NGO Another Way (Stichting Bakens Verzet),

1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02 :10 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org.

NEW Capital is debt.

NEW Comments on the (Jaromir Benes and Michael Kumhof) Chicago Plan Revisited

Paper.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

![]()

This

work is licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence

CAPITAL IS DEBT

By

Version 4 09/02/13

For background work

see:

http://integrateddevelopment.org http://sustento.org.nz

The world is

now locked in a debt trap.

You can have debt

without capitalism but you cannot have capitalism without debt.

Nor is it possible to

have debt without interest, or usury as it has been called through much of

recorded history. All major religions ban usury because the payment of interest

transfers wealth as unearned income from borrowers to lenders. That means the major religions morally ban

debt. Despite that, those with money to start with or who could mint it or

plunder it or control it have almost always been financial and political

winners. That is still the case today.

As Stephen Zarlenga

in “The Lost Science of Money” says

“[B]y misdefining

the nature of money, special interests have often been able to assume

the control of society’s monetary system, and in turn, the society itself.” [1]

This paper will

show that in the capitalist system there must be debt to enable the purchase of

capital goods and that the amount of debt used to purchase new productive capital goods defines

productive economic output (savings=investment). Because productive debt and economic output

in the capitalist system are closely interwoven, capitalism = use of debt. No

debt, no capitalism.

The bond between

capitalism and debt does not necessarily hold in reverse. There have been

periods in history long before the advent of capitalism when communities have

gone deeply into debt and had to be rescued through debt jubilees such as the

one proposed in The Manning Plan referred

to in this article.

In this day and

age, practically all money is created as interest bearing debt by private

banks. As a result, most of the world is now locked into a debt trap and usury

is almost universal. Interest is justified by “lending risk” even though the

lenders nearly always take separate security in full for the debt.

The online

There are a lot of similar definitions that also fail to take one of the

basic features of capitalism into account: that investment money usually has to

be borrowed [2].

Monetary reform

proposals like those referred to in this paper must take all debt into account

if we are to retain some form of capitalist economy. The alternative is to

adopt some other cooperative or mutual form of economic organisation. Economic

organization evolving over the coming decades might replace capitalism as we

know it today; or it might be a hybrid of capitalism that embeds cooperative

locally distributed production and consumption, shared use of the commons for

the public good and even, perhaps, subsistence systems.

Traditional

hoarding has been replaced by deposits in banks.

Most monetary

reform proposals (with the exception of the Manning Plan )

fail to account for and manage total debt and interest rates thereby leaving

the existing capitalist economy intact. In the longer run they will accentuate

the glaring problems of income and wealth distribution, global environmental decay and widespread injustice, especially at the

cost of women, that characterize the present system.

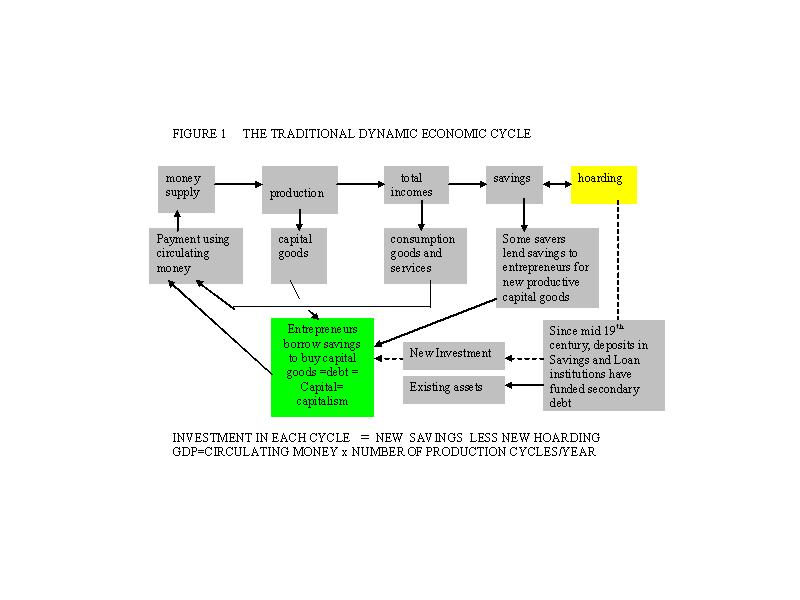

In Figure 1, if hoarding is stable, the value of consumption goods and

services and new capital goods matches total incomes. There is enough income to

“clear the market” and exchange all production. Conceptually, some people in a

traditional cash-based economy save some of their income and on-lend it to

entrepreneurs to invest to buy the new capital goods. Savings = investment is

one of the cornerstones of orthodox economics. The money supply is relatively small because most of it is

recycled with each cycle of production and consumption.

FIGURE 1 : THE TRADITIONAL DYNAMIC ECONOMIC CYCLE.

{kind=link}

INVESTMENT

IN EACH CYCLE = NEW SAVINGS LESS NEW HOARDING

GDP =

CIRCULATING MONEY x NUMBER OF PRODUCTION CYCLES/YEAR.

Figure

1 represents a capitalist Savings and Loan model of economy and it forms the basis

of the equation Savings = Investment found in most orthodox economics

textbooks.

In

Figure 1, not all savings are invested, so that in practice new Investment =

(Savings minus hoarding). As long as the hoarded savings remain constant as a

proportion of all savings and there is no interest paid on the investments,

inflation-free growth in the Savings and Loan model shown in Figure 1 is

limited only by resource constraints and monopolistic business behaviour.

The

main change in the Savings and Loan model over time has been that for most of

history savings were physically hidden because there were no deposit banks,

whereas these days most savings are “banked”[3] as shown at the lower right of

Figure 1.

