NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 :15 June, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the (Jaromir

Benes and Michael Kumhof) Chicago Plan Revisited Paper.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

There’s no such thing as affordable housing.

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple Starts

Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

![]()

This

work is licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence

THERE’S

NO SUCH THING AS AFFORDABLE HOUSING.

By

Sustento Institute,

08 June, 2013.

Version 4 : Distribution

2.

Email: manning@kapiti.co.nz ; bakensverzet@x4all.nl

Edition 01 :15 June, 2013.

The concept of “affordable

housing” is political propaganda, a hand washing exercise so governments can

“feel good” while household home ownership rates in

Property, especially

residential property, is one of the few genuine “markets” left in

Everyone in the property

business knows that property values are the sum of the land value and the value

of improvements.

The main value of the

improvements is the house or other building on the land. That building has a

cost made up of materials, labour, council and government compliance costs and

the like. The cost of housing in

A cheaper building has to be

smaller and simpler and use relatively lower grade fittings, because everything

else is controlled by the applicable standards and regulations. So, a

government that talks about a cheap or

affordable house it is really talking about a lesser house in respect of

size, comfort and quality.

Since house “costs” do not govern

the variation in property values, the land value must be doing so. Wide

variations in land values mean they are subjectively assessed according to

location and demand. Those factors determine the relative value of land from

one place to the other, but not the value

of the land in aggregate.

The aggregate “value” of the

land portion of the property is determined by the pool of investment money

available to purchase and exchange it, not by the land itself or government

policy.

Residential property forms a

large part of the value of unproductive capital investment in all developed

countries. When the banking system deposits increase sharply, so will land

prices in aggregate, and therefore

property prices in aggregate, but not the

prices of the improvements on them. This is true for all non-productive investments in

equities and commercial paper as well. The relative weighting of non-commercial

property, equities, government and commercial paper, and bank deposits depends

on regulatory policy settings such as tax rates, lending criteria, subsidies

and the perceived impact of offshore events.

In

The year to year correlation

of the two graphs in Figure 1 is low because housing is only one of four areas

of non-productive investment, the others being equities, government and

commercial paper, and bank deposits.

Investors always have a choice

where to invest. For example, during the dotcom boom, equities were preferred

relative to residential housing. House prices at that time fell briefly while

bank borrowing surged.

