and businesses and

subsequently “Invested” by entrepreneurs who wish to buy them. The internal

lending allows the production loans to be repaid. For simplicity Figure 2 does not separately

include loan interest. Therefore:

Saving =

Investment (exactly as is

found in most orthodox economics textbooks)

The internally self-cancelling

production process shown in Figure 2 is mediated by the banking system. At any

time, the total outstanding loans used to buy the capital goods produced equals

the total outstanding principal still owing on those capital goods (the orange

boxes in Figure 2). Net capital

formation, equals “gross capital formation” as shown in the SNA less principal

repayments on existing capital goods.[2]

THE DNA OF THE DEBT-BASED ECONOMY.

The paper “The DNA

of the debt-based Economy” extends the discussion set out in “The Savings Myth”

and relates the systemic processes taking place in the productive economy to

the Fisher Equation provided by Irving Fisher in 1912 [3]

[2] The System of National Accounts (SNA)

incorrectly uses depreciation instead of principal repayments in its Income and

Outlay account because depreciation is not a financial outlay.

[3]

Irving Fisher, “Elementary Principles of Economics”, 1912. The Fisher equation has been very widely discussed

in relation to the economic difficulties arising from the sub-prime mortgage

defaults in the

in his well-known

equation of exchange that takes the form:

MV = PQ (1)

Where:

M = the amount of

money in circulation

V = the speed of circulation of that money; the

number of times M is used over a given period T

P = the price level of goods and services an

economy produces during time T

Q= the

total quantity of monetised goods and services an economy produces

during time T.

The product PQ is

what is known today as Gross Domestic Product or GDP. Some of the main features

in the paper are:

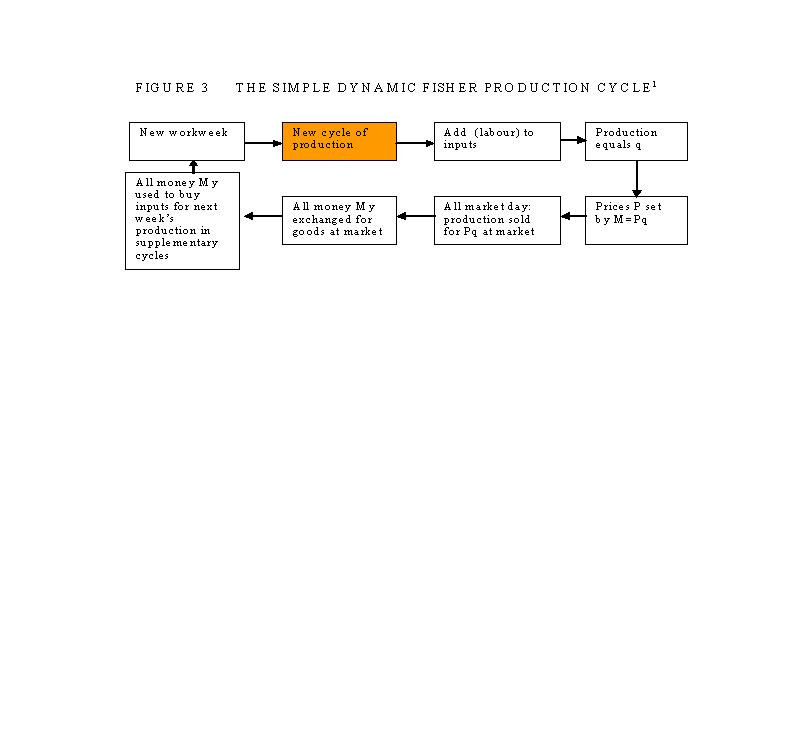

a) Figure 3 reproduces Figure 1 from “The

DNA of the debt-based Economy”.

FIGURE 3 THE SIMPLE DYNAMIC FISHER PRODUCTION CYCLE.

[4]

{kind=link}

[4]

“M” in the original Figure 1 is shown as “My” and “Q” in the original

Figure 1 is shown as “q” (that is, Q=q x V) so the terms are comparable with

those in Figures 4 and 5.

The economic

activity shown in Figure 4 is still self-cancelling because there is no interest

included on the debt. It does not show the internal Saving = Investment

function of Figure 2 which focuses on the production and sale of capital goods

as distinct from the broader Gross Domestic Product (GDP) that includes both

capital goods and consumption goods and services. Figure 4 describes the self-funding,

self-cancelling nature of the economic cycle itself as a whole. The green boxes

show the income (production) side, and the blue boxes the consumption side of

the productive cycle.

Because the market

is held weekly there are 52 weekly markets in a year and so on an annual basis

the speed of circulation Vy of the money My

in the Fisher equation in that case would be 52. Figure 2 also assumes that there is no

hoarding (“saving”) of money so that all the money supply My is used each week.

If that were not so either prices P or output q, (or both) would be smaller.

b) Developed economies are no longer

cash-based as shown in Figure 2.

Instead, they have become debt-based.

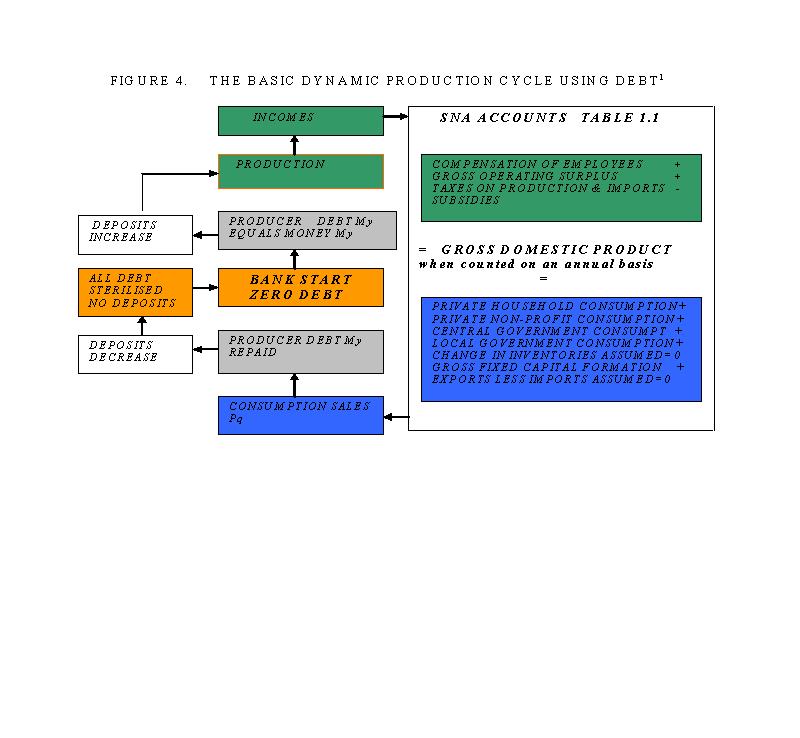

Figure 4 reproduces Figure 2 from “The DNA of the debt-based

Economy”. Figure 4 shows how debt

instead of money is used in the production cycle shown in Figure 2. It also shows how the basic production cycle

relates to the System of National Accounts discussed in “The Savings Myth”.