Despite appearances, the

Savings and Loan economy of Figure 1 is far from being debt-free. Assuming the

money supply itself is debt-free, as was the case when coin was the primary

means of exchange of goods and services, the total debt accumulated in the

system is the sum of outstanding loans provided by savers to entrepreneurs plus

that loaned to exchange existing capital goods. Hoarded money was taken out of

circulation (frozen) and did not begin to participate in the real economy until

Savings and Loan institutions developed. Savings and Loan deposits were on-loaned, typically to governments

and local authorities, increasing the total debt.

In the debt system the

accumulated net savings owed by entrepreneurs in Figure 1 is the sum of

outstanding productive capital

investment or, more simply the capital employed in the economy.

Capital is debt, and therefore capitalism is

debt-based.

Orthodox economics texts are

unanimous in defining investment in the equation Savings=Investment as investment

in new productive capacity as shown in Figure 1. In practice, economies

have never behaved the way orthodox economic theory would have us believe

because many people invest in non-productive and existing productive capital

assets like housing and stocks and bonds, creating a non productive “shadow

economy” now called the “investment sector” or “paper economy”.

With a constant rate of

saving, when savings are directed into non-productive investment instead of new

capital goods (productive capital), economic growth in the Savings and Loan

model of Figure 1 must stall unless new money is injected into the financial

system to compensate for the losses to the investment sector. The growth of the

investment sector means that either productive capital has to be generated from

somewhere else to compensate for the withdrawals from the productive economy or

disposable incomes in the productive economy must fall rapidly. In the present

financial system debt to feed the investment sector and prevent failure in the

productive economy is created by private banks for profit. This is discussed in

more detail later in the paper.

Payment of interest further

complicates the basic structure shown in Figure 1. Savers must have “an

incentive to invest” otherwise they would either hoard their surplus income or

spend it. In Figure 1, as long as the savings go into new productive investment

as orthodox economic theory requires, the productivity gains from the

investment should be sufficient to allow both for interest payments and for

repayments of principal. If the financial surplus from the new investment is

not enough to pay both principal and interest, the new investment project will

not proceed.

On-lending of savings for

production creates productive debt for capital goods while non-productive

investment creates secondary debt for existing assets as shown in Figure 1.

There is always a total debt equal to the outstanding loans in both the

productive and the investment sectors whether the financial system is based on

interest-bearing debt issued by private banks or whether it is based on

debt-free money.

Failure by economists to take

the debt in both the productive and the non-productive sectors collectively

into account and their insistence on viewing public debt as independent from

the total debt shows just how limited their understanding of the present

financial system is.

Periodic debt jubilees freed debtors from the

need to repay their debts.

Figure 1 suggests that debt

has been around almost as long as money has been used. There are several documented

cases of whole countries being bankrupted because the (typically

non-productive) investments they made with borrowed money failed. [4]

The debt that forced debt

jubilees thousands of years ago was probably also a kind of unproductive “pre

Savings Bank” savings and loan debt broadly similar to that shown at the lower

right of Figure 1. Peasants may have had to borrow during hard times to

maintain their existing production, especially when that production was used to

supply the lender’s “city”. The land was often held in common by a tribe or

clan. The impoverishment resulting from the payment of interest usury left

little alternative to forgiving the debt. Without the produce from the land the

“city” itself would die. That historical process may have been a precursor to

the feudalism that swept through parts of

For a long time most investment was non-productive.

Historically, interest rates

on borrowed money tended to be high. There was little productive investment

because there were few savers willing to lend and not much new technology to

invest in. Even many of the wealthy elite hoarded their money. [5] The green

coloured text box in Figure 1 shows that in a Savings and Loan system “some savers lend savings to entrepreneurs

for new capital goods”. The church(es) and nobles used their “savings”

to build cathedrals, churches, castles, manors and stately homes,

and had little incentive to invest in new technology. They represented an

extraordinarily tiny elite of land-based feudal aristocrats that persisted

until the industrial revolution transferred what the French economist Francois

Perroux called the “dominant revenue” from land to industry.[6] That was one

reason why, until the industrial revolution, lending became concentrated within a small group of

goldsmiths, money lenders and merchants.

Capitalism

has been resisted almost since it began with European colonial expansion, the

introduction of improved agricultural methods and land enclosures. From the

Levellers in England in 1648 with their manifesto “Agreement of the People” and

the Diggers of 1649, to the Chartists and their Peoples Charter of 1838,

through Marx and Engels’ famous Communist Manifesto of 1848 [7] to the Paris

Commune of 1871, the Communist Revolution in Russia of 1917 and the broad

Fabian and Labour movements of the late 19th and 20th centuries,

people have been fighting to retain ownership of the commons and (in some

cases) the means of production. The various commons movements reject free

market capitalism to a greater or lesser extent insisting that the nation’s

resources belong to everyone and should not be sold to or stolen by capitalists

for profit.

While earlier movements were

sometimes motivated by religion the later ones were based on the understanding

that the wealth generated by colonial expansion and the industrial revolution

was not being shared then any more than it is today. Whatever definition of

capitalism you choose, when “a country’s trade and industry are controlled by private owners for

profit “ (from the on-line Oxford dictionary referred to above) there is, by

definition, little room for cooperation or the common good or even for the

planet itself. The bottom lines of self interest and profit are all that

matter.

The negative effects of the enclosure of the

commons.

Marxism and the other modern

social movements grew in the cities due to urbanisation. Peasants didn’t live

in large groups and didn’t travel much. In

The capitalist enclosures of

land haven’t stopped. Ongoing resource exploitation by privileged corporations

encloses the land and the sea as much or more than the agricultural elite ever

did because they cover the whole world (or much of it). These days, knowledge

is enclosed in the form of patents over almost everything imaginable, from

individual genes that occur in everyone’s body, to the seeds and medicines we

buy. Even the airwaves, water, education and general healthcare are being

enclosed in a far more aggressive and insidious manner than the land enclosures

in earlier times. Perhaps, most importantly of all, money itself has been

enclosed as described in this paper.