The M3 data also reflects changes

induced by offshore “crises”. From 2002 to 2007, after the dotcom crash,

housing was relatively preferred to other forms of investment as Figure 1 shows

clearly. The plunge in property prices in 2008 and 2009 largely reflects

investor withdrawal from the housing market in sympathy with the

In the March years 2011 and 2012 the rate of the increase in house

prices was less than that for M3 because equities prices rose very

quickly. Yet there was no move by the

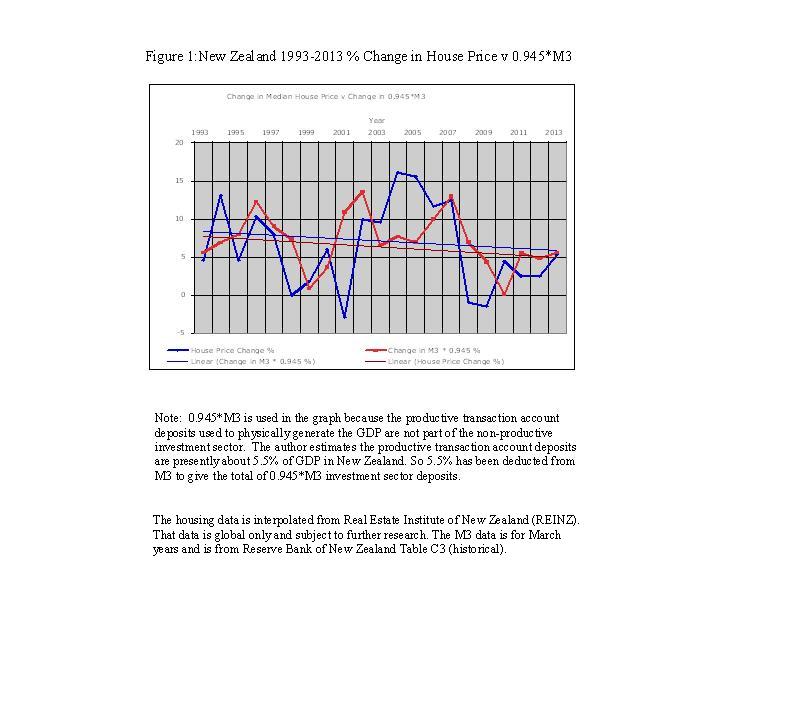

Note that 0.945*M3 is used in the graph in Figure 1

because the productive transaction account deposits used to physically generate

the GDP are not part of the non-productive investment sector. The author estimates the productive

transaction account deposits are presently about 5.5% of GDP in

Figure 1: New Zealand 1993-2013

: % Change in House Price v. 0.945*M3.

{kind=link}

The trend lines in Figure 1 rest

almost on top of one another. That shows that over the past 20 years house

prices have followed the money supply (0.945*M3) available to the investment

sector, not the physical cost of building houses or of developing land.

A government or a territorial

authority that “forces” housing development in chosen areas is literally

squeezing on a housing balloon. In

The only way to reduce the

rise in real property “values” in aggregate, and residential housing prices in

particular, is to slow the increase in the money supply as a whole. Unfortunately

for the government the money supply growth

in the existing debt-based financial system is systemic. It cannot arbitrarily be reduced below the trend line shown in Figure 1 without wrecking

the economy.

The mechanics of the debt

system are fully described by

the author in Financial system mechanics

explained for the first time. “The Ripple Starts Here”, a paper presented at the annual conference of the

New Zealand Association of Economists’ 50th in July, 2009. The paper

develops a simple debt model of the economy. Later updated papers are also

available at www.integrateddevelopment.org. The paper shows that systemic inflation is

the net deposit interest paid on deposits, while the systemic inflation rate is the net interest expressed as %

GDP.

The debt system mechanics

require that the total money supply increases by an amount sufficient to cover

systemic inflation (presently about 1.75%)

plus “growth” (say 1.5% after deducting a productivity increase of about

1%) plus domestic deposits that

result from the current account deficit. A positive balance of trade is counted

as GDP “growth” but it does not appear in domestic deposits because it is “used up” to reduce the size of the current account deficit. The GDP “growth”

figures in the official data for

In

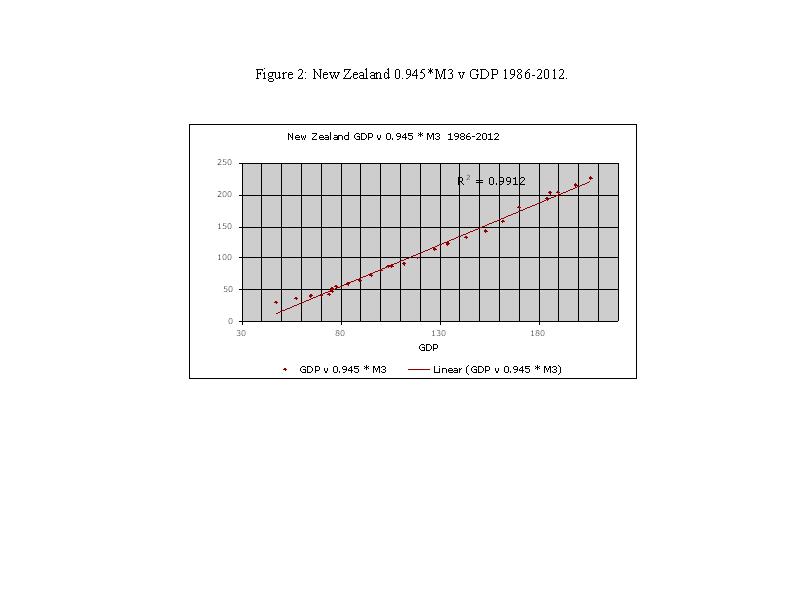

As discussed below, the excessive investment sector growth in debtor

countries like

Figure 2: New Zealand 0.945*M3

v GDP 1986-2012.

{kind=link}

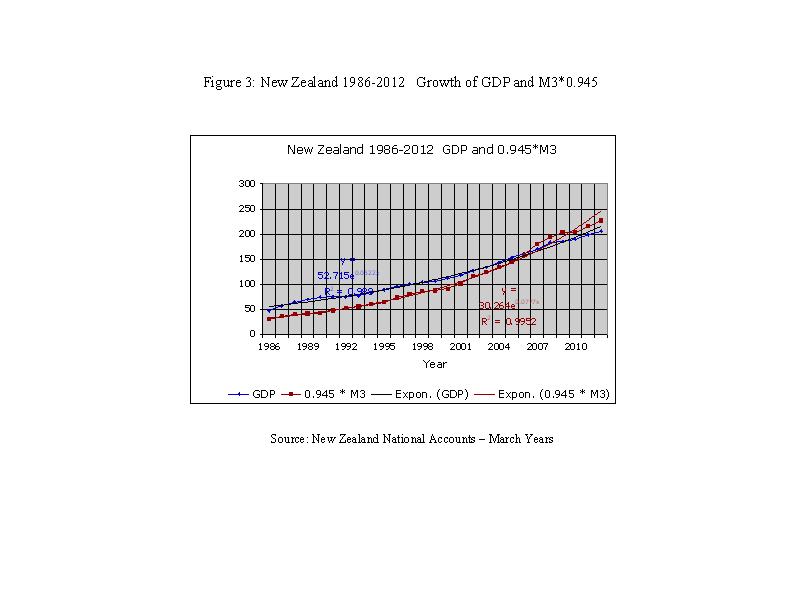

Figure 3: New Zealand

1986-2012:Growth of GDP and M3*0.945.

{kind=link}

The trendlines in Figure 3 are

exponential because the payment of deposit interest in the interest-bearing

debt system creates systemic inflation as mentioned on page 4. The net

additional flow of deposits from the current account deficit creates a

different exponential rate of growth of the investment sector relative to

GDP. That differential rate of growth has been about 0.7%/year over the period

1986-2012. The exponentials

shown in Figure 3 (5.2%, 7.8%) cannot be compared directly because the curves

in Figure 3 have different starting points. If the data series are set at the

same starting point (52.7) the 0.945*M3 exponential would be 5.9 instead of

7.8. This shows that 0.945*M3 increased 0.7%/year faster than GDP from

1986-2012.

Due mainly to the current

account deficits, the investment sector has grown at 5.9%/year while nominal

GDP has grown at 5.2%/year over the same period. That is why prices in the

non-productive investment sector are “overvalued”.

While nominal GDP has grown by

$159.2 billion, 0.945*M3 has grown by $196.3 billion, a difference of $37.1 billion. That extra $37.1 billion represents

surplus deposits over and above those needed to fund the principal outstanding

on capital investments in the capitalist system. The total surplus is more than $37.1 billion because the accumulated

surplus from before 1985 needs to be added. The total is thought to be a little

over $40 billion.

The author’s paper the “DNA of the debt-based economy”

demonstrates that GDP equals the outstanding principal on capital

investments. Were the growth of 0.945* M3

to exactly follow the growth of nominal GDP, the increase in the prices of

existing capital assets in aggregate

would mirror GDP growth. As shown in equation (1) below, it is mathematically

impossible for the total deposits to be lower than the existing

interest-bearing debt in the capitalist system after subtracting the banks’

residual (net worth) that they have “captured” from the deposit base (mostly

their net retained profits) and the country’s net foreign currency debt.

Debt figures used in this article exclude secondary

savings and loan debt such as the on-lending of deposits through finance

companies and other non-bank financial institutions. Secondary debt is thought

to amount to about 10% of Domestic Credit in

Debt is linked to deposits and the current account/NIIP by the formula:

(DC + NFCA) = M3 + Residual (1)

Assets = Deposit Liabilities + Net worth

Use of the

Net International Investment Position, (NIIP) in equation (1) might be a little

more accurate but the author uses the

current account for simplicity.

The formula represents the basic accounting equation viewed from the

banks’ point of view, where DC is Domestic Credit, M3 is the total bank

deposits, NCFA is the Net Foreign Currency Assets of the banking system and

Residual is the net worth of the banking system. The Residual is positive when the equation is in that

form, and NFCA is negative for debtor countries.

The numbers for

DC was $333.2 billion.

NFCA was $-52,6 billion.

M3 was $ 253,6 billion.

Residual was + $ 27.0 billion.

Applying Formula (1) to

$333.2 b - $52.6b = $253.6b + $27.0b

At that time,

-

- $151.2b (the accumulated current account deficit

$203.8 b.- the net foreign currency assets $52.6 b.) of the deposits created to

fund the accumulated current account deficit had therefore been returned to New

Zealand in the form of foreign ownership,

The annual GDP for 2012

($209.3b) x 1.055%, or $220.8b, of the $253.6b M3 deposit base was needed for

capital and to fund the productive transaction accounts. The productive

transaction accounts in

The multiplier 1.055 is used

because the dynamic transaction account balance (0.055* GDP) must be added to

GDP (the net outstanding principal on capital investments) to get the minimum

debt needed to fund a capitalist economy before taking into account the NFCA

and bank Residual.

The domestic money supply M3 ($253.6b) –

the annual GDP for 2012 $209.3b x 1.055%] ($220.8b) gives an amount of

$32.8b.

Between

1985 and 2012

Recent IMF comments that

housing in

In

New Zealand therefore remains

at risk of further asset inflation should the present arbitraging of interest

rates by the New Zealand banks be reversed. As shown on page 7, the banks have

borrowed a net amount of $52.6b, the

NFCA, offshore. They have done so because it is cheaper for them to do that than

pay deposit interest in

International financial institutions

are concerned with financial stability. They are not concerned about the

economic asymmetry that foreign ownership of a domestic economy creates. Nor

are they concerned about domestic imbalances in wealth and income distribution.

If the banks were to stop borrowing money abroad to finance their operations,

most of the NFCA of $52.6 billion would be invested in existing assets in

There are two main options to

“pop” the housing “investment bubble”. Neither of them has anything to do with

building houses!

In

The

The second option makes more

sense because it removes a primary source

of the structural asset “bubble”, namely the persistent growth of foreign

ownership through the current account. Reversing that growth means managing the

exchange rate, but the government and it advisors like the Treasury and the

Reserve Bank of

The government could easily

set up a variable and tax neutral Foreign Transactions Surcharge (FTS) as set

out in the paper Using a foreign transactions

surcharge (FTS) to manage the exchange rate. The FTS is an

automatically collected levy on all outward domestic currency transactions

passing through the foreign exchange interface. Its effect would be to increase the aggregate cost of

repatriating domestic currency offshore and lower the aggregate cost of using

domestic currency locally. The revenue obtained from the levy would be used

only to reduce domestic taxation and to begin repayments of foreign debt, in

effect repurchasing those assets already ceded to foreigners. While an FTS will

correct the exchange rate and current account it will have little immediate

effect on investment prices or the property market. It would instead lead to a

gradual easing of the rate of investment price increases over time.

There is no such thing as

affordable housing. There is just a

housing market. Aggregate prices in that market are structural. Any government attempt to manipulate the market without

addressing the structural causes of property inflation will fail. The sooner

the government introduces a program to resolve the main issue of foreign

ownership generated through the current account deficit, the sooner house

prices will become more stable.

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English edition, Peter Owen,

![]()

This work is

licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence.