NGO Another Way (Stichting Bakens Verzet), 1018

AM

SELF-FINANCING, ECOLOGICAL,

SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S POOR.

|

FREE E-COURSE

FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 : 24 June, 2011.

Edition 02 : 08 August, 2011.

Edition 03 (revised) : 12

September, 2011.

Edition 05 : 09 February,

2013.

(VERSION EN FRANÇAIS PAS

DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE

SAVINGS MYTH

By

We

are almost blind when the metrics on which action is based are ill-designed or

when they are not well understood.[1]

Key Words: accumulated current account deficit, CPI, current

account deficit, debt, debt model, debt growth, deposit interest, domestic

credit, exponential debt growth, E-notes, Fisher equation, foreign debt,

inflation, national accounts, NFL, revised Fisher Equation, saving, savings,

SNA, systemic inflation, unearned income.

|

CONTENTS: 01. EXECUTIVE SUMMARY. 02. BACKGROUND. 03. THE SYSTEM OF NATIONAL

ACCOUNTS. 04. THE CURRENT ACCOUNT

PROCESS. 05. CAPITAL FLOWS AND THE

PURCHASE OF CAPITAL GOODS. 06. CHANGES IN INVENTORIES

(STOCK). 07. “SAVINGS” THAT DO NOT

QUALIFY UNDER THE SYSTEM OF NATIONAL ACCOUNTS. 08. RE-EVALUATING AND

CORRECTING NET SAVINGS AND RELATED ENTRIES IN THE NATIONAL ACCOUNT. 10. CONCLUSION. 11. BIBLIOGRAPHY AND

ACKNOWLEDGEMENTS. APPENDIX 1. DERIVATION OF

SAVINGS FUNCTION FROM THE STEM OF NATIONAL ACCOUNTS. APPENDIX 2. COMMENT ON THE

NEW ZEALAND SAVINGS WORKING GROUP (SWG) REPORT TO NEW |

Page |

01. EXECUTIVE SUMMARY

This paper reviews the nature of saving in a

debt-based economy and the System of National Accounts (SNA) used

internationally to represent national economic outcomes.

The most important account in

the SNA system [2] is the Gross domestic product (GDP) and expenditure

account. In

[1] Stiglitz et al 2009 p. 9.

[2] See United

Nations, 2009. The appendices set out the order of the SNA

tables.

A

trade surplus swaps domestic consumption goods and services for foreign capital

assets.

The “gross operating surplus” used

in a country’s national income and outlay account (Table 1.2 of the national

accounts) must reflect the final net figure from the Gross domestic product and

expenditure account after taking into account the purchase of foreign assets to

satisfy the balance on external goods and services.

The forced purchase of foreign

capital assets resulting from a positive trade balance reduces the real growth

in the domestic economy of the exporting country compared to what it otherwise

would be, because there are fewer consumption goods and services left to buy

there and no corresponding domestic incomes to buy them with.

A

positive balance of trade therefore tends to be a negative domestic growth

factor in the exporting country at large and a positive growth factor for that

country’s business interests.

An increase in the trade

balance should be deducted from the

presently measured domestic growth of the exporting country because it does not

properly reflect the real growth of its domestic economy. There is no such

thing as an “export-led recovery” because a positive balance of trade does

nothing in aggregate to improve the well-being of consumers in the exporting

country. Potential economic growth in the exporting country is swapped

for foreign capital assets that narrowly benefit business interests instead of

those of the wider community. The national accounting effect is to reduce

domestic credit and deposits below what they would otherwise have been.

The “Saving” presently shown

as a residual in the National income and outlay account [3] of the National

accounts prepared under the international System of National Accounts is a

myth. It does not satisfy the fundamental orthodox economic principle of

Saving equals Investment where

“investment” is defined as productive investment in new capital goods.

[3] For example Table

1.2 of the New Zealand National Accounts published by the NZ Department of

Statistics.

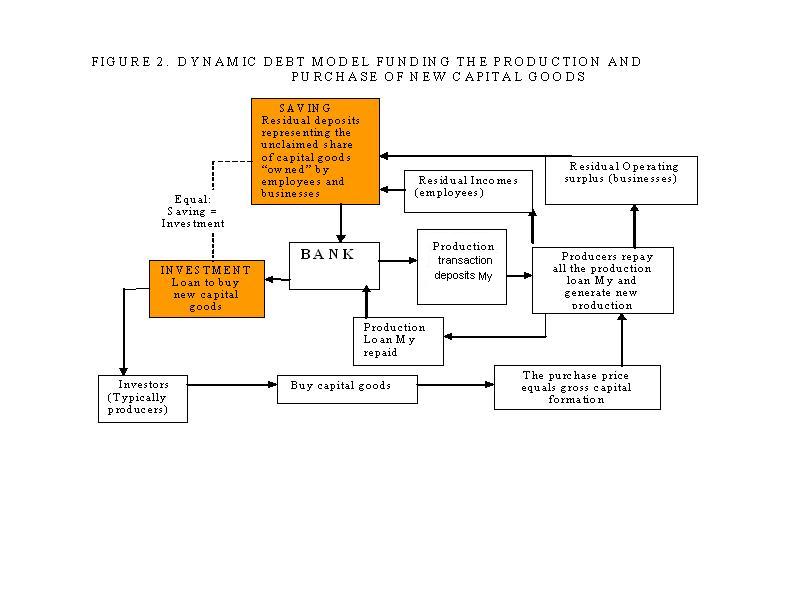

The debt model referred to in the

introduction (Section 2) of this paper shows that the production and purchase

of capital goods takes place within the productive sector of the economy.

The process is discussed at length in Section 5 of this paper and illustrated

at Figure 2. To comply with orthodox theory the SNA National income and outlay

account must comply with equation (1) in the paper, namely:

S = DI – C

(1)

Where:

Saving S in equation (1) equals the transfer of productive

income from income earners to the purchasers of new capital goods within the

productive economy,

DI is disposable income from the National income and

outlay account, and

C is final consumption expenditure also taken from the

National income and outlay account.

For S to satisfy equation (1)

it must equal gross capital formation as stated in the SNA less the

principal repayments being made on existing capital goods. S is not a residual as the present national

accounts claim. It is a real number based on the sale price of

capital goods produced over any period of time and the principal loan repayment

schedules required by lenders during the same period. When the Saving S, as it

is defined above, is entered into the “use of income” side of the National

income and outlay account, the account, in its present form, no longer

balances.

The National income and outlay account fails to

balance for four reasons:

(a) because it includes the current account balance on

one side only of the account, and

(b) it includes the full value of inventory changes that have little real value,

and

(c) it is based on depreciation (a wealth statistic

used for taxation purposes) instead of the financial cash flow in the economy

represented by principal repayments, and

(d) the residual gross

operating surplus is the figure from the gross domestic product and expenditure

account before taking account of foreign assets purchased abroad to satisfy the

balance on external goods and services as discussed above.

Taking each of the four reasons in turn:

(a) The first reason.

This paper shows that the “balance on the external current account” (CA) is

primarily a capital account item even though it forms part of the National

income and outlay account of the SNA. CA includes the balance on external goods

and services, net compensation of employees from the rest of the world, net

investment income from the rest of the world and net current transfers from the

rest of the world [4]. If the current account balance CA is included as national

income on the income side of the national income and outlay account, the same

sum must be recorded as “non-productive investment abroad in capital goods” in

the “Use of income” side of the account because CA is not Saving in the

orthodox sense of equation (1). The corresponding entries

required on each side of the national income and outlay account are positive

for creditor countries and negative for debtor countries. This conclusion is

analysed in Section 4.

In a creditor country with a current

account surplus, consumption goods are consumed offshore and there may also be

interest income and profits remitted to the creditor country from its debtor

countries. The resulting incomes are spent by the productive sector of the

creditor economy to purchase capital goods offshore to satisfy the foreign

exchange mechanism. This leaves less of the gross operating surplus shown on

the gross domestic product and expenditure account of the creditor country for

new gross fixed capital formation as already described above, effectively reducing total incomes there.

In a debtor country with a current

account deficit, the surplus imported consumption goods are consumed through the creation of new domestic debt. Interest

payments and other remittances made by the debtor country through its current

account are also funded through the creation of new domestic debt. The deposits

arising from that debt are used to pay for the surplus consumption, interest

and other remittances. The payments are then returned to the debtor

country in exchange for capital goods or claims on capital goods that can

include commercial paper such as loans to banks in the debtor country.

Those return “capital flows” satisfy the foreign exchange mechanism set out in

Section 4 of this paper. The domestic debt of the debtor country increases

[5]. There is a corresponding increase in its domestic deposits. This

increase excludes foreign exchange loans to debtor country banks that do not

appear as M3 deposits in debtor country bank accounts [6]. If the net

consumption, interest and profit paid by the debtor country to its foreign

creditors is deemed to be negative national income in its national income and

outlay account, there must be a corresponding entry on the “use of income” side

of the account to reflect the loss of the debtor country’s capital goods. All

that has happened is that the debtor country economy has exchanged some of its

existing capital goods for consumption goods and to cover other remittances it

makes to fulfil its foreign currency debts. These exchanges take place outside of its productive economy.

[4] For example

: As set out in Table 1.4 of the New Zealand National Accounts published

by the NZ Department of Statistics.

[5] As is evident from

the reconciliation of monetary and credit aggregates, for example, Reserve Bank

of New Zealand Table C3 “Monetary and credit aggregates (NZ$ million)”.

[6] Refer, for example

to New Zealand Reserve bank Table C3 “Money and credit aggregates (NZ$

million).

(b) The second reason. The change in the

valuation of inventory in the gross domestic product (GDP) and expenditure

account of the National Accounts is discussed in Section 6. Inventory (other

than “stable” inventory needed to maintain reasonable continuity of supply to

consumers taking into account population growth and inflation) has little

residual value. This is because it must either be discounted at a cost to

future sales or it must lead to a reduction in future production. Either

production levels are maintained and goods and services are sold at a lower

price, or the price is maintained and the quantity consumed is lower, as

predicted from the Fisher Equation of exchange [7]. In most circumstances a

growing inventory represents a future “cost” rather than an “investment”, which

is one reason inventories are kept to a minimum in modern industrial

management.

Much of the change in

inventory “value” now registered in the SNA accounts is being “double counted”

in the GDP. This is because the corresponding incomes that would have been

needed to buy the inventory have either been siphoned off into

non-productive “saving” (referred to below) or they have been used to subsidise

other consumption prices. Non-productive “saving” and subsidies for consumption

prices use up the incomes that would have purchased the spare inventory.

When that is properly taken into account, current production [8] has not

been discounted enough to clear the market. As a first approximation, the value

of the change in inventory has been set at zero for the purposes of this

paper. That reduces the residual “Gross operating surplus” in the Gross

domestic product and expenditure account [9], and, therefore the National

Disposable Income (DI) [10] by the same amount.

(c) The third reason. To align with basic

theoretical principles of saving and investment, “Consumption of fixed capital”

in the national income and outlay account [11] must be replaced by the cash

flow figure “repayments of principal”. The cash flow figure represents the

outstanding loan debt on existing capital goods that is retired during the

period to which the account refers.

(d) The fourth reason. The

“Balance of external goods and services” is part of the current account

balance. Section 4 shows that the surplus consumption goods making up the

balance on external goods and services are “swapped” for capital goods. When

the current account items are placed together on the “income” side of the

National income and outlay account an equal and opposite entry “non-productive

investment abroad in capital goods” must be placed on the “use of income”

side of the National income and outlay account. In that case, a new entry “less the balance on

external goods and services” is required on the income side below the existing

entry “gross operating surplus”.

Inclusion

of the “Balance of external goods and services” in the SNA calculation of GDP

means that the economic growth figures provided in official statistics are

invalid. This is because they reflect

a change of foreign ownership abroad rather than a change in the domestic

economy. They are unsuitable as a basis for deciding domestic

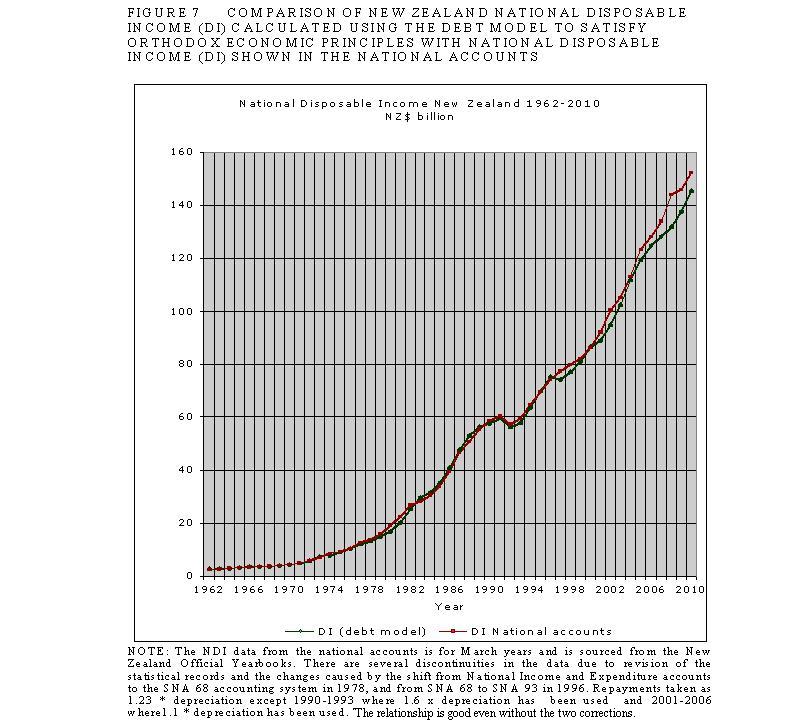

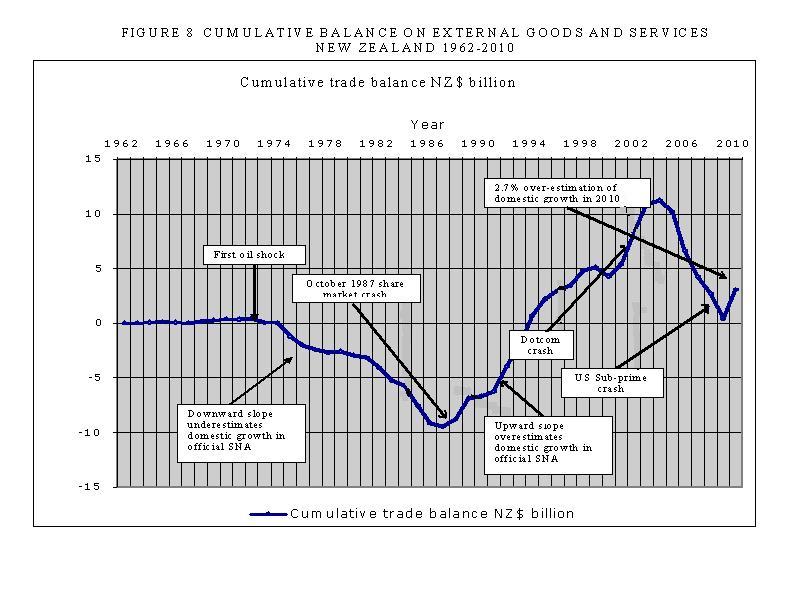

economic policy. Figure 7 suggests that domestic growth in

The changes

proposed in this paper bring the “use of income” and “income” sides of the

National income and outlay account [12] into alignment as

discussed in Section 8 of the paper. In summary it becomes:

Use of income :

= Final consumption C.

+ Purchase abroad of non-productive capital

investment goods (=CA).

+ Saving for productive investment S.

(18)

Income :

= GDP

+ Current account balance (CA).

less the balance on

external goods and services.

less repayments of

principal on outstanding productive investment.

(19)

Figure 7 provides a comparison

of the National Disposable Income (DI) corrected as proposed above and the DI

as shown in the existing national accounts for

The SNA National capital

account [14] needs to be restructured too. The capital assets bought by a

creditor country to settle its current account imbalance are added to its

“capital accumulation”. They are funded by new debt in the debtor country. The

“finance of capital accumulation” in the SNA capital account [15] becomes almost meaningless. Domestic

growth is swapped for foreign assets.

[12] Ibid Table 1.2.

[13] Figure 7 is indicative

and subject to recalibration. It is presently based on principal repayments

being 1.23 x the depreciation figures given in the existing National accounts

except for 1990-1993 when 1.6 x depreciation has been assumed and from 2001 to

2006 when 1.1 x depreciation has been assumed. Figure 8 hints that the model DI

curve should be above the official DI curve, but it is not.

[14] See for example

Table 1.3 of the New Zealand National Accounts published by Statistics New

Zealand.

[15] Ibid Table 1.3.

Assets purchased by a creditor

country from a debtor country are already “fully paid” by the creation of new

debt in the debtor country. If double entry bookkeeping is retained in the

capital account, the entry on the capital accumulation side would need to be

“Purchase abroad of non-productive capital investment goods” and the entry on

the finance of capital accumulation side would be an equal sum labelled

“Sale of surplus consumption goods and receipts of interest, profits and other

current transfers on the current account”.

Conceptually, therefore,

there is no such thing as foreign debt. There is only foreign ownership.

A debtor country with an accumulated current account

deficit is “owned” by foreigners in the proportion the total deficit bears to

the debtor country’s productive asset base [16].

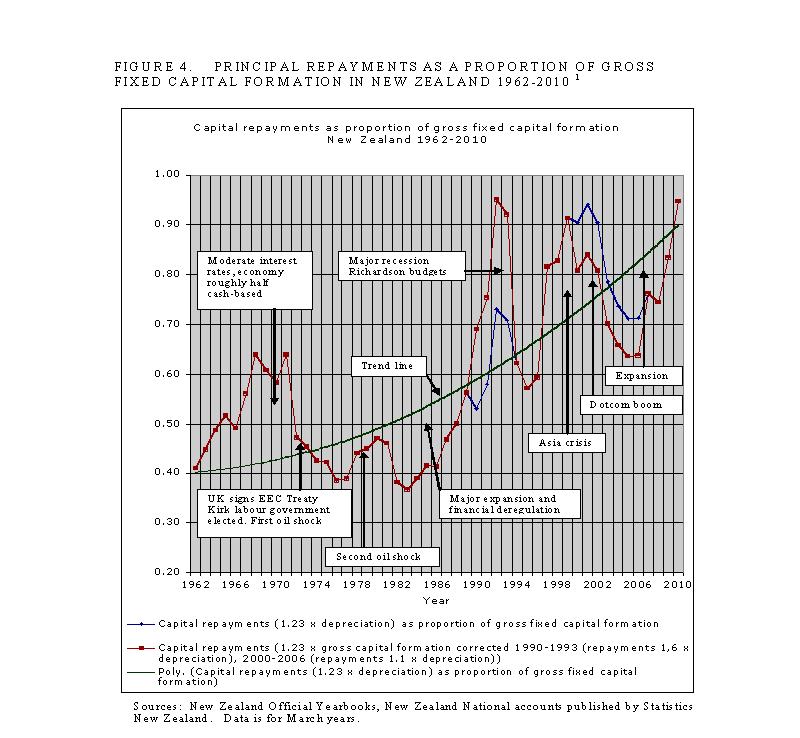

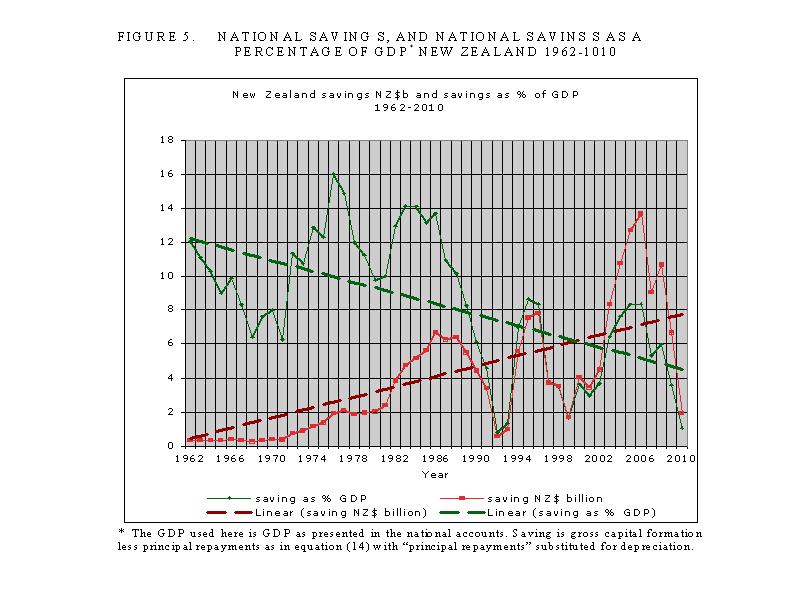

Saving trends are discussed in

Section 5 and the key findings are presented in Figures 4 and 5. Figure 4 plots

principal repayments as a proportion of gross capital formation (GCF) in

Section

5 shows that the decline in Saving for productive investment in

A primary cause of the decline

in Saving for productive investment is the rise of average depreciation rates

over time. This is shown in Figure 4. According to the second order polynomial

trend line of Figure 4, capital repayments have increased in

The

dire conclusion from this paper is that Saving for productive investment and

real GDP growth as measured using the international System of National Accounts

cannot be restored to modern developed economies unless the protocols around

depreciation are altered, bank lending polices and regulations reviewed and the

serious distortions in the SNA records themselves are corrected.

The final major issue of this

paper, discussed in Section 7, relates to the nature of “saving” that

does not qualify as Saving S for productive investment. Examples of this kind

of “saving” in

The productive economy is

self-cancelling. GDP is produced using only a small amount of debt. The debt used for

production is estimated to be less than 5.5 % of GDP in

[16] A wealth base

could also be used depending on what ownership comparison is being made.

[17] For example Table

1.2 of the New Zealand National Accounts published by Statistics New Zealand.

[18] Details of these

funds including their annual reports are readily available by searching “NZ

[name of fund]” on the internet.

[19] See paper “The DNA of the debt-based

economy.” The debt issued to generate the GDP has increased as a proportion

of GDP over time as the cash-based economy has been replaced with a debt-based

economy.

[20] See also Kerin, 2009.

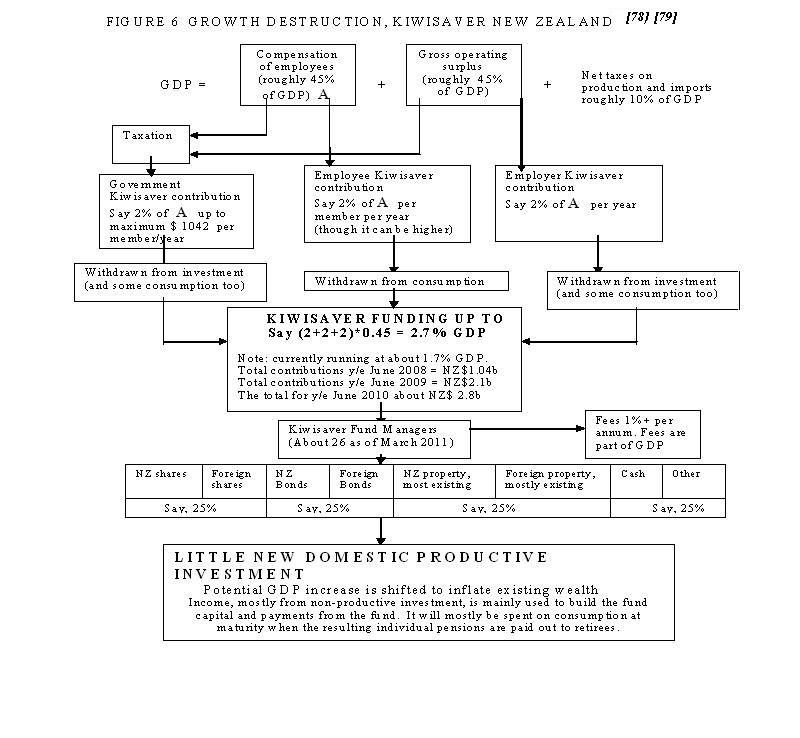

“Savings” programmes

like the “Cullen” Fund and the Kiwisaver scheme in

(a) Deposits in the form of unearned income paid as interest on

banking system deposits (Ms in the debt model referenced

in this paper)

(b) Deposits arising from the sale of domestic assets to foreigners (Dca in the debt model referenced

in this paper)

(c) Increased consumer debt where consumers are

enticed to maintain demand by borrowing beyond their incomes such as by the

systematic transfer of productive incomes into speculative non-productive

“investment” in the so-called “investment” sector or paper economy [21] (Db in the debt model referenced in this paper)

The manifestations of such “saving”

are wage stagnation, higher unemployment and recession, and increasing

inventories caused by lack of consumer demand.

The “investment” sector relies

for financial returns on unearned income and asset

inflation. Non-productive “savings” are the diametric opposite of the

needs of a healthy productive economy. They are parasitic. Since they cause a

transfer of funds from the productive economy to the speculative paper economy

they should really be included as negative items in the national income and

outlay account [23].

The

combination of the structural decline in real productive investment, harmful

“saving” and systemic error in the SNA itself is lethal to productive economic

activity in industrialised countries. It shows the extent to which the savings

myth has destroyed monetised human economic potential worldwide.

[21]

See previous papers by the author for further information: Financial system mechanics explained

for the first time “The Ripple Starts Here” and The interest-bearing debt system and its

economic impacts.

[23] Section 8 of this paper does not yet go so far, but it does propose to

include relevant capital items in the national capital account.

02.

BACKGROUND.

The theoretical work on which this paper is based can be

found at http://www.integrateddevelopment.org

There are now seven papers and ten documents altogether :

00. General summary of all papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of 95 principles of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

Papers 2, 5 and 7 are

especially relevant to this paper. Click on the links to access them. All

the work is covered by Creative Commons Attribution Non-commercial Share-alike

3.0 licence. This means it is free for access, download and use on a reciprocal

basis. The debt model used in this work is developed at “The interest-bearing debt system and its economic impacts”. That paper expands the Fisher equation of

exchange to allow for the effects of using interest-bearing debt in the world’s

financial systems.

Inflation in the debt model is

systemic and is directly related to deposit interest rates. The present model

calibration shows the inflation rate in

New Zealand is half the average deposit interest rate before adding the

recent one-off 2.5% GST increase (which is tax, not inflation, even though it

appears in prices) and provided wages and incomes are increasing with inflation

and capital inflows are not used for consumption. If interest rates rise, systemic inflation rises with them, but the

real effect on prices during recessions is masked by business discounts. Measured consumer price inflation falls when

interest rates are raised because the higher interest rates “kill” the economy,

not because they kill systemic inflation.

Paper 5 How to create stable financial

systems in four complementary steps includes a proposal to use

electronic cash or E-notes to achieve “quantitative easing”, enabling

real earned savings to accumulate. Issuing E-notes is exactly what governments

do when they purchase bonds from the banks except the bonds bear interest and

have to be repaid with new debt. As set out in the following sections of this

paper, the existing financial system based on interest-bearing debt does not

allow for aggregate non-productive saving

In the debt model, GDP arises

from the flow of the productive transaction deposits My used by the productive sector

to produce goods and services, multiplied by its speed of circulation Vy. The pool of transaction deposits My that funds the productive sector in the debt model

must grow if the GDP is to increase. Without the issue of new

debt or interest-free E-notes there can be no new GDP. Over the past

several decades New Zealand’s debt has been growing much faster than its GDP

because there is a structural transfer, in the form of unearned deposit

interest, of productive incomes to the unproductive “investment sector” or

paper economy. The same has been happening almost everywhere else in the

world. The debt model shows how that extra debt arises and how it fuels

the non-productive investment sector causing asset bubbles. The use of

interest-free E-notes on a wide scale instead of debt would allow interest

rates to be set at very low levels, stopping asset bubbles and bringing the

unproductive investment sector expansion into line with that of the productive

economy. Using E-notes is more efficient than using debt. Overall, far

LESS debt and fewer corresponding bank deposits would be needed using E-notes

than are needed now. This is because the pool of debt Ms supporting the

un-productive investment sector would grow much more slowly than it has grown

in the past.

In relation to “saving” in the

System of National Accounts (SNA), a primary ‘bible” for measuring asset prices

and depreciation is the OECD Manual 2009 “Measuring Capital”, 2nd

Edition”[24]. The general purpose of both the SNA and the Manual relates to

measuring wealth to

assist in the calculation of financial returns. That is likely to

be why the SNA uses “consumption of fixed capital” based on depreciation

schedules. No matter how refined those schedules are, they cannot

represent the monetary flows contemplated by the National income and outlay

account of the SNA. This causes an

inherent contradiction in the National Accounts [25]. Lack of

understanding of the nature of saving in a debt-based financial system is

widespread throughout economic literature[26]. This is a core issue of

this paper and especially its Section 4. Figure 5 shows how catastrophic the

unjustifiable use of depreciation in the SNA has been in slowing economic

growth.

A main source for measurement

of the Balance of Payments and International Investment Position is the

“Balance of Payments Manual” Edition 6 (BPM6) published by the International

Monetary Fund (IMF) in 2009 [27].

In

In practice, according to the

debt model, deposits that migrate outside the productive economy must, in

aggregate, be funded either from new bank debt or a decrease in consumption

demand. Otherwise the purchase of new productive capital goods cannot be

completed within the productive sector as the debt model requires [28].

[24]

Especially Ch 5 “Depreciation or Consumption of Fixed Capital”.

[25] This becomes apparent as early as page 10 of SNA 2006, United Nations,

2008 where par. 1.63 says: “The accounting rules

and procedures used in the SNA are based on those long used in business

accounting” while in the very next paragraphs it says that where there is a conflict

between business accounting and economic theory, economic theory will take

precedence. However, in practice, the National Accounts do NOT give

precedence to economic theory, otherwise they would not be faulty as this paper

demonstrates.

[26] Ideological

“capture” of economic debate at some major universities and financial

institutions may have contributed to this.

[27]

The New Zealand Statistics Department is still using the previous edition

(BPM5).

[28] See later

discussion especially Section 7.

03. THE SYSTEM OF NATIONAL ACCOUNTS.

Simon Kuznets worked widely on

economic measurement and received a Nobel prize for his efforts in 1971. He is

one of the fathers of the System of National Accounts (SNA) in use throughout

the world, especially the parts relating to national income[29].

The work of Kuznets and others

developed largely from the pioneering work of Irving Fisher [30] and was

extensively used during and after World War II to help direct economic

resources to where they would be most productive. The essence of the SNA is to

measure both the income side and the expenditure side of monetised economic

activity and compare the two.

Basic economics texts give

remarkably little space to saving. Baumol and Blinder [31] for example devote

only a couple of pages to it. At the most basic level they define Saving S

as the difference between disposable income (DI) [32] and consumption

expenditure C [33]. In the SNA, saving is a residual number obtained by

measuring disposable income DI and consumption C, though DI itself also

contains another residual

called the gross operating surplus which is used to balance the income side of

GDP.

S = DI – C

(1)

This is confirmed by the section

on “use of national disposable income” that forms part of the national accounts

of most of the worlds’ nations [34]. Baumol and Blinder write:

“The economy will reach an equilibrium at full employment only if the

amount that consumers wish to save out of full-employment incomes is precisely

equal to the amount that investors want to invest”[35].

According to Baumol and

Blinder Savings S=Investment I “always” (Italic in text p181)

[36]. Most “modern” basic economics texts including Baumol and Blinder

provide circular flow diagrams of the economy that stress this interpretation.

[29] Among his major works: National

Income and Capital Formation, 1919–1935.

[30]

Fisher’s well-known equation of exchange is revised in Manning op cit. to take

into account the modern debt-based financial system.

[31]

For example, “Economics Principles and Policy”, William J. Baumol and Alan S.

Blinder, 4th Edition Harcourt Brace Jovanovich, 1988.

[32] (National) Disposable Income (N) DI is not the same as Gross Domestic

Product (GDP). The two are linked in the System of National Accounts (SNA) by

the relationship: (N) DI = GDP+ net property and entrepreneurial income from

the rest of the world -consumption of fixed capital (depreciation) + net

current transfers from the rest of the world.

[33] Baumol & Blinder op cit p 155.

[34]

For example Statistics

[35] Baumol & Blinder op cit p 177.

[36]

The statements fail to consider the mechanics of the financial system such as

credit creation and retirement, growth, debt servicing and unearned income and

associated speculative investment: and they simply assume equilibrium theory.

Baumol and Blinder are also explicit about the

definition of investment:

“As defined

in the national income accounts, investment includes only newly produced

capital goods, such as machinery, factories, and new homes. It does not include

exchanges of existing assets.” (emphasis in text). [37]

Those newly produced capital

goods are produced and sold in the marketplace just like goods and services for

consumption (As set out in Figures 1 to

3 and Section 7, and in the paper “The DNA of the debt-based

economy.”

For Saving to equal

(productive) Investment in the SNA, it must, according to orthodox economic

theory, arise from production incomes when there is “full-employment” in the

economy. The theory provides little guidance on what happens in the

absence of “equilibrium” or “full-employment”.

The SNA National Income and

Outlay account also includes “investment income from the rest of the world,

net” and “current transfers from the rest of the world, net” [38] that

together make up the Current Account surplus CA if they are positive and

Current Account deficit if they are negative.

The derivation of the Savings function from Table 1.1

and Table

Saving S (net) =

Current account surplus (CA)

+ Gross capital formation

(including increase in stocks) [39].

- Consumption of fixed

capital (depreciation).

+ Statistical discrepancy

[40]

(13)

The SNA Saving S formulated that way fails to satisfy

the orthodox economic conditions for saving in at least four respects [41].

[37] Baumol & Blinder op. cit. p. 159.

[38] NZ

National Accounts Table 1.2.

[39]

Gross capital formation is the same as Investment. Increase in stocks is also

usually treated as investment.

[40] Required

because of errors in the GDP production and expenditure estimates even though

the operating surplus is itself already a residual.

[41] In

the SNA itself, at United Nations, 2008, par. 9.28, p.183 saving is defined a

little more loosely: “Saving

represents that part of disposable income (adjusted for the change in pension

entitlements) that is not spent on final consumption goods and services.” However,

the economic compliance failures discussed in this paper still apply.

First, current account surpluses

are not, for the most part, formed of saving as defined by orthodox theory.

This is despite their being represented by new debt in the debtor country and

by an equivalent amount of foreign assets in the creditor country. For details

on the current account process see section 4 of this paper. In practice,

current account surpluses in creditor countries result in non-productive

“saving” outside of the domestic economy. The “saving” is funded by new debt in

the foreign debtor economies. The new debt in the debtor countries is created

outside of their domestic productive economies.

Secondly, depreciation is not

a cash flow and so cannot relate to income and outlay. For details see section 5

of this paper on capital flows and the purchase of capital goods. United

Nations (2008) at par. 6.240 on p. 123 makes clear that “consumption of fixed

capital” in the SNA is meant to reflect the residual economic value of an

asset, as distinct from its accounting depreciation. It is unclear how the

residual economic value of an asset can be calculated unless actual repayments

are taken into account [41] [42]. Whatever “consumption” allowance is

made, it still does not represent a financial flow as the SNA itself insists is

necessary. The national income and outlay account is, by definition, about

income and expenditure, not about wealth.

Thirdly, while increases in stock are produced, they

are neither investment nor saving because they have little net residual value.

For details see section 6 of this paper on changes in inventories (stocks)

[44].

[42] Refer United nations, 2008, par. 248-251 for further clarification.

[43] United Nations, 2008 (SNA) at par. 10.25 p.198 defines “consumption of capital: Consumption of fixed capital is the decline, during

the course of the accounting period, in the current value of the stock of fixed

assets owned and used by a producer as a result of physical deterioration,

normal obsolescence or normal accidental damage”. This

is itself evidently a wealth related definition rather than a dynamic income

flow.

[44] This applies

notwithstanding the valuation of stocks in the SNA, United Nations, 2008 par.

124-125, p.208

Fourthly and above all, Saving S is defined in Table

1.2 of the National Income and Outlay account to be Disposable Income less

Consumption (equation 1) as orthodox theory requires. However, in its present

form the National income and outlay account as a whole prevents Saving S from

conforming to the definition required by orthodox theory.

The existing sequence and

format of the tables making up the national accounts under the System of

National Accounts can be readily accessed at Annex 2 (from page 561 onward) of

the SNA protocol:

http://unstats.un.org/unsd/nationalaccount/docs/SNA2008.pdf

.

04. THE CURRENT

ACCOUNT PROCESS.

While the current account (CA)

can be interpreted as a form of “saving” for the creditor country, it does not automatically follow

that a CA deficit can be considered a “negative saving” in the debtor

country. “Negative saving” is extremely difficult to visualise. Borrowing

to settle the foreign exchange transactions on the current account deficit is, by

definition, “dis-saving” because it results in the sale of domestic productive

assets to foreigners except to the

extent domestic deposits arising from the sale of those productive assets are

reinvested in new productive assets.

Some of those deposits could

potentially qualify as productive SNA investment but most do not. That is

not quite the same as in equation 13. The SNA appears to be mixing productive

sector transactions with non-productive investment sector ones; thereby

confusing income with wealth.

Foreign ownership

of the assets of debtor countries is not always made public there. Its

consequences are not widely advertised and its serious economic impact is

poorly understood in the wider community.

New deposits from the creation

of extra debt in the debtor country are not strictly Saving in the creditor

country because they do not increase productive investment there. In the

absence of the exchange (the swaps), the creditor country would face a quantum

of inflation in its productive sector equal to its current account surplus.

The current account process is

shown in Figure 1. Arguably, neither the debtor country nor the creditor

country gains from current account imbalances. The creditor country spends its

deposits from the sale of its surplus production and other remittances earned

abroad to buy an equal “value” of assets from the debtor country. That

increases the creditor country’s nominal wealth but does little for its

domestic economy. If it did not purchase assets abroad there would be too

much income left in circulation in the creditor country for the purchase of the

goods and services left over there after exporting its production surplus. That

would be inflationary, and seems to be one origin of the widespread

misapprehension that creditor countries “export” inflation [45]. To avoid

that, the surplus income must be re-invested abroad. That re-investment affects

the creditor country’s capital account rather than Saving on its national

income-outlay account. In

practice exporting countries merely maintain their purchasing power status quo

by means of the foreign exchange transactions. Those transactions do, however,

alter the balance of consumption and

investment within the domestic economies of exporting countries.

[45]

Systemic inflation does occur indirectly in the debtor country from the

increase in deposits there. This is discussed below.

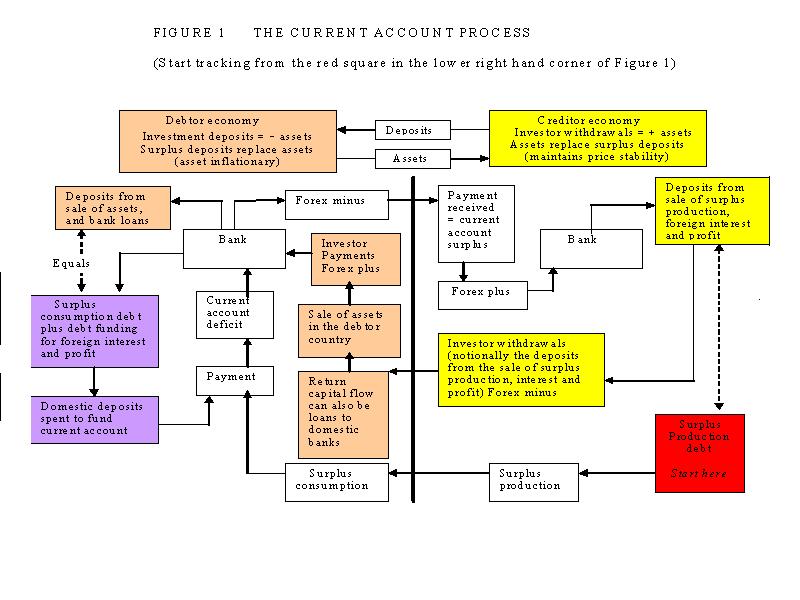

Click here to see : FIGURE 1 : THE CURRENT

ACCOUNT PROCESS. (Start tracking from the red square in the

lower right hand corner of Figure 1.)

{kind=link}

Creditor country “investor

withdrawals” shown on the lower right hand side of Figure 1 are surplus

domestic deposits in the creditor country arising from the production debt used

to produce the current account surplus. To avoid inflation in the creditor

country those deposits are switched from domestic consumption there to foreign

“investment”, through bank intermediation.

Much, if not most, foreign

“investment” fails to qualify as productive investment as defined under the

SNA. The creditor country produces those surplus goods and services. Both the

production debt used to produce them and the corresponding incomes in the form

of compensation of employees and gross operating surplus foreseen in the SNA

exist in the domestic economy of the creditor country. The surplus goods and

services are therefore part of the gross domestic product of the creditor

country. GDP has been defined as:

“The total market value of goods and services produced in [a country]

after deducting the cost of goods and services utilised in the process of

production, but before deducting allowances for the consumption of fixed

capital.” [46]

[46]

As shown below, a negative

“balance on external goods and services” is funded by new domestic consumer

debt in the importing debtor country. A positive balance on external goods and

services is, in principle, exchanged for capital goods imported from debtor

countries through the current account.

At the point of production,

all incomes, whoever owns them, are deemed to be in domestic accounts. The

creditor country swaps its spare production for (mostly existing) foreign

capital goods produced elsewhere while the debtor country creates the same

amount of new debt to buy the spare production imported from the creditor

country.

That

new debt forms part of the debtor country’s current account because there are

no “spare” deposits created in the debtor country during the production phase

of the imported goods.

Interest and profit remitted

abroad as a result of foreign ownership of domestic production form part of

domestic incomes in the debtor economy. When the remittances covering interest

and profit are sent offshore they form part of the current account expenditure.

Domestic deposits in the remitting country are reduced by the same

amount.

In a debt-based economy, it is

not possible to both consume domestic production and pay for the remittances to

foreign countries covering interest and profit because that would mean spending

the same deposit twice. The cost of remittances for interest and profit payable

abroad must therefore also be borrowed within the domestic economy of the

debtor country to enable the value of goods and services in the debtor country,

represented by the remittances, to be consumed. That adds to consumer debt

in the debtor country.

The

total new deposits in the debtor country, in principle, therefore, include all

of its accumulated current account deficits.

The debtor country sells some

of its capital goods to get back the corresponding deposits from abroad that it

used to pay for the surplus imports, the remittances and the remainder of its

current account deficit. That sale balances its foreign exchange position and

leaves it with additional domestic deposits equal to the added consumer debt.

Those deposits from the sale of capital goods do not return to those who

borrowed the debt to pay for the surplus goods and services and remittances

sent offshore. They finish up, instead, in the hands of those in the

debtor country who have sold assets (or an indirect claim on those assets) to

the creditor country to settle the current account deficit. This means the

debtor country’s capital account must be reduced accordingly.

In Figure 1, the debtor

country finishes up with the new debt that created the deposits used to buy the

surplus foreign production it imports and to fund its other remittances

offshore, enabling it to balance its foreign exchange position. The creditor

country receives those deposits. They are then returned to the debtor country

when the debtor country sells domestic assets (or bonds or commercial paper) to

its foreign creditors. The repatriation of deposits from the creditor country

is shown as “investor withdrawals” at the lower right hand side of Figure

1. For the foreign exchange position of the debtor and creditor countries

to balance, the sale of debtor country assets (or bonds or commercial paper) MUST take place. The market price

paid by the creditor country for the assets in terms of its own currency is

determined by the currency exchange rate between the two countries.

The debtor country deposits

arising from those asset sales are not inflationary as long as they are used

for new productive investment within the strict terms of the SNA. If any of

them were to be used for consumption there would be some consumer price (CPI)

inflation in the debtor country. Deposits used to buy existing assets in the

debtor country would cause inflation (such as in property prices) in the

unproductive investment sector. Many of the deposits arising from the sale of

capital goods by a debtor country to balance its current account are used that

way, contributing to the asset inflation commonly observed there. In any case,

according to the debt model, the extra deposits in the debtor country cause

additional systemic inflation through the on-going payment of deposit interest

on the extra deposits. In that indirect sense, current account deficits are always inflationary in the debtor country.

The amount of inflation depends on the interest rate paid on deposits in the

debtor country and the tax rate on interest income there.

This discussion suggests the current accounts of the world’s

nations should always be balanced and there should be mechanisms in place to

ensure a balance is maintained.

John Maynard Keynes argued for

balanced trade at the Bretton Woods conference in 1944, but lost out under

In

The use of the term “saving”

to describe a current account surplus is therefore misleading [48]. In Figure 1

the creditor country has surplus deposits. It uses the deposits to buy foreign

assets not because it has saved but because it has sold surplus production

offshore. It is a trading dynamic, not a conscious decision to forgo or defer

consumption. It is often more a function of overproduction than

under-consumption. The assets it buys mostly represent existing wealth

like equities, businesses, property, and related loans, rather than new

investment in bonds and business expansion in the debtor country that would be

defined as productive investment in the SNA. It is not “saving” as defined

in orthodox economic theory because the purchased assets do not relate to new

domestic production in the creditor country and do not alter its gross domestic

product.

From the debtor country’s

point of view, deposits arising from foreign capital inflows on the current

account “invested” in funds that are not committed to productive investment or

that are held in the form of loans to domestic banks do not qualify as

investments in the debtor country national accounts. They do so only when they

are committed to new productive capacity in the debtor country. Instead, most

inflows that appear as domestic deposits in the debtor country typically

qualify as “investment” in the unproductive investment sector that serves to

inflate the value of existing assets or “wealth” there. Such “investment”

neither adds to nor reduces production capacity. It does not qualify as

investment under the SNA and is therefore not “saving” as defined in orthodox

economic theory. Moreover, any deposits from the capital inflows used to retire

existing debt in the debtor country reduce debt and deposits by the same

amount. They do not affect the domestic economy of the debtor country other

than to reduce its rate of systemic inflation a little [49].

Treating a current account

surplus or deficit as wholly positive or negative in the saving equation (13)

in the National income and outlay account therefore cannot be correct because

the “investment” arises from consumer debt as shown in Figure 1 [50].

The SNA National income and

outlay account [51] does contain the gross operating

surplus and “consumption of fixed capital”, so it does make allowance within the account for investment

qualifying as productive investment under the SNA. However this investment is not the residual referred to as “Saving” in the national income and outlay account.

In the debt model, new capital goods are produced and then “consumed” in the sense

of being purchased as is discussed fully in Section 5 of this paper. All new

capital goods are bought from total incomes given on the income side of the

national income and outlay account. Repayment of existing debt comes out of the

income (the gross operating surplus in the national accounts) generated from

existing and new capital investment. The more repayments there are, the

less net income there will be left over to pay for new capital goods. Net

expenditure on new productive investment in the national accounts should, from

equation (1), therefore be:

Saving S = Productive investment = DI-C = gross

fixed capital formation less principal

repayments. (14)

[47] Reserve Bank of New Zealand Table C3 (current).

[48] The SNA amplifies this at United Nations, 2008, Ch. 26 “The rest of the

world accounts and links to the balance of payments, BOPM6”.

It says at p. 683, “In the SNA,

transactions between a resident unit and the current external balance thus show

how far residents call on saving by non-residents.”

[49] This is true even if the debt retired forms part of the productive

transaction deposits My in the debt model. In that case, other players in the productive economy

would have “spare” income leading either to inflation or to additional non-SNA

qualifying “savings” as discussed in Section 5.

[50] It could perhaps be labelled “surplus consumption debt plus debt

funding for foreign interest and profit”.

[51] Shown as Table

Equation (14) reflects the

fundamental orthodox economic premise stated at page 11 of this paper that

Saving = (productive) Investment. Productive Saving is a net figure that

recognises that some of the incomes nominally available for investment are used

to retire existing investment debt. Only the net income left over after

debt retirement is still available to buy new capital assets as discussed fully

in section 5 of this paper.

The

SNA national accounts are not presented in the format shown in equation (14).

In fact, there is no such

thing as the “residual” “saving” figure that is presently shown in the national

income and outlay account of the national accounts. Saving S = (Productive) Investment is

indirectly built into the income side of the national income and outlay account

(as presently presented in the national accounts) as “gross fixed capital

formation” (Investment) less “consumption of fixed capital” (depreciation) but,

as discussed in section 5 below, that is neither accurate nor sufficient.

In a creditor country the

production surplus is sold through its current account but it does not qualify

as investment in Equation (14). The purchase of foreign assets by a creditor

country is an exchange of spare domestic consumption capacity in the creditor

country for other (capital) goods from the debtor country. That is

fundamentally no different than if the spare production were consumed

domestically. The total income and

expenditure remain the same. The only difference is that the capital

account balances of the creditor and debtor countries change.

The purchase of offshore

assets including loans to offshore banks is, from the point of view of the

creditor country, income earning and “productive” at the price paid for them,

otherwise the exchange would not take place. That “income” is not strictly

national income for the creditor country because it cannot be remitted

there. It forms part of the creditor country’s current account surplus

that is, in turn, swapped for more foreign assets, and so on as long as the

current account surplus continues.

The key conceptual element

is the “swap” that takes place within the domestic economies of the debtor and

creditor countries.

In a debt based financial

system, deposits to pay for surplus consumption and remittances in the debtor

country originate outside of that country’s production cycle. The only “income”

generated is that resulting from the subsequent sale of capital goods in the

debtor economy to its foreign creditors, but that must be treated as a economic

loss rather than income from production.

Taking the current account

balance in creditor countries and debtor countries in turn the sequence of the

exchange that takes place is :

Any gross fixed capital

formation from return capital flows invested by a creditor country as foreign

direct investment in new capital goods in the debtor country is automatically

included in the GDP of the debtor country [52]. The increase in the total

capital value in the creditor country contributed by the capital goods it

receives in payment of the debtor country’s CA deficit should be recorded in

its capital account as well, if it is to be treated as income, as in its

National income and outlay account.

In a debtor country, gross fixed capital

formation arising from any return capital flows invested by the creditor

country in new capital goods in the debtor country is automatically included in

the GDP of the debtor country [53]. The decrease in the total capital

value of capital goods in the debtor country resulting from its sale of capital

goods to the creditor country in payment of the debtor country’s CA deficit

should be recorded in its capital account as well as, if it is to be treated as

negative income, in its National income and outlay account.

These sequences comply with

the traditional orthodox economic theory represented by the amended savings

equation (15) below. When a country’s current account is in balance or when the

current account balance is omitted from the national income and outlay account

as proposed above, equation (14) becomes:

Saving S (net)(Investment)

= Current account surplus (CA)

+ Gross capital formation (including increase in stocks) [54]

- Consumption of fixed capital (depreciation)

+ Statistical discrepancy

[55]

(15)

[52] It is assumed that, since the debt that gives rise to the sale of

capital goods in the debtor country already exists, the deposits created from

that debt also exist at any point in time. Any productive investment arising

from those deposits returned to the debtor country in payment for its capital

assets is therefore automatically included in the debtor country’s

domestic gross fixed capital formation.

[53] It is assumed that, since the debt that gives rise to the sale of

capital goods in the debtor country already exists, the deposits created from

that debt also exist at any point in time. Any productive investment arising

from those deposits returned to the debtor country in payment for its capital

assets is therefore automatically included in the debtor country’s domestic

gross fixed capital formation.

[54] Gross capital formation is another term for (gross productive)

Investment. Increase in stocks is also usually treated as investment by

convention.

[55] Required because of errors in the GDP production and expenditure

estimates even though the operating surplus is itself already a residual.

In equation (15) investment is

still incorrectly defined

as Gross capital formation (including increase in stocks) less Consumption of

fixed capital (depreciation).

Equation (15) would only

represent Savings = Investment according to the orthodox economic theory if

consumption of fixed capital (depreciation) were a cash flow and the increase

in stocks represented productive investment. It is not and they do not.

Equation (15) as it stands

still does not represent orthodox economic theory.

The mechanical processes relating to capital flows,

the purchase of capital goods, and changes in inventories (stocks) are

discussed further in Sections 5 and 6 of this paper.

The amended National Disposable Income (DI) for New

Zealand 1962-2010 is shown in Figure 7 of this paper. Figure 7 incorporates the

following changes to the existing SNA format :

(a) deletion (or reduction) of the change in

inventory from the gross product and expenditure account and corresponding

correction of the gross operating surplus.

(b) substituting the corrected gross operating

surplus after subtracting the “balance on external goods and

services”.

(c) replacing residual ‘saving” with Saving as

in equation (15) but with

principal repayments substituted for depreciation.

(d) deleting the current account surplus,

including the “balance on external goods and services”.

Contrary to the methods of calculation in use until

now, the proposed changes provide rational results for

05. CAPITAL FLOWS AND THE PURCHASE OF CAPITAL

GOODS.

The production of goods and

services giving rise to new capital goods is included in the productive

transaction deposits as My that when multiplied by their

speed of circulation Vy give rise to the Gross Domestic Product (GDP).

[56] Those new capital goods must be sold to clear the market. Since the

income earners in the productive sector who want to buy the capital goods are

not usually the same as those who produce the capital goods, they are exchanged

through bank intermediation. The buyers of the capital goods borrow part of the

production incomes of employees (employee incomes) and businesses (gross

operating surplus) as shown in the upper part of Figure 2. That enables the

original producer loans to be retired, thereby clearing the market as the debt

model requires.

[56] See The interest-bearing debt system and

its economic impacts for details of the debt

model.

In aggregate, some employees and

businesses have swapped their share of the sale price of the capital goods that

they do not want to consume with others in the productive sector (the

investors shown at the lower left of Figure 2), who do want to consume

them. This creates lending within

the productive sector.

Click here to view : FIGURE 2. DYNAMIC DEBT MODEL FUNDING THE PRODUCTION

AND PURCHASE OF NEW CAPITAL GOODS.

{kind=link}

In Figure 2 the bank loans

supporting the production transaction deposits conceptually retired in each

production cycle. (See The interest-bearing debt system and

its economic impacts). My is assumed for simplicity to include the whole value

of goods produced during the production cycle.

In

the hypothetical case when no capital goods are produced, the outside loop on

the left and bottom of Figure 2 would not be needed. The transaction deposits My would be used to produce goods and services for consumption, generating

incomes. The incomes would be banked and then used to pay for consumption. The

producers would then use the sale income to pay off their transaction deposits My. In practice the process is dynamic. There is always an outstanding pool

of transaction deposits My that is continually being recycled through

the production system.

When capital goods are also

produced as shown on the left and lower part of Figure 2, producers (employees

and businesses) initially collectively “own” the capital (investment) goods

they produce. Conceptually, they hold their share of the capital goods as

security for the bank loan (part of the debt giving rise to My ) used to produce them. The bank loan (part of the debt giving

rise to My) used to produce the capital goods has to be

repaid when they are sold just as is the case for consumption goods and

services.

The producers have an asset

equal to the sale value of the capital goods and an equal offsetting liability,

their debt (part of the debt giving rise to My) to the bank. The

debt model assumes for simplicity that, during the production phase of the

production cycle, producers draw down (pay themselves) all of their operating

surplus as income [57]. The production transaction deposits My represent the full sale value of all the goods and services, including capital goods,

produced during the production phase.

[57]

For simplicity, in the debt model, all income including all of the gross operating

surplus is included in My. Any error in this

assumption is small because My is small compared to GDP.

Once the consumption goods and

services have been consumed only the capital goods are left. The market sale value of those capital goods

that have not yet been “consumed” equals the remaining incomes that have not

yet been spent, as shown at the top left of Figure 2. The remaining

incomes are the Saving required by orthodox economics as discussed in section 4

of this paper. The capital goods for sale are the corresponding investment.

This gives Saving = (productive)

Investment as in equation (14).

Producers must sell the

capital goods they have produced to repay their bank debt (part of the debt

giving rise to My). When they do so, the buyers of the capital

goods take out a bank loan as shown on the left of Figure 2. The total of such

loans is the Saving shown at the top of Figure 2. The buyer of the capital good

(the investor) pays the producer the sale price and the producer then retires the

outstanding loan (part of the debt giving rise to My) used to produce

the capital good. Conceptually the investors (bottom left of Figure 2) have

borrowed just enough from the Saving pool (top of Figure 2) to clear the

outstanding production debt (part of the debt giving rise to My) used to produce the capital goods. That is exactly as defined in the

Baumol and Blinder quote on page 11 of this paper. The only way for the market

to clear without inflation or deflation is where the purchase price of the capital goods to be “saved” by one part of

the productive sector equals the sum on-loaned to investors who usually form

another part of the productive sector, exactly as orthodox theory

requires.

Capital

formation therefore conceptually takes place by new debt formation within the

productive sector itself. It is the

re-allocation of existing incomes in the productive sector.

This

is in full agreement with orthodox economic theory.

In aggregate, “Saving” in the

orthodox sense of Saving = (Productive) Investment as illustrated in Figure 2

occurs only to the extent some employees and businesses lend some of their

market incomes to other players in the same market who wish to buy the capital

goods that are available. If some of those market incomes (employee incomes and

gross operating surplus as shown at the top right of Figure 2) are withdrawn

from circulation in the form of non-productive “saving” for non-productive

“investment” as currently claimed in the SNA National Income and Outlay

accounts, or for debt retirement, either an equivalent amount of NEW bank debt MUST be introduced to make up the difference or economic activity

will be suppressed. There would not be enough income left to buy all the goods

and services, including capital goods, which have been produced. [See

Figure 3 investment I1 below and section 4 of this paper]. The only

exception to this would be where an equal existing non-productive “investment”

deposits were returned to the productive economy to be used for consumption. This

happens, for example, when pensions are paid out of pension funds.

In

practice, as shown in the more recent paper The DNA of the debt-based economy all of the net capital investment is initially represented by bank debt and the

accumulated outstanding principal on that debt equals the GDP. That is because

the residual existing incomes in the productive sector referred to above are

withdrawn from circulation to satisfy the requirements of the debt model (Ms + Dca + Db). They are a structural part of

the debt system and are not related to voluntary “saving”. That is why trying

to increase non-productive “saving” destroys economic activity unless that

”saving” is invested in new productive

capacity.

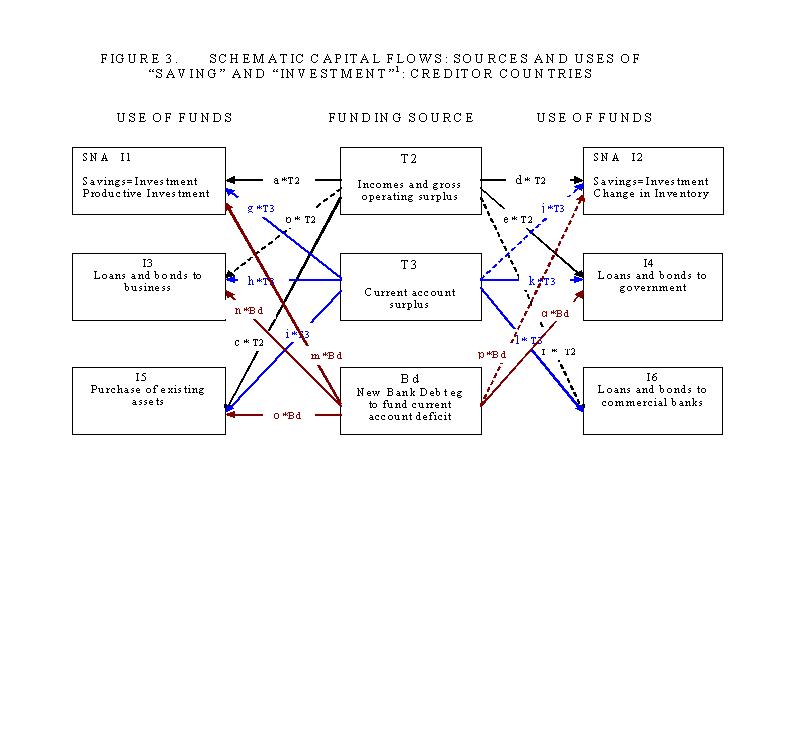

Figure 3 traces the broad

savings impact in a debt-based economy. It assumes the residual “saving”

presently shown in the income and outlay account of the national accounts

prepared under the SNA (called here Type 1 saving) is a myth.

Let Type 2 saving (the funding

available from income and operating surplus shown at the top of Figure 3) be

T2.

Let Type 3 “saving” (the

funding available from the current account surplus as presently shown in the

income and outlay account of the national accounts prepared under the SNA) be

T3. It is shown at the centre of Figure 3.

Let new debt funding from

domestic banks be Bd. This is shown at the bottom of Figure 3.

Further let the funding T2, T3

and Bd be distributed according to the following six uses:

I1 = productive

investment

I2 = change in

inventories

I3 = loans and bonds to

business

I4 = loans and bonds to

government

I5 = purchase of

existing assets

I6 = loans and bonds to

commercial banks

Let a, b, c, d, e, f be

the proportion of Type 2 funding applied to each use, g, h, i, j, k, l be the

proportion of Type 3 funding applied to each use and let m, n, o, p, q be the

proportion of new bank debt applied to each use.

The resulting schema shown in

Figure 3 applies to creditor countries and shows the sources and distribution

of funding. Its application to debtor countries is discussed above. Links

considered to be minor are shown dotted. Consumption is omitted.

Click here to view FIGURE 3. SCHEMATIC CAPITAL FLOWS: SOURCES AND USES

OF “SAVING” AND “INVESTMENT.”[58]: CREDITOR COUNTRIES.

{kind=link}

[58]

Figure 3 is drawn from the point of view of a creditor country.

There are many known quantities

in the matrix shown in Figure 3 and it should be possible to calculate each of

the proportions a, ………q. At this point the intent of Figure 3 is to show

how the current system of national accounts (SNA) and orthodox economics fail

to reflect the real dynamic economy. A more detailed analysis would

require a separate paper.

There are several obvious

relationships. For example:

a*T2 + g*T3+ m*Bd

= Productive investment I1, whether Gross fixed capital formation or net

fixed capital formation. (Net fixed capital formation = Gross fixed capital

formation – Principal repayments on existing capital goods).

For the market to clear just

current production of all goods and services, (g*T3 + m*Bd) must represent net

household, business and government non-productive “savings” including, in New

Zealand, Kiwisaver, the various superannuation funds like the Cullen

Superannuation Fund, and sinking funds like Accident Compensation Corporation

and the Government Earthquake Fund. Otherwise, as described above,

productive Saving could not equal Investment as shown in Figure 2.

That in turn suggests:

g*T3+m*Bd

= b*T2+c*T2+d*T2+e*T2+f*T2.

If that were not so, the

productive sector would either inflate or deflate because demand does not match

the goods and services available for consumption. The total of

b*T2+c*T2+d*T2+e*T2+f*T2 represents a withdrawal of purchasing power from

incomes leaving too little income to buy the available goods and services that

have been produced. The withdrawal must be replaced with new purchasing power

if the market is to clear. The only replacement funding to T2 (neglecting j* T3

and p* Bd) is g*T3 and m* Bd. That is what gives rise to the equality proposed

above.

The ratio f, the proportion of

T2 “savings” from incomes and operating surpluses “invested” in the form of

loans and bonds to commercial banks, is usually small. Net household, business

and government “savings” from incomes and operating surpluses pass largely into

non-productive investments. In the case of c*T2 they inflate the value of

existing assets and in the case of e*T2 they support government budget

deficits.

Figure 3 is drawn from the

point of view of a creditor country with a current account surplus. It shows

how the outward capital flow through the current account surplus T3 is spent,

that is, what the creditor country buys with the surplus. For some countries,

l*T3 (funds from the T3 current account surplus loaned to commercial banks in

the form of financial instruments such as bonds) has become an important part

of the T3 capital flow to debtor countries. It is part of the so-called “carry”

trade. It can be cheaper for banks to borrow foreign money and hold foreign

exchange liabilities than it is for them to pay deposit interest on domestic

deposits arising from the sale of domestic assets to offset foreign exchange

obligations, especially if the liabilities are hedged in the local currency.

The widely held belief that

bank funds borrowed offshore give rise to escalating property prices is false. This

is because the domestic debt that causes the borrowing has already been created

to fund the current account deficit. On the other hand, as described in Section

4 of this paper, the sale of domestic assets to settle the debtor country’s

foreign exchange obligations does result in debtor country deposits that do tend to inflate existing asset “values” there as well as

increase the debt model systemic inflation.

The

creation of domestic debt in the debtor country precedes the return capital

flow from the creditor country. The sale by NZ registered banks of bonds to

foreigners is just another form of foreign investment by the creditor country.

The root cause of asset price inflation rests in the mechanics of the debt

system itself, as set out in the debt model for which links are provided at the

start of Section

The situation in debtor

countries is slightly more complicated than shown in Figure 3. Figure 3

shows what creditor countries buy with their inward capital flow. The capital

comes in, and domestic assets of the debtor country are sold, though often

indirectly as in the case of investment categories I3, I4 and I6, including

bank commercial paper.

Domestic assets in debtor

countries, on the other hand, do not just pass into foreign ownership. There is

a further issue over what the domestic seller in the debtor country does with

the deposit resulting from the sale of domestic assets. For example, if the

loans and bonds to business (I3) are used to finance mergers there is no new

productive investment from the process. If deposits from the purchase of

existing assets (I5) by foreigners are used for consumption or for bidding up

the price of other existing assets (for example if the previous owner retires)

they will lead to asset price inflation. The opposite would be the case if they

were used to retire existing domestic debt. While Figure 3 assumes for

simplicity that none of the T3 capital flows is used for consumption it is

theoretically possible some consumption does occur.

Fundamentally,

there is no such thing as foreign debt. There is only foreign ownership

of a debtor country’s productive resources and other assets. Current account

surpluses must be generated if the foreign ownership is to be reduced.

The new productive investments

shown in Figure 2 produce income. They form part of the (presumably) growing

productive sector. The debt used to purchase them is progressively repaid from

the income received.

Any part of aggregate domestic

production incomes held by foreigners that is repatriated abroad is part of the

current account of both the debtor and creditor countries. In

Current

account transactions are EXCHANGE transactions, not production transactions. In the debtor

country GDP incomes exclude extra payments needed to pay for surplus imports.

The “balance on external goods and services” is part of the additional debt it

must borrow to settle its current account. The additional debt figure is negative

when the balance on external goods and services is positive and positive when

the balance is negative. A positive trade balance simply reduces the current

account deficit of a debtor country. A similar thing happens in the creditor

country. There the incomes that still exist when the surplus goods are exported

are offset (sterilised) by the subsequent purchase of offshore assets.

There is no “saving” residual on the “use of

income” side of the National income and outlay account because the items

Current account balance (CA) and the “Purchase abroad of non-productive capital

investment goods” there cancel each other out. There is, instead, (subject

always to the following sections 6 and 7 of this paper and Figure 4 below) a

known quantum of saving as in equation (15).

Saving S

(net) = + Gross capital formation (including

increase in stocks) [59].

- Consumption of fixed capital (depreciation).

+ Statistical discrepancy [60].

(15)

[59]

Gross capital formation is the same as Investment. The increase in stocks is

also usually treated as investment by convention.

[60] Required

because of errors in the GDP production and expenditure estimates even though

the operating surplus is itself already a residual.

That brings the national

income and outlay account into agreement with conventional economic theory as

discussed in Section 4 as long as

depreciation is replaced with “principal repayments” and as long as the gross

operating surplus is what is left after the balance on the external account has

been subtracted.

Leaving aside the Current

Account balance as in Section 4 of this paper and substituting directly from

SNA Table 1.1 of the National Accounts, the “income” side of the National

income an outlay account then becomes:

National disposable income

(DI) = Compensation of employees

+ Gross operating surplus

+ Taxes on production and imports

(less subsidies)

Change in inventories

Gross fixed capital

formation

+ Gross fixed capital

formation (including increase in stocks)

- Consumption of fixed

capital

(16)

Even more simply, substituting

the terms for GDP from equation

National disposable

income (DI) = Gross Domestic Product

- Balance on external goods and services

- Consumption of fixed

capital (17)

Equation 17

is logical as long as “consumption of fixed capital” is replaced with

“principal repayments”, as discussed in Section 7 of this paper. The total

amount available to spend is what is earned less debt cancellation through debt

retirement and what by necessity has been spent or sent abroad. A positive

balance on external goods and services is not “disposable” because it is

unavailable to the domestic economy. On the other hand, a negative balance is

“disposable” because it is available to the domestic economy even though the

“income” to buy it is borrowed rather than earned. That means National

disposable income is quite a different concept from GDP, and, on the face of

it, is misnamed. The “statistical discrepancy” in equation (15) might not be

required because there would be only one residual number in Tables 1.1 and 1.2

of the National Accounts, namely the “gross operating surplus” whereas there

were previously two: the “gross operating surplus” and “saving”.

And, where the current account

surplus is treated as income in the National accounts, it must included in both

sides of DI:

Use of income side: =

Final consumption C

+ Purchase abroad of non-productive

capital investment goods (=CA)

+ Saving for productive investment