In a broad sense modern

enclosures represent ongoing efforts by capitalism to monetise the commons. The

more of the world and what it contains can be monetised (and therefore counted

in GDP) the greater control capital has over the world and everything that

lives on it. In medieval times very little was monetised. Most people sold or

exchanged only what they produced over and above their subsistence needs so

relatively little money was needed. The advent of modern debt-based banking has

enabled much more of the world to be monetised. Further monetisation of human

activities and assets requires capital. Ongoing monetisation is a therefore

feature of capitalist expansion.

The arrival of Savings and Loan institutions.

As long as hoarding reduced

the circulating money supply it severely limited productive investment and

growth. When the money supply was constant, investment was dependent on the

savings income earners were willing to on-lend. The creation by statute of

“Savings and Loan” institutions like the Post Office Savings Banks in countries

such as

From the mid 19th century, the secondary

on-lending of savings deposited with Savings and Loan Institutions therefore

tended to increase debt without directly increasing the money supply. Instead

of growth of the money supply the speed at which the existing money supply

circulated increased. The Savings banks paid interest on their clients’

deposits, generally in the region of 2-3%. Savers were then “hoarding for

profit” instead of hiding it and taking it out of circulation.

The critical element of the

Savings banks and other secondary lenders such as building societies, lodges

and the like was that they often lent for non-productive purposes like new and

existing residential property. The actual construction of new houses is part of

the productive output (GDP) but new houses themselves are not new productive capital investments because they do not add any new productive capacity.

While the activity of building is

productive, the investment by the

house-buyer in the property itself is not. Housing debt is part of the grey

box “new investment” at the lower centre of Figure 1. The money used for

initial construction activities first makes a round of the productive cycle

then some of it finishes up “hoarded” in existing assets. The buyer on the

other hand usually finishes up with just a large long-term non-productive

interest-bearing debt. Productive transaction account money is used to build a

house but capital (usually debt) is

needed to buy it.

Traditionally, while wealthy

elites built vast palaces, housing was not a very important part of ordinary

family investments. In many areas of the non-industrialised world this is still

the case today. Increasing housing expectations (bigger and better houses, more

and better fittings and the like) have become an Achilles heel of the

capitalist system. The proportion of incomes committed to housing has

skyrocketed, depriving the economy of productive investment. That is why nobody

in developed capitalist economies can find a way to provide “affordable

housing”.

The interest payments on those

non-productive loans for housing had to come out of productive sector incomes as

did the principal repayments on the original amount borrowed. That is not

possible in the Savings and Loan model of the economy shown in Figure 1 without

injection of new money into the financial system because the speed of recycling

of savings could not increase quickly enough to meet the extra demand for

housing finance. The immediate result of rapidly increasing non-productive

lending for housing tended to reduce disposable incomes and deflate the

productive economy. To avoid deflation, ever more new money had to be injected

into the financial system. Instead of the same pool of money circulating

faster, some way had to be found to make the pool of money itself grow.

Companies and limited liability legislation led

to a high demand for private debt and the expansion of industrial capitalism.

One early response to the lack

of money in countries where precious metals were being used for coins was to

reduce the amount of precious metal in the coinage. [8] Another way to increase the money supply was

to create what is called fiat money in

the form of tokens or banknotes that have no intrinsic value. That has been

done at various times throughout history.

Until the British Parliament

passed the Joint Stock Companies Act in 1844, companies in

Limited

liability was not available in

The result of such limited

access to capital prior to the early decades of the nineteenth century was that

in

Notwithstanding the limitations in the Bank Charter Act, the new

legislation opened the door to a vast expansion of demand for private debt and

greater risk-taking to fund industrial expansion once James Watt’s patents [35]

on the steam engine expired in 1800. Boulton and Watt produced just 496 pumps

and engines under patent in 25 years up to 1800 and 1164 by 1824, but they gave

Inflation was negligible for six hundred years.

The introduction of steam

technology and rail led to rapid industrialisation and greater urbanisation

that reduced the excessive weather dependence of income earners nationwide.

Despite the changes in population demographics, the mass of peasants and others

who had few assets and very little money continued to hoard what little money

they had. [12] At that time, few ordinary people had bank accounts, in part

because there was no network of deposit banks where most people lived. People

had hoarded their savings for more than 500 years because there had been little

or no inflation. Many people continued to do so after the mid-nineteenth

century because there was still no inflation despite the introduction of

Savings banks in

For most of the period 1300-1900 only a relatively small proportion of

the total economic output was monetised. Except in the towns, families

generally consumed and exchanged what they produced. Moreover, while prices for

staple commodities varied wildly in the short term, there was considerable

elasticity of demand because many people could shift to cheaper alternative

products. The Savings and Loan model shown in Figure 1 coped well with the vast

increases in output through the industrial period until long after World War

II, as well as with war inflation that doubled prices in both WWI and WWII. The

legislative changes previously referred to enabled the money supply to grow and

savings to be recycled and there was relatively little interest-bearing private

bank debt. The new regional banks helped power what is called the Second

Industrial Revolution beginning in the mid 19th century as the

development of steam technology reached its peak and railways expanded.

Productive investment is the sum of all

outstanding current and past investments.

The productive investment from

the green box in Figure 1 “Entrepreneurs

borrow savings to buy capital goods =debt =Capital = capitalism” can be

accumulated over time. The total

productive investment at any time must then equal the sum of the outstanding principal

on current and past investment. The total national economic output (Gross

Domestic Product or GDP) is also a function of the circulating money supply in

Figure 1. To the extent GDP is created through productive investment rather

than monetisation of existing production there must be a direct relationship

between the outstanding productive debt and GDP at any given point of time.

[13] A good case can be made that much if not most of measured economic growth

in recent decades results from monetisation of existing non-monetised output

rather than any actual growth in GDP. Child care, elderly care, the fast food

industry and a sizable part of the healthcare industry are just a few examples

among many.