FIGURE 4. THE BASIC

DYNAMIC PRODUCTION CYCLE USING DEBT. [5]

{kind=link}

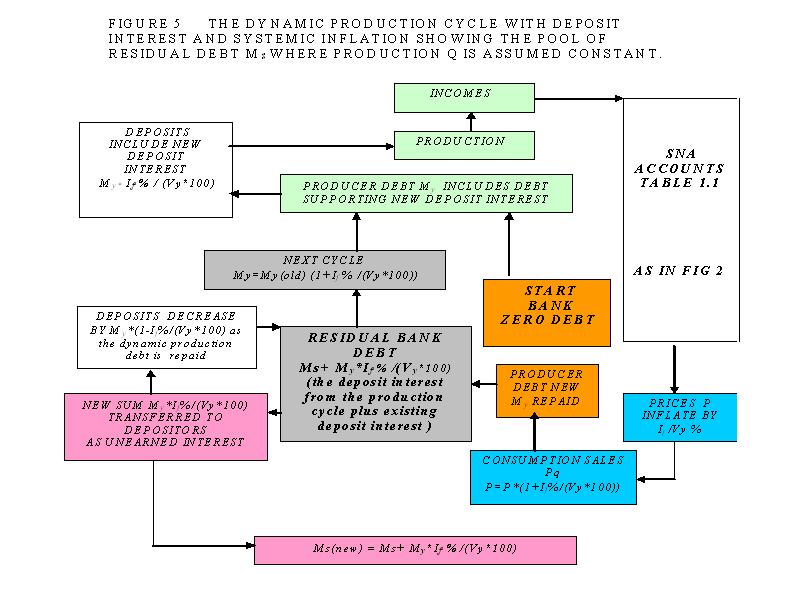

c) Figure 5 reproduces Figure 4 of “The DNA of the debt-based economy” [6].

[5] “M” in the original Figure 2 is shown as “My” and

“Q” in the original Figure 2 is shown as “q” (that is, Q=q x V) so the terms

are comparable with Figures 3 and 5.

[6] Three minor text

amendments have been made to make Figure 5 easier to read.

Figure 5 shows what

happens when interest is introduced into the financial system.

The result is a

build up of debt and interest external to the productive

cycle. The productive cycle is then, in

aggregate, no longer self-cancelling.

Instead, it produces unearned income in the form of interest on deposits

that must be funded by the productive economy.

Unearned income, by definition, produces nothing because it is not

backed by productive activity. In Figure 5 If is the average

interest rate paid on deposits. Ms in Figure 5 is the accumulated

pool of unearned deposit income.

{kind=link}

The price change formula P=P*(1+ If % /(Vy *100))

shown at the bottom right of Figure 5 refers to a single production cycle

producing the (constant) economic

output q.

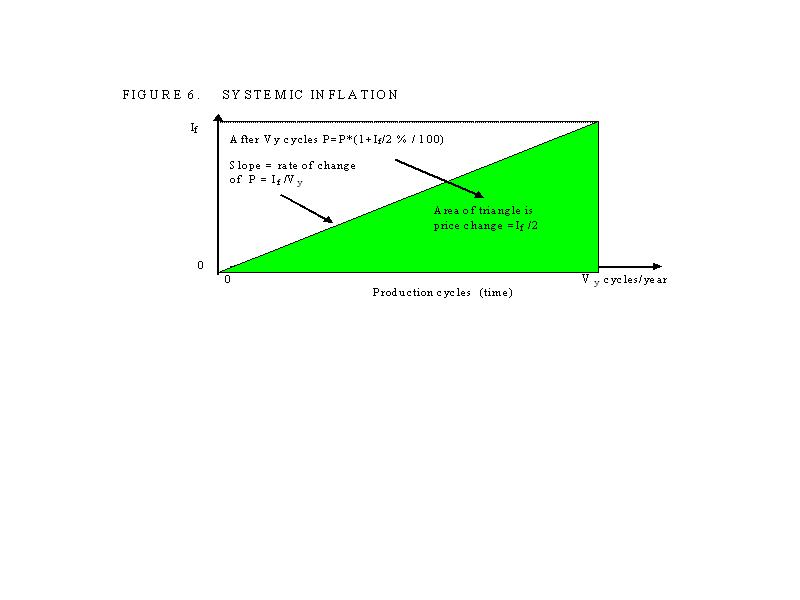

d) Figure 6 of “The DNA of the debt-based Economy” is

reproduced as Figure 6. Figure 6 shows

that, assuming the deposit interest rate If and output q are more or less constant,

physical inflation is half of If %. The figure P* If %

/(Vy *100) is the rate of change of Price P. It must be

mathematically integrated to give the numerical inflation. This aggregate

increase in the annual GDP output caused by the price increases shown in Figure

5 is called systemic inflation.

{kind=link}

Subject to several qualifications, systemic inflation is therefore equal

to half the average interest rate paid on deposits. [7]

[7] The qualifications are that incomes

rise with inflation plus productivity growth, that there are no changes in

indirect taxes included in the price level P, and that aggregate net

contributions to non productive savings schemes are funded by debt from outside

the productive economy.

At this point, the financial system is made up of:

i) the self-cancelling

cycles of production shown in Figure 4 that includes internal Savings =

Investment as shown in Figure 2, funded by a dynamic pool of transaction

account debt supporting the productive

transaction deposits.

ii) the systemic inflation

arising from deposit interest shown in Figure 5 represented by the accumulated

unearned income.

iii) the accumulated debt,

including government bonds, borrowed to service the current account shown in

purple at the bottom left of Figure 1. Deposits corresponding to that debt

arise from the sale of debtor country assets together with commercial bank

foreign exchange borrowing to satisfy the foreign exchange settlement

requirements (top left of Figure 1).

iv) any expansionary “bubble” debt

representing debt borrowed outside the productive economy to fund the purchase of

existing assets.

3. THE DEBT MODEL. [8]

At any point in

time in the debt system there are five broad blocks of deposits and some

circulating currency in the domestic financial system.

They are:

Mt The transaction deposits representing the

productive debt My - M0y so:

My = Mt +

M0y (2)

M0y is

the cash in circulation included in My and used to contribute to

productive output.

Mca is

the accumulated domestic deposits representing the sale of assets to pay for the

accumulated current account deficit. It equals Dca defined below

less the Net Foreign Currency Assets (NFCA).

Ms is

the accumulated deposits arising from unearned deposit income on the total

domestic banking system deposits M3 (excluding repos). [9]

M0 is the total

cash in circulation so that (M0-M0y) is cash hoarded by the public and not

used to generate measured GDP.

The total of Mt + M0y + Mca

+ Ms, is provisionally assumed to be the monetary aggregate M3

(excluding repos) published by most central banks monthly, less the amount of

cash in circulation M0 except for the part M0y that is included in My. M0y is assumed to have the same

speed of circulation as My. In industrialised countries, the

contribution of cash transactions to the measured output of goods and services

(GDP) has been declining in recent decades and their contribution to the GDP

has been provisionally calibrated for the purposes of this paper. [10]

The total debt in

the domestic financial system is assumed to be the Domestic Credit, DC debt

aggregate published by most central banks monthly. [11]

[8] The effects

of secondary non-bank lending are not included in Section 3 but they are

considered later.

[9] Repos refer

to inter-institutional lending.

[10] More accurate

assessment of the cash contribution to GDP over time requires further detailed

study.

[11] At this

point the model does not include secondary non-bank lending thought to be

around 10% of DC. This point is considered in Section 4 of this paper.

[12] The accumulated

sum of capital transfers could be included here, in which case the net

international investment position (NIIP) would be used instead of the

accumulated current account. The decision affects the size of the “residual” Db.

At any point in

time there are four broad blocks of domestic debt in the domestic financial

system. Three of them together add up to DC such that:

DC = Dt + Dca [12] + Dr

(3)

Where:

Dt is

the productive debt supporting the transaction

Dca is the whole of the debt created in the

domestic banking system to satisfy the accumulated current account deficit.

[13]

Dr is the residual debt to balance

equation (3).

Db, is

the virtual “bubble” debt, the excess credit expansion or contraction in the

banking system such that Dr - Db = the debt Ds supporting the

accumulated deposit interest Ms defined above.

Therefore, Dr= Ds+Db. Db can be positive or negative.

By definition in

this paper : My x Vy = GDP; and Ms = Ds

; and Dr=Ds+Db, and

Dt= My-M0y;

and the cash contribution to GDP = M0y * Vy. .

By substitution

into equation (3): [DC = Dt + Dca [14] + Dr

]

[13] This is greater than the monetary deposits Mca

because the banking system may have sold commercial paper to borrow foreign

currency to satisfy the foreign exchange settlement as shown in Figure 8.

[14] The accumulated sum of capital transfers could be

included here, in which case the net international investment position (NIIP)

would be used instead of the accumulated current account. The decision affects

the size of the “residual” Db.

DC = (GDP)/Vy - M0y + Ms + Dca

+ Db (4)

Ms =Ds = (DC – Dca ) – GDP/Vy + M0y

- Db (5)

GDP = Vy *(DC - (Ms +Dca

+Db ) + M0y ) (6)

My = GDP/Vy = DC - (Ms +Dca + Db) + M0y (7)

where the terms are

as defined above.

Equations (4) to

(7) are all forms of the economic debt model shown in Figure 7.

In equation (5),

all the terms except GDP/Vy = My and Db are

known or can be estimated with reasonable accuracy. My can be

approximated in equations (4) and (5) using trend-lines because it is small

compared with Ms and DC. Db is unknown but can be

approximated through model calibration. The calculations in equations (6) and

(7) involve the subtraction of large numbers to get relatively small numbers,

which leaves them sensitive to modelling and data error.

If Ms,

calculated as “the accumulated deposits arising from unearned deposit income on

the total domestic banking system deposits M3 (excluding repos) ” as

defined on page 10, agrees more or less with that calculated in equation (5),

bearing in mind the value of Mb, the proposition that debt growth is

determined by deposit interest will be proven.

The model will require further calibration as further data becomes

available.

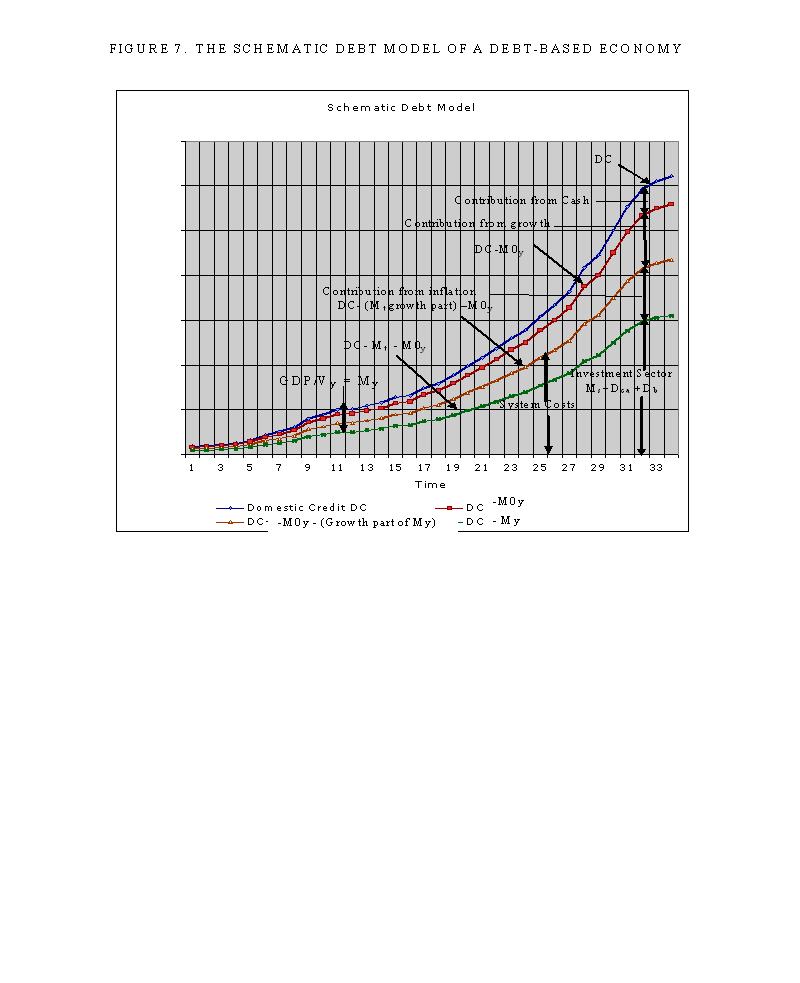

FIGURE 7. THE

SCHEMATIC DEBT MODEL OF A DEBT-BASED ECONOMY.

{kind=link}

Db will be

positive during periods of rapid expansion, particularly as bubbles form, and

will become negative during periods of rapid contraction, particularly as

bubbles collapse. The classic case of this in

[15]

This is discussed at length in the paper “The interest-bearing debt

system and its economic impacts” referenced above.

The dependence of the

gross domestic product (GDP) on the Domestic Credit DC and the interest rate on

bank deposits in the modern cash-free economy from which Ms is

calculated has profound implications for economics.

In the light of the

worldwide financial chaos of 2007-2009 the indicative debt model shown in

Figure 7 provides a powerful argument in support of public control of a

nation’s financial system. In Figure 7, the blue curve (DC+M0y) is drawn to

scale (the total was about NZ $310 b. in

The present

debt-based system shown in Figure 7 leaves the world economy at the mercy of

private banking institutions working for private profit by allowing

irresponsible increases and contractions (Db in equations (4) to

(7)) of the Domestic Credit and its associated bubble formation. The problem is

systemic because the existing financial system requires exponential growth. In

the case of

It probably isn’t

possible to have a simpler model of the economy than equation (7):

My =Nominal GDP/Vy = domestic

credit DC less (accumulated unearned deposit income Ms + the

accumulated current account deficit Dca + the cash contribution to

GDP, M0y plus a correction for bubble activity Db (+/-))

Domestic

The difference

between the two curves is mainly the result of domestic debt needed to fund the

accumulated current account deficit that, in

It does not appear

to be theoretically possible to maintain exponential debt expansion faster than

the GDP expansion over an extended period because the added debt servicing

costs will always leave the productive sector insolvent.

To avoid national

bankruptcy, each nation must maintain, in aggregate, a zero accumulated current

account deficit.

The financial

system is dynamic. The debt used to

purchase capital goods is continually repaid from economic growth. In

aggregate, as long as new investments exceed repayments, both the debt and

deposits expand together. The paper “The DNA of the debt-based Economy” shows

that the total outstanding Saving and the total outstanding debt at any time

are equal to the aggregate sum of economic growth and that this must also equal

the GDP as shown as Figure 8.

The following

three-dimensional diagram (Figure 8) represents the DNA of the debt-based

economy. It is tilted forward from the top to make its features easily

understandable.

The diagram is made up of two

mirrored helical strands of financial DNA. The blue strand represents the total

accumulated GDP output for a given period while the red strand represents the

total outstanding productive investment principal. The vertical axis of the

helices represents time. The diagram shows a random period of four years.

On the blue helix, Vy

bases of production output My are added over the time span needed to

make one full turn of the blue helix (usually a year). On the red helix, Vy

bases of national saving Sy (net new productive investment) are

added over the time span needed to make one full turn of the red helix (usually

a year). For ease of consultation, the bases are shown only for year three. The

drawing shows nineteen of them, as this is the approximate speed of circulation

Vy of productive deposits My in

The helices replicate by

extension. The blue helix showing GDP “dies off” at the end of each period. The

helices grow exponentially by the transfer of net Saving Sy from the

blue helix to the red one over each notional production cycle.

For each of the bases the

national saving Sy is returned to the next production cycle on the

blue helix in the form of net new capital investment Sy (Saving =

Investment) as shown. Individual bases can vary in size (up or down) reflecting

the state of the economy.

The annual length or growth

ring Lz of the blue helix shows the GDP as it accumulates during

that year. The nominal, usually annual, GDP growth in the blue DNA is the

change in length Lz of the DNA spiral over the period z compared

with the corresponding length L z-1 over the previous period. In the

diagram, the length (and therefore the diameter) of the GDP spiral is shown to

be increasing exponentially from year to year.

The annual increase in the

length of the growth ring Lz of the red helix shows the annual increase in outstanding investment

principal S which also equals the nominal GDP growth for that year. The total

length of the red helix at any time is the sum of all outstanding investment

principal. It equals the current

(annual) GDP at any time.

At the end of each (annual)

period z (and only then) the value of output represented by length Lz

of the blue helix (the GDP for that year) equals the value represented by the

whole of the red helix (its total length representing the sum of all

outstanding investment principal).

The plan diameter of the

helices typically expands exponentially. The helices vary together with the

state of the economy. In the case of recessions they show up as changes in the

annual rate of increase of the helix

diameters, and therefore the length of the spiral loops. In the case of

depressions they would show up as an actual

annual decrease in the helix diameters.

FIGURE 8. THE DNA OF THE DEBT-BASED ECONOMY.

{kind=link}

n n+2 n+3 n+4 EACH (BLUE) BASE=My =GDP/Vy![]()

![]()

![]()

4. DEBT AND DEBT GROWTH.

The following

sections of this paper explore the relationships between the debt model

variables and the DNA of the debt-based economy shown in Figure 8. At first

sight, Figure 8 suggests a Saving and Loan model of financial

organisation. It shows that

collectively, those with incomes derived from the production of capital goods

(savers), must invest those incomes by buying the capital goods they have

produced. If they do not do so the

market cannot be cleared of those capital goods unless their purchase price is

borrowed from the banking system. If the purchase price to buy the capital

goods is borrowed from the banking system, there are surplus “hoarded” deposits

held by the savers. Those deposits would then remain in the bank with nowhere

to go other than for non-productive investment in existing assets.

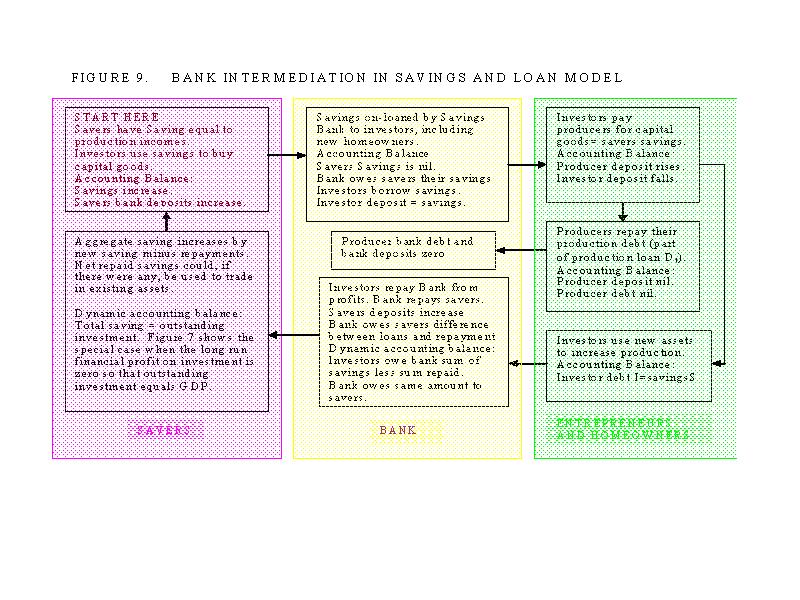

Figure 9 shows a

Savings and Loan model described above. [16] In Figure 9, the Saving deposits

become physically unavailable to the savers for a time. The investor uses them to pay the producers

of the capital goods. The producer uses them to cancel the production debt

created to produce the capital goods. At

the start, the investor has a debt to the Savers and an asset represented not

by a deposit but by the asset itself. At

the end the investor has no debt and the savers regain their deposit (with

interest).

[16] This is an idealised diagram

that assumes producers and entrepreneurs are different groups. This is

discussed further at Section 5.3.

FIGURE 9. BANK INTERMEDIATION IN SAVINGS AND LOAN MODEL.

{kind=link}

In Figure 9 there

is no net bank debt created. The savings repaid by investors to Savers are

available to trade in existing assets. The amount available is the original purchase

price of the assets less the outstanding loans. When an existing capital asset

is on-sold, the purchaser typically borrows the (re) purchase price from the

banking system. The original asset owner

(investor) repays his outstanding debt to the Savers, and, depending on the

sale price and outstanding principal may make a capital gain.

Figure 10 shows

what happens when investment is funded by commercial bank debt rather than

rather than internally from Savers.

FIGURE 10. FUNDING

OF INVESTMENT USING NEW BANK DEBT.[17]

{kind=link}

[17] Figure 10 is an idealised

diagram that assumes producers and entrepreneurs are different groups. This is

discussed further at Section 5.3

The main difference

between Figures 9 and 10 relates to the existence of bank debt. In the Savings and Loan model (Figure 9)

there is no net bank debt involved because the bank has on-loaned the savings

deposits. Savers (at least nominally) do not have access to the their deposits.

Only net repaid investment loans would be available to pay for the exchange of

existing assets. When savings S = Investment I, there are no net repayments.

The bank-funded model (Figure 10), on the other hand, involves bank debt and

Savers have full access to their bank deposits. The dynamic balance in Figure

10 only also holds when the total outstanding investment equals total saving.

Savings S in Figure

10 must be invested in some other kind of investment because there is nothing

new to buy with them. That applies even if it means just leaving them on

deposit at the bank. In the paper “The Savings Myth” savings of this kind are

referred to as a myth. The investment is backed by debt rather than

savings and so does not qualify as investment as required by the principles of

orthodox economics.

The difference

between the Savings and Loan operation where the Savers’ deposits are used to

retire the production debt, and the bank intermediation outlined in Figure 10,

is profound. In the former case, shown

in Figure 9, Savers hold an IOU (rather like a corporate bond) from the

entrepreneurs and new homeowners while the entrepreneurs and new homeowners

have their capital asset on the one hand, and the debt to the savers as a

liability on the other hand. There are

no corresponding deposits in the system because they have been used to repay

the residual part of the production debt Dt.

In Figure 9, savers

lend to entrepreneurs and homeowners while in Figure 10 the bank lends to

entrepreneurs and homeowners. In Figure 9, the Savings are used to retire the

producer debt whereas in Figure 10 the deposits arising from the new bank loans

are used to retire the producer debt. So

Figure10 introduces a new layer of debt and deposits into the system that were

not there before.

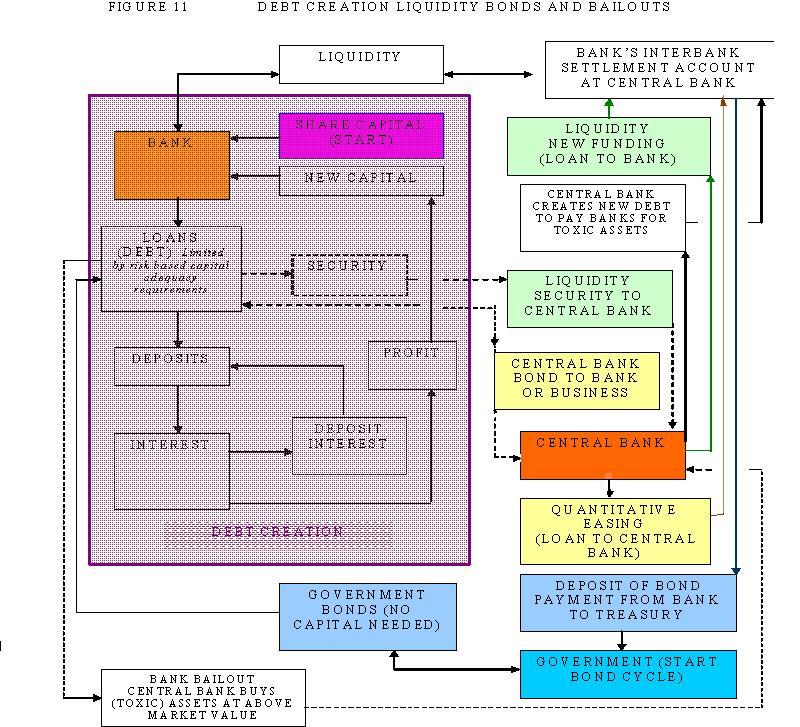

In the

existing debt-based economy almost all money is created as interest-bearing

debt and almost every deposit arises from a bank loan. Borrowers typically sign a loan agreement

before their bank gives them credit by putting money into their bank

account. The bank creates the money out

of nothing. The loan is an asset of the

bank because the borrower agrees to repay it over time. The deposit is a

liability of the bank because the bank allows the borrower to use the money it

has created in return for the interest he or she pays on the loan. The process is shown in Figure 11. For completeness Figure 11 also shows the

role of the central bank in creating bank liquidity, quantitative easing and

bailout funding and the banks’ lending to the government to fund government

debt.

Contrary

to what happens under the savings and loan model (Figure 9), banks never

lend their customers deposits in the debt model shown in Figure 11 because

doing so would deprive the borrower of the right to use of the money they have

borrowed. In accounting terms banks cannot lend their liabilities. This is different to the Savings and Loan

model (Figure 9) where savers do not automatically have access to their

deposits until their term deposit matures. [18]

[18] This is the basis, for example, of the

Investment Pool in the Bank of

From the relationships

shown on page 11 the following derivation can be developed

DC = Dt + Dca + Ds + Db (8)

Of the total, Dt alone

relates to the dynamic transaction account debt used to fund the productive

economy.

The rest makes up the so-called (non-productive) “investment sector” that

trades in existing capital goods and financial assets. The non-productive investment sector

can be called Di such that:

Di = Dca + Ds + Db (9)

Equation (8) is a

modified form of the well-known Fisher Equation of Exchange (M*V=P*Q) described

in Section 2 that takes account of the debt-based economy.

Domestic

DC= M3 – NFCA - R (Residual) [19] (10)

[19]

Many central banks regularly publish financial aggregates that clearly

demonstrate this relationship. Residual includes the banks’ net worth and

several smaller items. NFCA is Net Foreign Currency Assets. As previously noted at footnote 11 the debt

model does not at this point provide separately for secondary non-bank debt,

nor does it allow for a substantial proportion of cash transactions.

Which can be rewritten as

M3- (NFCA + R) [20] = DC

. If the monetary deposit base of the economy

is taken as (M3-repos) rather than M3 to remove the effect of

inter-institutional lending, and since in the productive sector My=Py*Qy/Vy,

and in the investment sector Mi=Pi*Qi/Vi,

equation (8) can be rewritten as the Fisher equation where

(M3-repos)=Py*Qy/Vy+ Pi*Qi/Vi

=(Dt +M0y)+ Di+ (NFCA+R) – repos (11)

Where:

Di is as in equation 9, Pi is

the price level in the investment sector, Qi is the quantity of

investment assets (or alternatively the quantity of investment assets

exchanged) over any given period and Vi is the speed of circulation

of Di. Vi will depend on which version of Qi

is used.

[20]

Except where the entire banking system is insolvent (that is, has

negative net worth), R is a negative number.

NFCA is also likely to be negative in debtor countries (like

Debt growth in the

investment sector is exponential because, as shown in the debt model (described

at section 3 of this paper) any interest rate creates an exponential curve when

the interest is continually added to the existing debt. Debt growth in

the productive sector must also be exponential because the productive sector

has to fund the investment sector debt Di. The growth rate of the

total debt DC will change over time according to the interest rate and physical

changes in the debt base like those arising from the balance of trade,

population growth and productivity.

FIGURE 11 DEBT CREATION LIQUIDITY BONDS AND BAILOUTS.

{kind=link}

The prices of existing capital

assets tend to rise whenever the pool of investment sector debt Di

increases faster than the net value of new capital assets being added to the

investment pool. Asset prices can also be affected when savers (non-productive

investors) "sit on the sidelines" by leaving their deposits "in

the bank". In that case, the speed

of circulation Vi falls, which means either asset prices will fall

or there will be less trading so that Qi falls, or both.

The increase in domestic

debt DC is net of debt repayment, so when some non-bank investors deleverage,

or "take losses" to repay their debt, Di will be lower

than it otherwise would have been and asset prices will tend to remain static

or sometimes fall. In

[21] For example, under the proposed Bank of

England (Creation of Currency) Bill the repeated on-lending of Customer

Investment Accounts would create a very large pool of bank debt outside of the

Domestic Credit or monetary deposit figures.

Call Dnb the pool of all non-bank created debt and call Msnb

the accumulated interest paid to depositors arising from Dnb. Since Dnb

does not directly add to deposits (contrary to Ds which is assumed

to mirror Ms, and Mb which is assumed to mirror Db

in the debt model), then:

DC + Dnb =(Dt + Ds + Dca+ Db)

+ Dnb (12)

M3(-repos) = Mt + M0y

+ Mca + (Ms + Msnb ) (13)

That means that if

interest rates remain comparable, (M3-repos) and DC both have an extra

exponential added to them to supply the extra deposits Msnb. Remembering that

from page 10, Mca=Dca+ NFCA, and (Mt+M0y)=My

then

DC = (Mt+ M0y)

+ [Dca + NFCA] + (Ms

+ Msnb) + repos - (NFCA

+R )

= My + Dca + (Ms + Msnb) + (repos -R ) (14

)

If the

current account is balanced, the overwhelming driver of exponential debt growth is the

interest paid on deposits.

If

secondary lending in the form of non-bank debt Dnb were to become an important factor as it

would, for instance, if the proposed Bank of

From equation (11) DC= Pt*Qt/Vt

+ Pi*Qi/Vi - [(NFCA+R) – repos], when DC increases sharply

the investment sector Pi*Qi/Vi will also

usually increase. Since there is, in

normal times, little reason for Qi to increase sharply or for Vi

to decrease sharply, investment prices will usually tend to rise faster than

the productive economy whenever DC increases faster than nominal GDP growth.

[22]

[22] Qi and Vi can

move in tandem, as, for example, when there is a slump in house sales due to

recession or changes in bank lending criteria, especially when an exchange form

of Qi/Vi is used.

5. THE MISSING LINKS.

5.1 CAPITAL BASED AND DEPOSIT BASED DEBT

GENERATION.

The confusion over how

debt is created is astounding. The box on the left of Figure 11 clearly shows

how debt is created in the present debt-based system. In the capital based

system a bank can and does typically create debt on demand as long as it meets

its capital and liquidity requirements and provided the bank is prudent and has

creditworthy customers.

In the

present debt-based system deposits follow debt creation.

The “competing” deposit

story of debt creation arises from the Savings and Loan model shown in Figures

8 and 9 that follows from the orthodox economic theory shown in Figure 2. That theory states that savings, productive

investment and debt growth are three sides of the same triangle. Savings =

Productive Investment, and the cumulative investment is the cumulative debt

owed by homeowners and entrepreneurs to income earners generally.

In the

Savings and Loan model, debt follows deposits instead. The deposits are

expended to repay the production loans. Savers give up their deposits in return

for an IOU (debt) from entrepreneurs and new homeowners.

The orthodox model

applies only in a Savings and Loan system where the actual Saving is on-loaned

to the buyers of capital goods. In that

case, savers do not have immediate access to their deposits.

The debt system is

not operated on a Savings and Loan basis.

Instead, Savers, as shown in Figure

5.2 INTEREST AND EXPONENTIAL DEBT.

Nominally, the only

deposits in a Savings and Loan system are the dynamic deposits My in

the productive sector. That changes in the debt-based system shown in Figure 10.

Since domestic housing is not usually productive once it has been built, both

the repayments and the interest relating to domestic housing must be funded

from productivity growth if the economy is to remain stable. The productive economy must therefore fund

interest and repayments for both the productive sector and the unproductive

(housing) sector.

Any interest on the

accumulated productive investment debt (GDP in “The DNA of the Debt-Based

Economy”) must be paid out of productivity gains and the corresponding higher

incomes made available through the new productive investment. Otherwise

according to the debt model (equation (11)) prices in the productive sector

must inflate .

The economy will

become unbalanced very quickly if the interest and repayments on new housing

investment exceed what the productive economy can support. If the productive

sector inflates, My in the debt model (Section 3 of this paper) will

expand exponentially even though it is small.

That is exactly what happened when money was used instead of debt in

centuries past and the coinage was often debased by reducing the amount of gold

and silver in the coins. This was done to pay for non-productive expenses, such

as unsuccessfully waging war where the “booty” failed to cover the war costs.

Exchange of

existing capital assets in a Savings and Loan system occurs by selling the

asset for its market value. Any remaining debt on the asset is repaid, and the

new owner re-borrows the new purchase price.

The system remains balanced as long as the market value equals the

original purchase price less the principal repayments already made, its

“residual” purchase cost. If there has been inflation, or if, for some reason,

the new owner pays more for the capital asset than its “residual” purchase

cost, there is nowhere to obtain the extra funding within the savings and loan

system. In that case the additional part of the purchase price must be paid for

from new bank borrowing.

Banks lend money to

make money. The net profit they make on their bank spread (the difference

between the interest rate they charge borrowers and the interest rate they pay

on their deposits) is legitimate income, just like profit in any other

business. The difficulty with the banking system is that more lending typically

means more profit. It is, therefore, in the banks’ interest to lend as much as

they can.

There are four main

ways to increase bank lending.

The first way is by

minimising the contribution of cash transactions counted in the GDP. In many developed economies the cash

contribution to the economy is approaching zero. While there are still a lot of cash

transactions, they add very little to GDP.[23]

Cash in circulation also “uses up” bank capital, because the bank swaps

vault cash (capital) for a customer deposit. The customer deposit costs the

bank far less capital because, unlike cash, the bank can use it authorised

capital leverage when it creates the loan that gives rise to the deposit.

[23] For example, cash is still widely used

in retailing in many developed countries, but the average net profit on those

transactions is small and retailing as a whole makes up only a relatively small

part of GDP (say, 10%). Say, roughly 20% cash transactions x 10% GDP

= about 2% contribution to GDP.

The second way to

increase bank lending is to raise capital by retaining profits or by issuing

new shares. If the authorised bank leverage were 8%, the banks would be able to

lend about 12 times their capital. More

capital means more lending.

The third way to

increase bank lending is to lend to governments, because sovereign debt is

typically, though by no means always, deemed to be risk free. Therefore there are usually few limits on the

amounts governments can borrow as long as the nation’s tax base is deemed large

enough to support the interest payments on the public debt.

The fourth and

possibly most important way to increase bank lending is to pay interest to

depositors. Section 2 of this paper

shows how deposit interest causes systemic inflation. Equation (14) on

page 21 shows that, apart from persistent accumulated current account

deficits, the increase in the

accumulated deposit interest (Ms + Msnb) over time is by far the

biggest contributor to exponential debt growth. In equation (14) when (Ms + Msnb)

increases, debt measured as domestic credit (DC) increases by the same amount.

The work referred

to at the start of Section 2 of this paper is thought to be the first in the

world to demonstrate the systemic links among deposit interest, inflation and

exponential debt growth.

5.3 THE LINKS BETWEEN DEBT, DEPOSITS AND GDP.

The debt model and

“The DNA of the Debt-Based Economy” shown in Figure 8, and Figure 9 hints that

the system deposits should, in some way, be related to My +

GDP.

From equation (13)

on page 21, M3(-repos) = Mt + M0y + Mca

+ (Ms + Msnb

)

Since Mt + M0y

= My, GDP should be directly related to Mca + (Ms

+ Msnb ) in the above hypothesis. The debt model described in

Section 3 of this paper proposes that the quantity of debt determines economic

outcomes in accordance with a modified version of the Fisher equation of

exchange.

The postulated direct link

between the money supply and GDP is the last missing element in the debt model

that already directly links deposit interest, inflation and exponential debt

growth, as noted above. Linking the

money supply directly to GDP will provide further powerful support for the

quantity theory of money and debt proposed by the debt model.

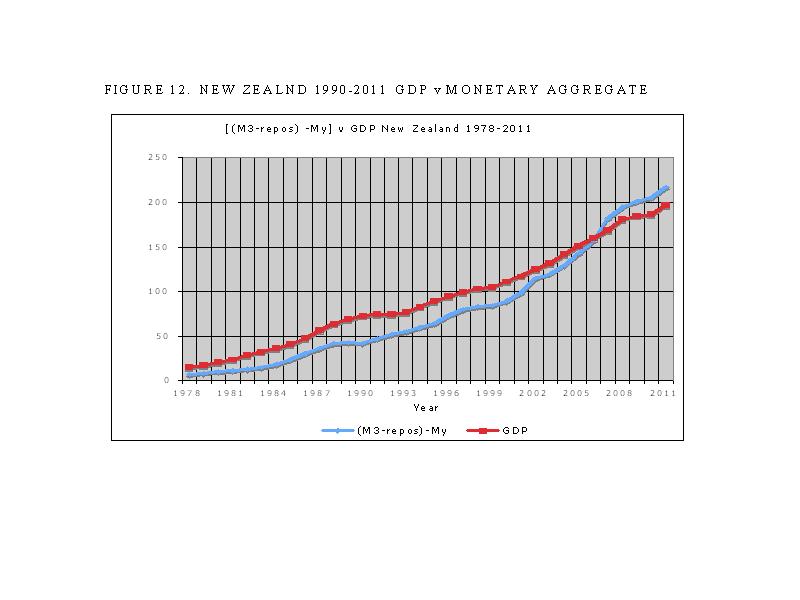

In

Figure 12 gives the figures

for

The purpose of this paper is

to indicate the links between the theory proposed in “The DNA of the Debt-Based

Economy” and the monetary aggregates. There is no reason to suppose deposit

aggregates “should have” followed GDP on a one to one basis in practice. The

“wobbles” about the trend line can easily be related to the boom and bust

periods and the creation and “popping” of bubbles (Db in equations

(8) and (9)).

FIGURE 12. NEW

ZEALND 1990-2011 GDP v MONETARY

AGGREGATE.

{kind=link}

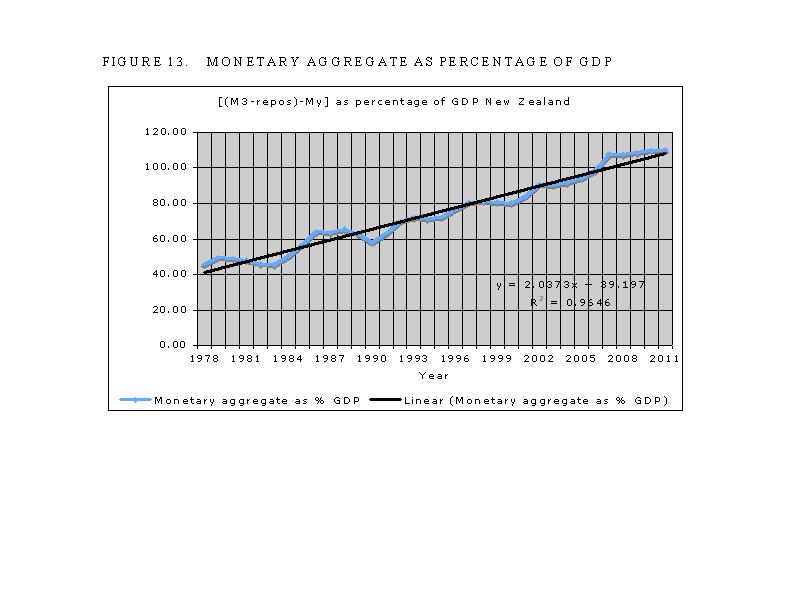

FIGURE 13. MONETARY AGGREGATE AS PERCENTAGE OF GDP.

{kind=link}

There are five main reasons why

there is not a direct one to one relationship between the monetary aggregate

and GDP in Figure 12. Each of those reasons is systemic and can be quantified

with further research.

The first reason is that a lot

of funding of the purchase of capital goods used to be done using the Savings

and Loan model shown in Figure 9. Savings and Loan funding for new capital

assets does not generate bank deposits.

In

The second reason is that

businesses used to retain profits and reinvest them directly in new

capacity. In the idealised funding

models shown in Figures 9 and 10, it was assumed that all the Savings were

saved as deposits and on-loaned to entrepreneurs and homeowners. However, that

has never been wholly so. When producers collectively contribute their own

profits to the purchase of some of the capital goods they themselves produce,

those profits (Saving) are converted to equity. There is then less borrowing

needed from other income earners or from banks. Increased corporatisation and

globalisation in ever more deregulated capital markets have all but eliminated

the retention of profits for reinvestment. [24]

[24]

The third reason the GDP to

deposit ratio has changed is increased social mobility. More people move more

often which creates more sales of existing capital assets, especially

homes. As discussed at page 24, this can

create demand for new bank lending where the amount paid for the asset exceeds

the outstanding debt on the asset. This

applies even though the buyer may have some equity or “savings” either from the

sale of a previous home or from some other source.

The fourth reason is that in

The fifth reason is that

personal incomes have not been rising fast enough to enable most people,

especially homeowners, to meet their capital debt-servicing commitments. The problem arises from growing income

distribution inequality around the world. [25] As that inequality increases,

home ownership typically becomes less affordable. In

[25] This is discussed in the paper “How to

create stable financial systems in four complementary steps.” for which a link

is provided at the start of Section 2 of this paper.

Amounts

attributable to each of the four factors mentioned can be quantified. Further

research will show that, subject to those factors, there is a direct and specific

relationship between banking system deposits and GDP.

Figures 12 and 13,

the debt model, “The Savings Myth”, and the “DNA of the Debt-Based Economy”

demonstrate how very poor public understanding of the financial system

mechanics has produced so much economic instability around the world. The role

of the banks in that overall process deserves wide public debate. The single

most relevant observation from this paper is that the financial system is

fundamentally flawed and requires major systemic review.

5.4 THE

RELATIONSHIP BETWEEN DEBT, DEPOSITS AND UNPRODUCTIVE ‘SAVING”.

Conceptually, no

deposits arise from productive Investment (see Figure 9). Saving = Investment both in orthodox

economics and in “The DNA of the Debt-Based Economy” create debt but no

deposits. According to the debt model

described in Section 3, the fewer deposits there are the less inflation there

will be.

As discussed in

Section 5.3, the real world is, however, different in that the deposit base has

become more like Figure 10 with some add-ons such as the ones derived from the

third and fourth reasons on page 27 and the fifth reason referred to

above. The more bank debt is used the

larger Ms in the debt model will become, increasing the

non-productive investment “savings” pool.

In practical terms

all price is inflation. That must be so because inflation is measured by prices

rises. Those price rises are accumulated over time, so, in the limit, all price

is inflation. “Cost-push” price inflation

is caused by the payment of unearned income in the form of interest to deposit

holders. [26] The unearned income is

funded by systemic inflation in the productive economy. Inflation in the productive economy increases

the prices of new capital assets as well as consumer goods and services. Therefore numerically, the GDP is also almost

entirely made up of inflation and that in turn means that the price of new

capital goods is almost entirely made up of inflation. If the price of new

capital goods is almost entirely inflation, then the debt used to buy them also

reflects that inflation.

[26] The other kind of inflation,

demand-pull inflation occurs when more money is injected into t he economy in

the absence of a corresponding increase in production.

The entire modern

monetary system is founded on inflation.

Section 5.3 showed there are

specific quantifiable links between GDP and deposits. In equation (13) [M3(-repos) = Mt+ M0y

+ Mca + (Ms + Msnb )], the amount (Mt

+ M0y) is the dynamic production deposits My while

the sum

(Ms + Msnb

) is the systemic “cost-push” inflation from the productive sector. Mca

, on the other hand, mostly represents “demand-pull” inflation in the

non-productive investment sector caused by the sale of domestic assets to

foreigners to settle the foreign exchange mechanism in those countries with

accumulated current account deficits as shown in Figure 1.

None of the deposits arises

from choice. They arise from necessity in that they are a consequence of the

current financial system mechanics. The deposits exist. Their owners “invest” them in non-productive

investments. Everything that doesn’t belong to the productive sector My

is by definition non-productive. In

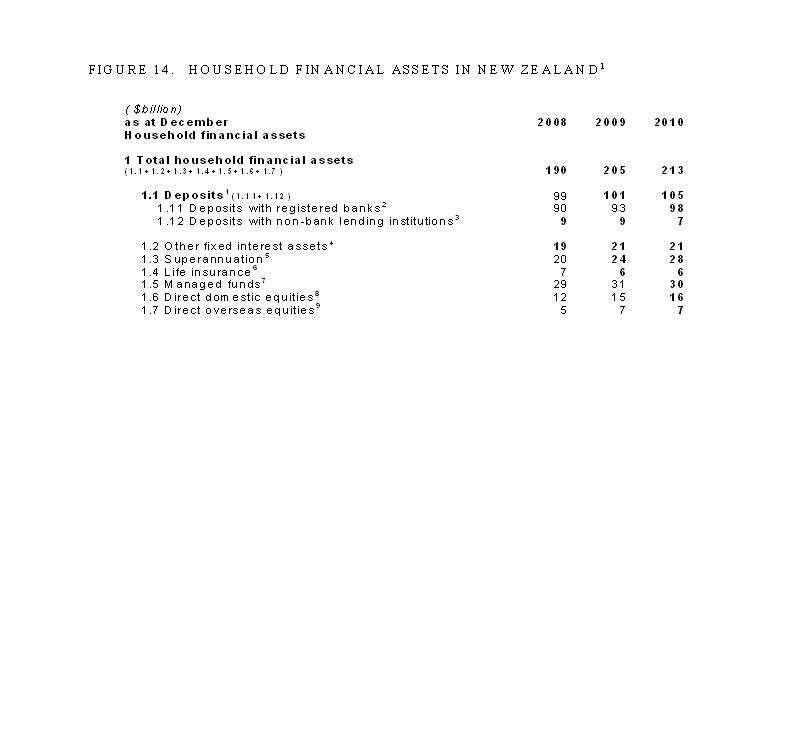

Most countries’ central banks

provide a breakdown of who holds the deposits.

The data for

FIGURE 14.

HOUSEHOLD FINANCIAL ASSETS IN NEW ZEALAND.[27]

{kind=link}

[27] The table is part of Table HA&L

(Household Assets and Liabilities) published by he Reserve Bank of

The household deposits

represent the accumulated cost-push systemic inflation plus the accumulated

current account-based demand-pull inflation of the debt system.

In the case of

In the first

instance, the effect of compulsory saving is to transfer earned incomes to the

non-productive investment pool, Mi , [Mi = Mca + (Ms + Msnb ) from equation (13)]. If consumption remains the same, the

“savings” withdrawals leave less income for debt servicing and to pay for

capital goods forcing an increase in bank borrowing or a decrease in new

capital investment, or both, as discussed at length in “The Savings Myth”.

More generally,

except for added real production, financial system debt and deposits have just

two sources. The first source is the

debt and deposits created endogenously through deposit interest on the

productive transaction accounts in the productive sector (Figure 5). The second

source is the debt and deposits created exogenously through the accumulated

current account deficit debt Dca and the deposit interest on that

part of it (Mca) returned to the debtor country following the sale

of domestic assets to foreigners (Figure 1).

Unproductive

“saving” is determined by the system mechanics. Government decisions requiring

forced saving are like squeezing a balloon.

The contents remain the same until the balloon breaks. Otherwise, an expansion in one place means a

contraction somewhere else. Economic

growth means blowing more air into the balloon instead of squeezing the air it

already holds. The extra air is

generated from increased economic activity. That means jobs, incomes and productive

investment.

Macroeconomic

numbers partner economic activity, they don’t lead it.

6. CONCLUSION

This paper closes

the theoretical loop established in the series of earlier papers for which links

are provided at the top of page 3. The primary determinants of macroeconomic

outcomes are:

* The interest paid on bank deposits.

* The accumulated current account

balance. [28]

* The allocation of productive resources.

* Private debt creation for profit.

[28] The net international

investment position could also be used.

The interest paid

on deposits is the cause of systemic cost-push inflation. Deposits returned to

a debtor country through asset sales to foreigners arising from an accumulated

current account deficit are a cause of demand-pull asset inflation.

Increased

productivity necessary for per capita economic growth requires new productive

investment. Overemphasis on new

non-productive capital investment such as housing distorts the productive

sector because homeowners can only service their debt through higher incomes

and higher productivity.

The confusion

surrounding the orthodox “deposit” based debt expansion of bank “reserves” and

the existing “capital” based debt expansion is historical. The banking system changed from being

“reserve” based to being “capital based” when the Basel I accord became

operative in 1992. In practice the

“reserve” system was also capital based except that the capital requirement was

limited to a fraction of the banks’ transaction account deposits. Government debt did not directly cause

“fractional reserve” debt expansion, but it did then, as now, introduce new

deposits into the banking system thereby expanding the banks’ balance sheets.

The dominant features

of the debt-based interest-bearing financial system are interest paid on

deposits and the accumulated current account balance (or net international

investment position, NIIP). Interest on

deposits creates systemic cost-push inflation in the productive sector, while

an accumulated current account deficit

(or NIIP) creates demand-pull inflation in the non-productive investment

sector caused by deposits arising from

the sale of debtor country domestic assets to foreigners. Those accumulated

current account deposits also create a deposit interest feed back loop that

adds to systemic inflation.

The paper shows the

entire modern monetary system is founded on inflation, and that there is a

systemic relationship between GDP and the monetary aggregate (M3-repos). The

rate of change of the exponential growth curves [(M3-repos) – the dynamic

production deposits My]/GDP has been linear in

This paper is based

on a debt model of the debt-based economy that shows that world debt cannot be

managed without removing unearned income from the system caused by the payment

of interest on bank deposits and by balancing each nation’s current account.

THE

REFERENCED PAPERS.

The

referenced papers :

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

Return to : Bakens Verzet

Homepage

"Money is not the

key that opens the gates of the market but the bolt that bars them."

Gesell, Silvio, The

Natural Economic Order, revised English edition, Peter Owen,

This work is licensed

under a Creative

Commons Attribution-Non-commercial Share-Alike 3.0 Licence.