If we accept the definition of

capitalism as “an economic

and political system in which a country’s trade and industry are controlled by

private owners for profit, rather than by the state” (or something

similar), then the available productive capital is represented in Figure 1 by

the cumulative outstanding invested savings so that:

No productive investment means

no capital and no measured economic growth (the increase in GDP output measured

as shown below Figure 1) other than what arises from monetisation of existing

activities. In Figure 1, as an economy becomes more monetised the physical

money supply must be increased to avoid deflation.

The use of new fiat money came with the Bank of

In the absence of enough precious metals, notwithstanding the 19th

century gold rushes, the money supply problem and the associated supply of

productive capital were eventually resolved by creating new fiat money. When,

starting in 1690, the American colonies began one by one to print their own

fiat money (called colonial scrip) to fund their economic expansion, their

economies boomed because their money supply increased. The colonies injected

publicly-issued and owned debt-free fiat money directly into new productive

economic activity. That increased the money supply pool in Figure 1. There was

little inflation because population growth and economic development were both

high. More money and more production produced more saving and more productive

capital for investment.

In 1751 the British government

restricted the use of colonial scrip but did not ban it entirely. The

restrictions related to using the colonial bills as legal tender to repay debt

that was likely to have been lent in sterling. The British government action

caused a classic extension of the issues arising from Figure 1. It was

impossible for the American colonies to expand without new money just as it was

impossible to expand the British industrial economy without new money, even

with the use of split tally sticks. [14]

Split tallies were a form of Government fiat money that had already been

in use in

The creation of the Bank of

England in 1694 provided a new source of fiat money.[16] The actions of the

bank have often been misrepresented because government debt had been around for

many centuries. The new feature of the Bank of England was that its first loans

to the government were created as perpetual

interest-bearing debt. Subsequent debts to the bank were not perpetual and

many of them were eventually repaid. The main drawback of the Bank of England

was that it was established as a privately owned joint stock company. Its debt

was issued at interest for private profit. That represented a major change from

the tally sticks created by the government and the colonial scrip created in

America.[17] The Bank of England’s ability to create notes was strictly

regulated and its main source of income for many years aside from Government

debt was in the discounting of commercial Bills. For a time, Bank of England

notes were “as good as gold”.[18] The Bank’s main function in its early years

was providing interest-bearing loans (debt) to the government to fund

government deficits during the political instability of the 18th

century when increasing taxation was politically impossible. In 1719 it was,

however still a small lender. At a time when the government debt was £50 million the Bank of England’s share was a little over £3 million, in the same order as that held by the British East India

Company. By contrast the South Sea Company held nearly £12 million.

Individuals held the rest of the government debt either in the form of

redeemable debentures or as annuities (pensions).

The Bank of

Most government debt in the

early 18th century represented the secondary lending of individual

savings. As already mentioned, government expenditure did not necessarily directly

increase productive capital in the green box of Figure 1, though there may have

been “downstream” productive capital raising by government suppliers.

Prior to the onset of the

industrial revolution the Bank of England’s impact on the British economy was

small.

“The 18th century was a period dominated by

governmental demand on the Bank for finance: the National Debt grew from £12

million in 1700 to £850 million by 1815, the year of Napoleon's defeat at

The vast bulk of that debt was

created during the Napoleonic wars though not all of it was Bank of England

debt. Referring again to Figure 1, the new wartime money created as

interest-bearing debt was added to the money supply while existing manpower and

resources were mostly diverted from existing productive output to the

non-productive military. Unlike previous centuries, plunder was usually

insufficient to pay for war even when you were on the winning side. And unlike

the American colonies, Bank of England debt creation allowed more new money to

be circulated than was offset by population growth or increases in

productivity. Private secondary lending to the government accentuated that

effect. Prices and incomes in

The Napoleonic wars increased

government debt but they did not necessarily increase the capital base in the

green box of Figure

Industrialisation and much

greater productivity allowed the money supply to be increased while at the same

time creating substantial financial surpluses (saving) that could be recycled

into new productive capital investment and secondary investment as shown on the

right hand side of Figure 1. From 1861, as previously mentioned, ordinary

people could bank their savings in the Post Office Savings Bank where their

deposits were government guaranteed, thereby reducing hoarding and providing a

new pool of Savings and Loan investment funds [20]. Throughout this period and

later, most bank loans were business overdrafts that directly supplied new fiat

money to the productive circulating money supply (today’s productive

transaction account balances) in Figure 1.

The rapid increase of debt-based money came

with financial deregulation.

As late as

The subsequent period of

deregulation in

By 2003, the debt situation in

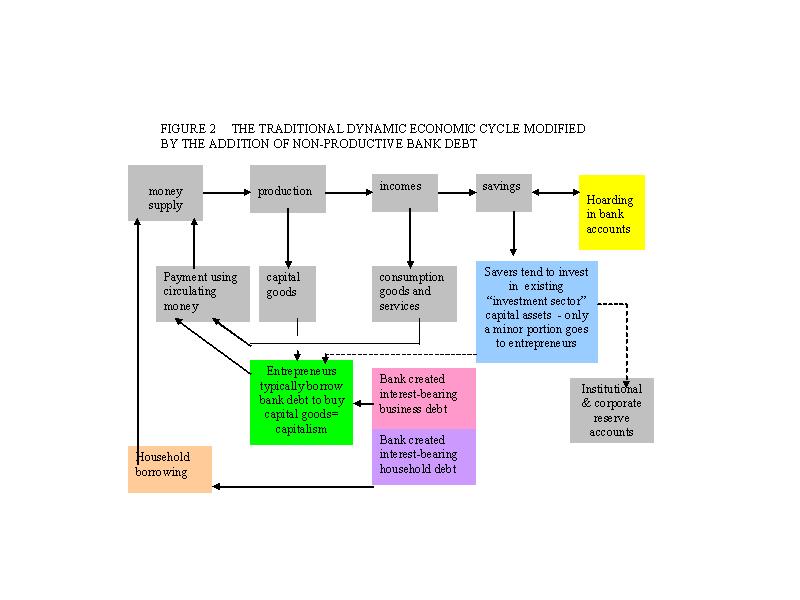

In Figure 2 existing savings

in the blue box are no longer being recycled primarily into new economic

activity as they were in Figure 1. They are instead typically channelled either

directly or through so-called institutional investors into the exchange of

existing non-productive assets. In that sense they perform the same function as

the Savings and Loan institutions previously described. To the extent the

savings end up in institutional transaction and reserve balances secondary

lending is on a one to one basis and there is no cascading effect from multiple

secondary lending.

The financial revolution was

that the savings in the savings and loan structure of Figure 1 that previously

funded new productive investment were replaced by new bank debt as shown in the

pink box of Figure 2 while at the same time the secondary non-productive debt

in Figure 1 was also replaced with new household bank debt shown in the

lavender box of Figure 2. That new bank debt for households is mainly

circulated as mortgages, student debt and credit card debt.

{kind=link}

The

closed money supply shown in Figure 1 has been replaced by the open ended money

supply in the form of interest-bearing bank debt shown

in Figure 2.

The resulting increased money

supply created as interest-bearing debt created greatly increased capitalist

opportunities for private profit seeking, especially in the private financial

sector. That is, referring again to the French economist Francois Perroux, when

the “dominant revenue” switched from the industrial sector to the financial sector

where it has remained ever since.

The speed of circulation of the money supply

has reduced as interest-bearing bank debt has increased.

One effect of the change

appears to have been a reduction in the speed of circulation of the money

supply. It may now be less than 1 because, as shown in the yellow box of Figure

2, there is less secondary (non-bank) debt because not all bank savings

deposits are recycled into circulation. Since savings deposits are liabilities

for the banks, the banks cannot on-lend them. For practical purposes, except

for deposits on-loaned on behalf of and with the express authorisation of the

deposit holders, bank savings deposits are withdrawn from circulation, or

frozen.

Historically, the speed of

circulation of the debt-free money supply in Figure 1 may have been roughly

2.5.[24]

A reduction in the speed of

circulation of the broad money supply in Figure 2 means there is a much larger

pool of money and therefore much more profit for the financial institutions

that have created nearly all that money supply. The banking system itself has

become a parasite on the productive economy because its financial power arises

from exponentially increasing privately created interest-bearing debt. Aside

from providing day to day banking services the banking sector does not

contribute to the economy. Instead, its retained profits constitute savings in

Figure 2 that under existing banking rules it can use to create new debt at the

rate of about $12 for every $1 saved. It also passes to deposit holders

unearned interest income on their rapidly rising pool of hoarded savings

causing systemic inflation in the productive economy as described earlier. More

debt leads to more interest, more inflation, and an exponentially expanding

banking sector so that the current financial system is truly capitalism run

amok.

The profound difference

between Figures 1 and 2 is the introduction of additional interest-bearing bank

debt in the pink and lavender boxes in Figure 2.

The amounts involved are now

vast. The banks’ interest income, their claims or lending rate less their

funding or deposit rate, used to be based on a relatively small amount of bank

debt. The interest now being paid on a vastly increased volume of

interest-bearing bank debt has been the primary cause of inflation and the

boom-past cycles in recent decades.[25]

Figure 2 is simplified for

clarity. In practice, the supply of capital for business or accumulation of

funds and debt for the man in the street is not entirely limited to bank debt.

As shown by the dotted line at the centre right of Figure 2, share offerings

and issues of debenture stock and other financial paper still occur, but Figure

2 is a reasonable first approximation. These days businesses borrow from banks,

so banks supply the bulk of entrepreneurial capital as well as day to day

working funds. They add their own bank interest “spread” or margin to the

interest they pay on the resulting deposits, thereby increasing the price of

debt for their own profit. Instead of one cost of borrowing, the interest paid

on savings as in Figure 1, there are now two. The borrower must pay the cost of

interest paid by the bank to the depositor (the “savings” in Figure 2) and the margin cost of interest (the

bank spread) to the bank. As discussed above, that has set the capitalist

system (inflation, debt growth and interest) into overdrive in comparison with

the Savings and Loan model shown in Figure 1.

After the US dollar was de-linked from gold in

1971, the banking system captured the money supply for profit.

The monetary revolution was

that deregulation allowed the private banking system to capture the money

supply for profit once the US abandoned the US$ gold peg in August 1971. Once

US dollars could no longer be converted into gold, bank deregulation meant that private bank debt world-wide suddenly

became 100% fiat money with few controls on the amount of debt created.

The monetary revolution has

reinforced capitalism through increasing the money supply for profit. As

previously described, the interest on that money supply creates a feed back

loop that continually transfers wealth from debtors to deposit holders and the

financial sector, inflating both the “savings” in the investment sector and the

productive capital investment required to generate GDP.

The financial system mechanics

now force the money issued in the form of interest-bearing private bank debt to

grow exponentially to fund both non-productive investment and productive business

expansion.[26] Few people these days

borrow from modern day savings and loan institutions such as finance companies

because the interest rates they charge on their loans are typically much higher

than the interest cost of newly created private bank loans.[27] This means that

multiple on-lending of credit-based savings with a higher speed of circulation

has been replaced by the creation of new debt which conceptually circulates

just once, though there is some secondary lending in most countries that

slightly increases the speed of circulation.

Interest-bearing debt increases exponentially.

In heavily indebted countries

like

In the present deregulated

debt-based system, the amount of new debt being fed into the financial system

through the pink and lavender boxes shown in figure 2 is constrained only by

the risk-based capital requirements of the Basel Accords that set out how much

the banks can lend relative to their own capital, and by the regulatory policy

settings such as Central Bank official cash (interest) rates, designed to

manage the physical market demand for new debt. The “regulatory” settings work

very poorly because the systemic customer demand for new debt precedes any

consideration of central bank reserves.

Most of the demand for new

debt is systemic. As shown in both Figures 1 and 2, debt growth is inherent in

the debt-based financial structure through the payment of interest or usury on

loans. That is the case whether or not the debt is secondary Savings and Loan

debt as shown in Figure 1 or bank debt as shown in Figure 2. Much of that

interest is justified on the basis of measured inflation but according to

detailed papers available at the websites shown at the top of this paper, there

is a systemic feedback loop that means inflation is related directly to the interest

rate paid on deposits. Deposit interest represents “something for nothing”

because it produces nothing, becoming instead a burden on the productive

economy.

In the absence of high

productivity gains, the money supply in Figure 2 must increase by both the

principal of the new non-productive loans in the lavender box, by the interest

paid on those loans and by the new productive loans in the pink box, causing inflation in the productive

sector. That inflation creates an exponential debt spiral along with a

corresponding exponential price spiral in the productive sector. In addition,

the invested savings shown on the right hand side of Figure 2 create a parallel

exponential growth of prices in the investment sector. (See “The DNA of the

Debt-Based Economy” on the referenced websites.) Assuming interest rates are

constant, the bigger the debt in the lavender box becomes and the more new

interest is payable on it the faster the total debt load on the productive

sector will also have to increase.

Interest paid on investment

sector debt is inflationary and falls within the definition of usury because

the depositor literally gets something for nothing. The interest must be funded

by the productive economy creating an imperative for GDP growth that rests at the

heart of capitalist economic expansion.[30]

Private banks can create far more debt than

their shareholders have invested.

Both the Savings and Loan

model of the economy shown in Figure 1 and the bank debt model shown in Figure

2 generate new debt. Both of the models are capitalist to the extent that

entrepreneurs use debt to pay for productive capital investment. The former

(after savings banks were established as shown at the bottom right of Figure 1)

is a mixture of new productive debt and secondary debt while the latter is

mostly private interest-bearing bank debt loaned on the basis of the leverage

allowed by the Bank of International Settlements in Basel that sets the rules

about how much banks can lend in relation to their capital. That enables private

banks to create far more debt than their shareholders have invested in the

banks. In addition, Savings and Loan savings, particularly within the Figure 1

model, can create a cascade of secondary debt that all monetary reform

proposals need to take into account.

In Figure 1, as long as

savings keep being recycled into new

productive investment a constant level of new productive investment can be

maintained with the same money supply. In that case, the debt entrepreneurs

have to savers, the total productive capital,

increases. The same is true with multiple recycling of savings into the

non-productive investment sector to exchange existing assets.

In the bank debt system shown

in Figure 2 there is, subject to several important qualifications, a one to one

relationship between debt and capital assets, both productive and unproductive.

The qualifications include the need for the accumulated current account to be

in balance, secondary debt (such as corporate bonds in the

In Figure 1 the secondary debt

is built up through the cascading effect created by Savings and Loan

institutions through the multiple recycling of depositors’ savings as

authorised by Statute. The historical figures do not lie. Prior to World War I

inflation was low because secondary debt was relatively modest and relatively

little interest was paid on bank deposits.[31].

In Figure 2 on the other hand,

if the productive circulating money supply in the productive sector is to

remain constant the interest paid on the productive debt (the pink box in

Figure 2) must either be recycled into consumption or it must be replaced by

new interest-bearing money creation by private banks. The interest on that new

money must be added to the interest on the existing money supply and, because

all the interest has to be borne by the productive economy, the new money will

cause inflation. Inflation increased this way after World War I because interest

on the non-productive war debt had to be added to the circulating money supply

just when more hoarded savings were being banked and the rate of economic

expansion from the industrial revolution was tailing off.

The exponential increase of interest on bank

debt causes inflation.

Those inflationary pressures

have accelerated in recent decades because of the rapid endogenous (internally

self-generating) increases in bank debt caused by the systemic exponential

increase of unearned interest referred to above. Moreover, the attempts to

manage those inflationary pressures using interest rate policy have been the

direct cause of modern business cycles and financial crises. As mentioned

previously, when total debt increases, capitalism concentrates financial power

in ever fewer hands.

In summary, both the secondary

debt of the Savings and Loan structure shown Figure 1 and the bank debt shown

in Figure 2 are inflationary when interest is paid on deposits and savings are

recycled into existing capital assets instead of new productive investment.

Accumulated current account deficits in debtor countries like

The lower the interest paid the lower the rate

of inflation.

One obvious practical response

to avoid inflation is to reduce interest rates toward zero, especially deposit

interest rates.

Capitalism is inherently

inflationary because it relies on interest-bearing debt whether that debt is

bank debt as in Figure 2 or secondary debt as in Figure 1.

Successful reform proposals must stop the march

of unbridled capitalism.

With the idea of reducing

interest rates to zero, several monetary reform proposals aim at nationalising

the issue of money. Some of those proposals first appeared nearly a century ago

before inflation and exponential debt growth became a major concern. At least 5

of them involve a public monetary authority issuing all new money

interest-free, thereby removing the ability of private banks to create new

interest-bearing debt.[32] All 5 seek to undo the banking revolution of the

1980’s based on the model shown in Figure 2 and return to the model shown in

Figure 1.

There are several advantages

to the reform proposals. They eliminate new interest bearing bank debt entering

the economy. The proposals all involve a government appointed monetary

authority issuing new money debt-free and interest-free into the economy

instead of its being loaned into the economy at interest. Four of the proposals

do this initially in a sort of “big bang” debt jubilee.

In the remaining proposal, The Manning Plan, new debt-free interest free money would be

progressively introduced in the form of a universal basic income. Some of that

new money would be used to cancel existing bank debt while the rest would be

loaned back to the monetary authority at a low interest rate for recycling into

new productive capital investment.

The proposals all tacitly

accept that there will be secondary interest-bearing debt generated through

Savings and Loan facilities as shown in Figure 1, whether or not that secondary

lending is mediated by the commercial banks. However, only one of the

proposals, The Manning Plan, manages both the quantity and

price of secondary debt. The other proposals deny (both conceptually and

practically) the cascading effect of both the quantity of secondary debt and

the interest rates paid for the use of that debt.[33] Escalating

interest-bearing secondary debt can still concentrate capital just as privately

issued interest-bearing bank debt has done, though probably at a slower rate. The Manning Plan attempts to limit concentration of that

capital. The other proposals do not, despite the best intentions of their

authors.

Secondary debt must be included in the total

debt figure.

This paper has dealt with the

historical impacts of secondary lending within a fiat-based monetary system

shown in Figure 1. Further research is needed to confirm the speed of

circulation that existed in developed economies before and after the

deregulation of the 1980’s. The value of secondary debt from official records

will need to be added to the bank debt (Domestic Credit) to get the total debt.

The same can be done for the present banking system, taking great care not to

double count secondary debt. Those figures can then be carefully compared to,

say, GDP to get a Total Debt / GDP ratio, making sure that “apples are being

compared with apples”.

The advantages of good

monetary reform are better control of both the total money supply (debt-free

money plus secondary debt) and the price of that money. One without the other will not necessarily

improve the financial system. Apart from the Manning Plan,

the existing monetary reform proposals do neither because they neither manage

the amount of secondary debt nor do they sufficiently manage its price.

Productive and non-productive public and

private debt together make up the total debt.

Total debt determines the

status of the economy in a reformed financial system that allows the recycling

of a debt-free interest-free monetary base because the real money supply is the

sum of the original debt-free interest-free system deposits plus the total

secondary debt arising from recycling those deposits. Total deposits alone no longer

represent the actual money supply.

A tiny elite has now “enclosed” the total money

supply for its own profit.

Capitalism involves debt creation

of all kinds and is just one of several tools available for the generation of

economic activity in a world with little real or cash money. In recent times,

the quantity and price of debt have been abused, allowing a large pool of

unearned interest income to be accrued through usury. Due to the systemic

effects of that usury the money supply in the non-productive investment sector

has finished up in the hands of a tiny financial elite. That is characteristic

of both the Savings and Loan model of the economy described in Figure 1 and the

Debt-based model described in Figure 2. The main difference between the two

models is that in Figure 1 capitalism and power over money tend to be more

diffuse because at least some of the money supply is under public control. In

the debt-based monetary system in Figure 2 both capital and power over money

are concentrated in the hand of an ever smaller elite.

Under capitalism as defined in

this paper “a country’s trade and industry are controlled by private owners for profit”. Most of the world

is now “controlled

by private owners for profit”. The public commons are

being “enclosed” down to the genes in our bodies and the water, food and plants

we depend on for survival. For the first time in history money itself has been

“enclosed” for private profit.

At a more theoretical level

this paper has shown that Capitalism is Debt-based, where just a few control

the money supply and the debt load is borne by others. In the debt system, debt gives birth to

money. For every dollar of debt there is a dollar claim on money created

somewhere, whether or not there are bank deposits backing those claims. The

bottom line is that Capitalism has created a financial elite that accumulates

the money while leaving the corresponding debt as an everlasting burden on

society at large just as it has consumed the earth’s resources and left the

mess for society to clean up.

Monetary reform must serve the public good.

As for models for monetary

reform Alperovitz and Dubb, referring to the

“For decades, to many the only longer term

choices have seemed to be state socialism

or corporate capitalism. But new approaches may also begin to pose

new systemic ideas for a longer term progressive structural change that is both

quite American in content, and quite radical in its vision of a system beyond

the traditional models.”[34]

This

paper has shown that to be useful, those new systemic monetary reform ideas

must reverse the enclosure of the public commons and they must manage debt and

money for the public good. Managing money is not the same as managing the

amount of bank deposits. If capitalism is to remain part of our economic and

social structure, “control”, “ownership” and “profit” in the definition “control of trade and industry by private

owners for profit” will all have

to be heavily moderated in favour of the public good. With the exception of The Manning Plan , the monetary reform proposals referred to

in this paper do not do that, so that as they are presently formulated, they

are insufficient to satisfy any “vision

of a system beyond the traditional models”.

End notes:

[1] Stephen Zarlenga “The Lost Science of Money” American

Monetary Institute 2002, ISBN 1-930748-03-5, p3.

[2]

[3] Savings were often

under a hearth where they could survive a house fire and easily be recovered.

In days gone by house fires were extremely common.

[4] The Court of Phillip IV of

[5] There was large-scale hoarding in medieval

[6] The numbers of those in the nobility

(including the church) was tiny. For example there were just 13 Earls in , a couple of small villages or hamlets. Most of the

remaining 20% were knights. Elite numbers fell to about 2000 as the population

decreased during the plague years. Much later, in 1688 when the population of

England was about 5.2 million, Gregory King estimated their number to include

about 186 lords (Dukes, Marquises, Earls, Viscounts, Barons and 26 “spiritual”

lords of the church), about 600 knights, 3000 squires and 800 baronets.

Baronetcies are usually hereditary titles but do not qualify for a seat in the

House of Lords. During the 17th and 18th centuries monarchs

sold baronetcies when the crown was desperate to raise money. There are now

excellent records for the nobility from baronet up and it is possible to work

out exact numbers at any given time.

[7]

http://www.marxists.org/archive/marx/works/1848/communist-manifesto/

[8] Fiat money is like cash today where the notes

and coins have no intrinsic value. When gold and silver were used the coins

were “worth” what they bought. When the coinage was debased by reducing the

amount of precious metals in it, as famously happened in the “Great Debasement”

of Tudor England, the coins still had some intrinsic value. They were a hybrid

of precious metal and metal with little or no intrinsic value. Fiat money has

been used on and off for thousands of years in

[9] http://en.wikipedia.org/wiki/Bank_Charter_Act_1844 (downloaded 25/1/13)

Due to

recurrent crises the Act was suspended in 1846,1857 and 1866. [see [19]]

“ Under the Act, no bank

other than the Bank of England could issue new banknotes, and issuing

banks would have to withdraw their existing notes in the event of their being

the subject of a takeover. At the same time, the Bank of England was restricted

to issue new banknotes only if they were 100% backed by gold . The Act served

to restrict the supply of new notes reaching circulation, and gave the Bank of

England an effective monopoly on the printing of new notes. The Act exempted

demand deposits from the legal requirement of a 100-percent reserve which it

did demand with respect to the issuance of paper money. Until the

mid-nineteenth century, commercial banks in

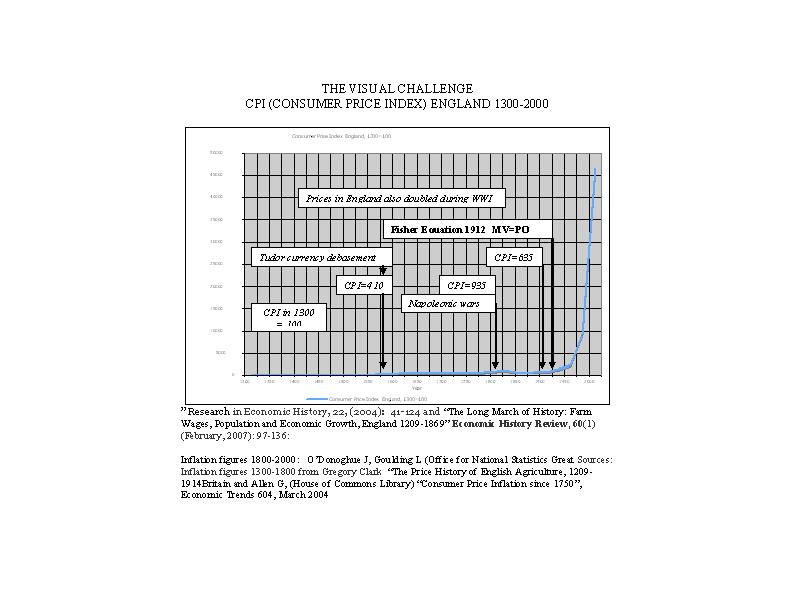

[10] (FIGURE 3) THE VISUAL CHALLENGE : THE CPI (CONSUMER PRICE INDEX)

ENGLAND 1300-2000.

{kind=link}

[11] There is considerable research on the

population in

[12] In

[13] There is a lengthy analysis of this by

the author in the paper “The DNA of the Debt-Based Economy” published at http://www.integrateddevelopment.org/lowellDNApaper20110805.htm

The author’s estimate of GDP for more than 5 million people in England in 1300

is less than 2 million pounds.

[14] The split

tally stick was a kind of fiat money widely used for more than 700 years.

Tallies were issued by the crown (exchequer) as receipts for government

purchases and could be used in payment of taxes. They were transferable, so

stocks (the larger pieces of the split tallies) on which the details were

inscribed also circulated as money. The crucial role played by split tally

sticks from the time they were introduced in

[15] http://www.ukpublicspending.co.uk/uk_art20_uk_government_spending_from_1600_to_present.html where there is a graph from work done by Professor Gregory Clark. The spikes in the

chart are major wartime periods especially the Napoleonic wars and WWI and

WWII.

[16] See Sir John Clapham “The Bank of England” 2

volumes, Cambridge University Press, 1944 for a definitive history. Many of the

Bank’s records survive and they provide details of most of the key events from

the time it was created.

[17] The tallies were not always interest free, as

some monarchs like King Charles II sold them at a discount to raise cash.

[18] Gold convertibility was suspended during the

banking crisis of 1797 and again during WWI.

[19] http://www.bankofengland.co.uk/about/Pages/history/major_developments.aspx#4

[20] http://postalheritage.wordpress.com/2011/09/16/150-years-of-the-post-office-savings-bank/ A few cooperative banks existed long before

Post Office Savings Banks were established. One of the most famous of these is

the Monte dei Paschi di

[21] Source: New Zealand Official Year books.

[22] Source NZ Official Year Book 2004 p 438

[23] The reason for the change

was the sale of Post Bank to ANZ in 1989. It was fully subsumed into ANZ by the

year 2000.

[24] Research by the author hints that the speed

of circulation in medieval

[25] According to Friedman and Schwartz in their

monumental book “A Monetary History of the

[26] This assumes for simplicity that all the

domestic debt funding and accumulated current account deficit has been returned

to the debtor country in the form of reverse capital flows. (And vice versa for

accumulated current account surpluses).

[27] Though there are well developed secondary

debt markets in a few developed countries like the

[28] The Net Foreign Investment Position can also

be used. While the burden of the accumulated current account deficit falls

ultimately on households, the major financial causes of

[29] Until recently the

[30] The methodology and management of interest

rates is beyond the focus of this paper, but they are supposedly managed by the

central bank. In

[31] In

[32] They are:

- The Social Credit Movement founded by Major Douglas in the

1920’s.

- The Chicago Plan proposed by Fisher and Simons and supported

by Friedman that was recently revived in an IMF paper “The Chicago Plan

Revisited” by

Kumhof and Benes.

- The “Bank of England – Creation of credit Act” promoted by

Positive Money in the

- The “National Emergency Employment Act” (NEED Act) promoted by

the American Monetary Institute (AMI) in the

- The Manning Plan

proposed by the author of this paper

(available at the websites referred to at the beginning of this paper.)

[http://www.integrateddevelopment.org/manningplan20120913.htm ]

[33] The AMI NEED Act does cap some secondary

debt interest rates at 8% including bank costs but that is still more than

sufficient to create massive systemic inflation.

[34] http://www.commondreams.org/view/2013/02/01-9 1/2/13

[35] http://mises.org/daily/3280 (James Watt)

ACKNOWLEDGEMENT

The author is greatly indebted

to Terry Manning of the Netherlands NGO Bakens Verzet for his careful editing

of this paper.

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org.

NEW Capital is debt.

NEW Comments on the IMF (Benes and

Kumhof) paper “The Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English edition, Peter Owen,

![]()

This work is

licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence.